Market Definition

The global medtech market encompasses the development, manufacturing, and commercialization of medical devices, diagnostic equipment, and healthcare technologies designed to prevent, diagnose, monitor, and treat medical conditions. This market spans a broad range of product categories, including diagnostic imaging systems, in vitro diagnostics, cardiovascular devices, orthopedic implants, surgical instruments, patient monitoring systems, and digital health solutions.

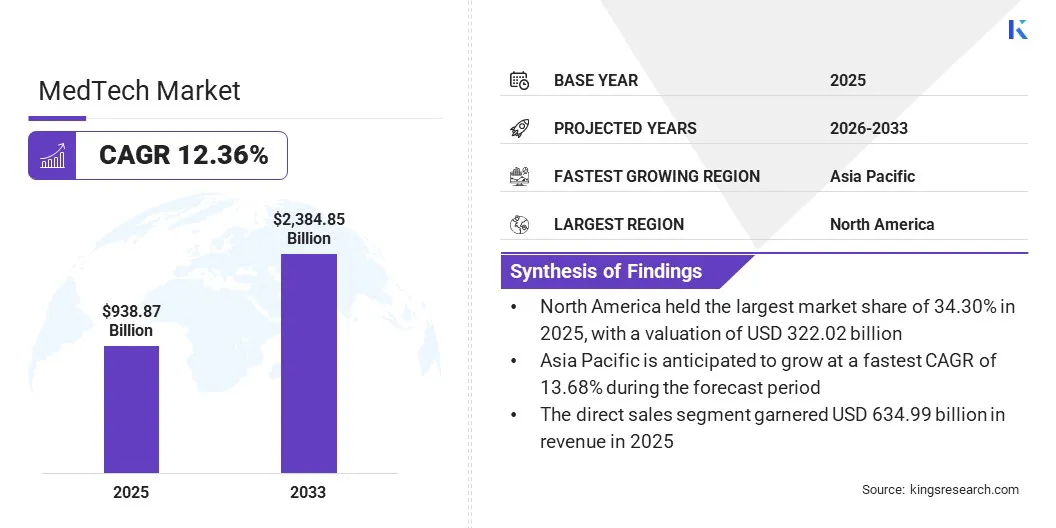

MedTech Market Overview

The global medtech industry size was valued at USD 938.87 billion in 2025 and is projected to reach USD 2,384.85 billion by 2033, exhibiting a CAGR of 12.36% during the forecast period. This growth is driven by advancements in medical technology, an increase in healthcare expenditures, rising prevalence of chronic diseases, and adoption of digital health solutions worldwide.

Major companies operating in the global medtech market are Medtronic, Johnson & Johnson, Abbott, Medline, Siemens Healthineers AG, Stryker, Becton, Dickinson and Company (BD), GE Healthcare, Baxter International Inc., Boston Scientific, B.Braun SE, Koninklijke Philips NV, Olympus Corp., OMRON Corp., and Roche Diagnostics.

Additionally, supportive government policies and investment in healthcare infrastructure are accelerating market expansion. The integration of artificial intelligence and robotics is further transforming diagnostics and treatment workflows, while ongoing innovation continues to enhance patient outcomes and operational efficiency across healthcare systems.

- In September 2024, iGan Partners announced a strategic alliance with Medical Alley to accelerate MedTech innovation in Canada and the U.S. The partnership aims to identify, support, and scale promising startups, leveraging Medical Alley’s network and iGan’s investment expertise to advance pioneering healthcare technologies and improve patient outcomes.

Key Market Highlights

- The global medtech market size was valued at USD 938.87 billion in 2025.

- The market is projected to grow at a CAGR of 12.36% from 2026 to 2033.

- North America held a 34.30% market share in 2025, valued at USD 322.02 billion.

- The medical devices segment garnered USD 594.63 billion in revenue in 2025.

- The direct sales segment is expected to reach USD 1,551.99 billion by 2033.

- Asia Pacific is anticipated to grow at a CAGR of 13.68% through the projection period.

How is the rising global prevalence of chronic diseases driving the growth of the medtech market?

The worldwide prevalence of non-communicable diseases (NCDs) such as cardiovascular disease, cancer, chronic respiratory disease, and diabetes remains a fundamental driver of the global medtech industry. In September 2025, the World Health Organization stated that 75% of all people died from non-communicable diseases in 2021, underscoring the scale of the global disease burden that healthcare systems must address.

This widespread and sustained burden is prompting simultaneous investment in medical technologies across both mature and emerging markets. These investments range from advanced diagnostic imaging and cardiac devices in developed nations to essential screening and monitoring equipment in resource-constrained settings. NCDs affect populations across every region and income level, resulting in consistent global demand for diagnostics, therapeutics, monitoring devices, and preventive care technologies.

How is the fragmentation of regulatory environments across regions hindering the growth of the global medtech market?

Despite international harmonization efforts, significant disparities persist between major regulatory bodies like the U.S. FDA, the EU’s MDR, and authorities in Asia-Pacific and Latin America. Variations in clinical evidence requirements, approval timelines, and post-market surveillance force manufacturers to develop separate compliance strategies for each market, raising complexity and costs. This patchwork of regulations can slow product launches, impede global market access, and disproportionately impact smaller companies.

To address this challenge, companies are investing in specialized regulatory affairs teams and leveraging local regulatory expertise in each target market. Industry players are also participating in global harmonization initiatives and forming strategic partnerships to streamline compliance and accelerate product approvals across regions.

How is the integration of artificial intelligence in diagnostics and imaging influencing the development of the medtech market?

The adoption of artificial intelligence across diagnostic and imaging applications is emerging as the most influential trend in the global medtech industry. Manufacturers are embedding machine learning capabilities directly into diagnostic devices to assist clinicians in identifying abnormalities, prioritizing urgent cases, and reducing diagnostic variability across practitioners and regions.

This momentum is being reinforced by regulatory bodies in multiple countries establishing dedicated approval pathways for AI-based software as a medical device. As healthcare systems across both developed and emerging markets face growing patient volumes alongside limited specialist availability, AI-assisted diagnostics are positioned as a central tool for improving efficiency and diagnostic accuracy on a global scale.

- In March 2024, Johnson & Johnson MedTech announced a collaboration with NVIDIA to accelerate and scale AI for surgery. The partnership aims to enable secure, real-time analysis and deployment of AI models within connected operating rooms, supporting improved surgical decision-making, training, and global access to advanced digital health solutions.

MedTech Market Report Snapshot

|

Segmentation

|

Details

|

|

By Product Type

|

Medical Devices, Digital Health & Healthcare IT, and Healthcare Robotics

|

|

By Distribution Channel

|

Direct Sales and Indirect Sales

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Product Type (Medical Devices, Digital Health & Healthcare IT, and Healthcare Robotics): The medical devices segment earned USD 594.63 billion in 2025, due to the demand for advanced diagnostic tools, rising chronic disease rates, technological innovation, and expanding healthcare infrastructure globally, making it the leading contributor in the market.

- By Distribution Channel (Direct Sales and Indirect Sales): The direct sales segment held 67.63% of the market in 2025, due to stronger relationships between manufacturers and healthcare providers, greater control over pricing and product education, and the preference for customized solutions, ensuring efficient delivery and enhanced customer support in the medtech industry.

What is the market scenario in North America and Asia Pacific?

Based on region, the global medtech market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

The North America market share stood at around 34.30% in 2025, valued at USD 322.02 billion. The dominant share is supported by a mature healthcare infrastructure, technological innovations, and significant investments in research and development across the region. The region benefits from well-established public and private reimbursement systems, which help accelerate the adoption of new medical technologies.

Strong institutional research capacity, extensive collaboration between academic medical centers and industry, and a robust venture capital ecosystem continue to fuel product innovation and commercialization. Canada complements this position through steady public healthcare investment and growing adoption of digital health tools, reinforcing the region's status as the largest revenue-generating medtech market globally.

- In August 2025, Philips announced over USD 150 million in new investments to expand U.S. manufacturing and R&D for AI-powered health technology. The initiative will enhance facilities in Pennsylvania and Minnesota, further supporting Philips’ advanced solutions used by clinicians in 90% of U.S. hospitals.

The Asia Pacific medtech industry is set to grow at a 13.68% CAGR over the forecast period, driven by an aging population, expanding healthcare infrastructure, and rising disposable incomes across regions. This demographic shift is prompting governments to increase public healthcare expenditure and expand national health insurance schemes, improving medical technology access across both urban and rural settings. The region has also emerged as a major manufacturing hub, with countries like China and India scaling domestic device production to reduce import dependence. Rapid urbanization and a growing base of private healthcare providers further support the region's accelerated market expansion.

- In April 2026, ANSR launched ANSR MedTech, a global capability center in India for a Fortune 100 MedTech company. The center will drive next-generation healthcare platforms, leveraging AI, cloud, and analytics to accelerate global MedTech innovation and develop advanced digital health and wearable technologies.

Regulatory Frameworks

- In the United States, the Food and Drug Administration (FDA) under the Federal Food, Drug, and Cosmetic Act (FD&C Act) regulates medical devices. It ensures the safety, effectiveness, and quality of devices entering the U.S. market, critical for protecting patient health in the medtech sector.

- In the European Union, the Medical Device Regulation (MDR) (EU 2017/745) governs medical devices. It establishes strict requirements for device safety, traceability, and clinical evaluation, enhancing market transparency and patient safety across EU countries.

Competitive Landscape

The global medtech market is moderately consolidated, comprising both leading international corporations and specialized regional companies that compete across a diverse array of product categories. Leading companies maintain strong positions through extensive product portfolios, global distribution networks, and continuous investment in research and development. These companies compete based on technological innovation, regulatory approvals, and strategic partnerships with healthcare providers.

Mergers, acquisitions, and collaborations remain common strategies for expanding therapeutic coverage and entering emerging markets. Meanwhile, smaller and mid-sized companies are carving out niches in specialized segments such as digital health, minimally invasive devices, and AI-enabled diagnostics, increasing competition and accelerating the pace of innovation across the industry.

- In February 2026, Alkem MedTech announced its intent to acquire up to 55% of Occlutech Holding, a Swiss leader in minimally invasive cardiac implants, for USD 117.5 million. This move marks Alkem’s entry into advanced cardiovascular devices and expands its global presence in the medical technology sector.

Key Companies In The MedTech Market

- Medtronic

- Johnson & Johnson

- Abbott

- Medline

- Siemens Healthineers AG

- Stryker

- Becton, Dickinson and Company (BD)

- GE Healthcare

- Baxter International Inc.

- Boston Scientific

- Braun SE

- Koninklijke Philips NV

- Olympus Corp.

- OMRON Corp.

- Roche Diagnostics

Recent Developments

- In June 2025, ClavystBio and A*STAR signed an MoU to accelerate MedTech ventures in Singapore. This two-year partnership will focus on venture creation, product development, and commercialization, leveraging both organizations’ expertise to strengthen Singapore’s MedTech ecosystem and support scaling of local innovations to global markets.

- In January 2024, IISc and Wipro GE Healthcare signed an MoU to advance MedTech innovation in India. The collaboration will focus on co-developing, validating, and locally manufacturing healthcare technologies in areas like AI, robotics, and precision care to address non-communicable diseases and boost India’s MedTech ecosystem.

- In March 2026, AdvaMed and Informa’s LSX Portfolio formed a strategic global partnership to align major MedTech events across the US, Europe, and Asia-Pacific. This collaboration will expand global reach, drive innovation, and create new opportunities for companies, investors, and partners in the MedTech sector.

- In May 2026, Sequenex partnered with MedTech Innovator, the world’s largest medtech startup accelerator. Sequenex will provide regulatory-ready software solutions and mentorship to selected startups. This partnership will accelerate the development and commercialization of connected medical devices, biosensors, and wearables, advancing healthcare innovation.

- In December 2023, BIOTRONIK opened a new Asia-Pacific Manufacturing and Research Hub in Singapore, spanning 20,000 m². The facility will support manufacturing, R&D, and sales, further strengthening Singapore’s MedTech ecosystem, especially in cardiac rhythm management devices.