Market Definition

The flat glass market refers to industry that manufactures and supplies flat glass sheet form used across construction, automotive, aerospace, electronics, and industrial sectors. The market includes various flat glass types, including float glass, tempered glass, laminated glass, coated glass, armored glass, lacquered glass, satin glass, and other specialty variants. The different types are manufactured using controlled processes like floating, rolling, tempering, and chemical or thermal treatments to achieve specific properties such as strength, safety, thermal insulation, soundproofing, and aesthetic enhancement.

The market is driven by the growing, increasing demand for energy-efficient and sustainable building materials in the construction industry; increasing adoption of advanced glazing solutions in modern architecture; and rising demand for lightweight, durable, and safety-enhanced glass in the automotive sector. Additionally, expanding applications in consumer electronics and solar energy systems with increased emphasis on safety and green building standards is further accelerating market growth.

Flat Glass Market Overview

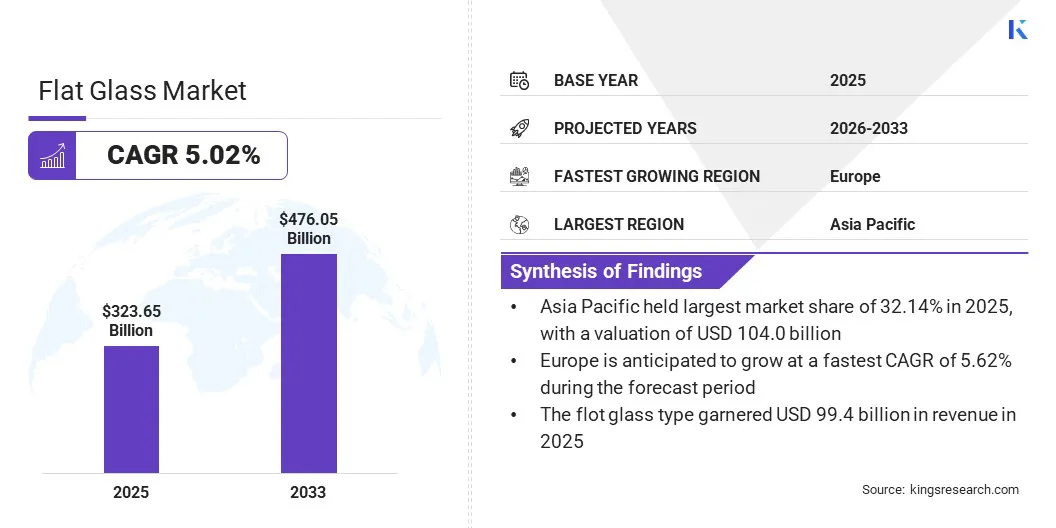

The global flat glass market was valued at USD 323.65 billion in 2025 and is projected to reach USD 476.05 billion by 2033, representing a CAGR of 5.02% over the forecast period. This rapid growth is propelled by the expansion of the global automotive sector along with the increasing demand for energy-efficient solutions in the building and construction sector across the globe. Government initiatives like Housing for All, implemented by the United Nations, which are targeted at providing affordable residential establishments across developing economies, act as a driving factor.

Major companies operating in the global flat glass industry include Asahi India Glass Limited, Taiwan Glass Industries Corp., CSG HOLDING CO., LTD., FUYAO GROUP, Nippon Sheet Glass Co., Ltd., Saint-Gobain, Şişecam, Central Glass Co., Ltd., AGC Inc., Trulite, SCHOTT, Cevital, CHINAGLASSHOLDING, Euro Glass, and Fuyao Glass Industry Group Co., Ltd.

Businesses across diverse end-user industries such as automotive, building and construction, and consumer electronics are adopting flat glass to enhance functionality, safety, and energy efficiency. The rise in the adoption of advanced flat glass products in the automotive sector with advanced safety systems like ADAS windshields, future augmented reality windshields systems, and connectivity with the Internet of Things presents market growth opportunities.

- In November 2025, Şişecam showcased its advanced automotive glass technologies, designed for the growing Head-Up Display (HUD) and Advanced Driver Assistance Systems (ADAS) trends, at the Auto Glass Week in Nevada, U.S. The coated products and heated glass solutions aid in maintaining cabin temperatures more efficiently, reducing reliance on fuel- or battery-powered climate systems, and supporting lower carbon emissions.

Key Market Highlights:

- The global flat glass market size was recorded at USD 323.65 billion in 2025.

- The market is projected to grow at a CAGR of 5.02% from 2026 to 2033.

- Asia Pacific held a share of 32.14 % in 2025, valued at USD 104.02 billion.

- The float glass segment garnered USD 99.39 billion in revenue in 2025.

- The direct sales segment is expected to reach USD 202.15 billion by 2033.

- The building and construction segment captured the largest share of 42.10% in 2025, with the valuation of USD 136.26 billion.

- Europe is anticipated to register the fastest CAGR of 5.62% through the projection period.

How Is The Rapid Growth In The Building And Construction Sector Driving Market Expansion?

The global surge in population and rapid urbanization is fueling market growth. The property of flat glass to retain heat inside a room or prevent excess heat from entering a room leads to a significant reduction in energy consumption from heating and cooling systems. This, in turn, boosts the demand for flat glass in residential and commercial buildings due to its energy efficiency, thermal insulation, and aesthetic appeal.

Moreover, the increasing emphasis on sustainable construction and green building standards promotes the adoption of advanced glazing solutions that reduce heat loss and energy consumption. Advancements in solar control glass, insulated glazing, and smart glass technologies are supporting market expansion by enhancing energy efficiency, occupant comfort, and environmental sustainability across the construction sector.

- In September 2025, Guardian Glass introduced SunGuard SNX 60 and SNX 60 Ultra, which are new triple-silver solar control glass products designed for commercial façades. The glazing offers high energy efficiency, strong thermal insulation, and a neutral, transparent appearance, allowing 60% natural light transmission while blocking much of the solar heat.

How Does Emission Of Greenhouse Gaseous Emissions In Flat Glass Production Negatively Impact The Flat Glass Market?

The generation of greenhouse gas emissions poses a major challenge to market development avenues. The melting and refining procedures in flat glass manufacturing require high energy utilization, which involves high economic and environmental costs. Additionally, the production processes lead to emissions of combustion by-products, comprising sulphur oxides (SOx), nitrogen oxides (NOx), and carbon dioxide (CO2), which increase global warming potential.

To address this challenge, industry leaders are optimizing POM manufacturing processes and adopting solutions such as carbon capture utilization and storage (CCUS), the inclusion of green hydrogen in manufacturing facilities, and circular economy approaches such as material recycling, process optimization, and closed-loop manufacturing practices.

- In July 2025, Ryze hydrogen signed a long-term agreement to supply hydrogen to the Goole, East Yorkshire flat glass facility of Guardian Glass. The partnership supports efforts to reduce carbon emissions in the glass industry, with Ryze collaborating through Glass Futures to explore hydrogen-based technologies and the adoption of sustainable industrial practices.

How Are Advancements In Low-E Glass And Solar Glass Emerging As A Notable Trend In The Flat Glass Market?

Low-E (low-emissivity) glass is a specially coated architectural flat glass that enhances energy efficiency, thermal insulation, and indoor comfort in residential and commercial establishments. The thermal insulation property of low-E glass enables the retention of indoor heat during colder months while preventing excess heat from entering during warmer seasons. It further provides effective solar control by reflecting a significant portion of solar heat while maximizing natural light transmission, thereby reducing air-conditioning loads, minimizing glare and blockage of harmful solar ultraviolet (UV) rays, and improving the overall visual comfort and durability of indoor environments. Additionally, low-E glass offers aesthetic flexibility, enabling architects to choose from different colors, transparency levels, and reflective finishes to create visually appealing façades and interiors.

- In September 2025, Saint-Gobain launched COOL-LITE XTREME 51/23 & 51/23 II, which are high-performance triple-silver-coated glass solutions. The solar control glazing products offer high daylight transmission with reduced heat gain and enhanced energy efficiency, aesthetics, and sustainability.

Flat Glass Market Report Snapshot

|

Segmentation

|

Details

|

|

By Type

|

Float Glass, Tempered Glass, Laminated Glass, Coated Glass, Armored Glass, Lacquered Glass, Satin Glass, Others

|

|

By Distribution Channel

|

Direct sales, Distributors / Wholesalers, Retail

|

|

By End Use

|

Automotive, Aerospace and Defense, Healthcare, Consumer Electronics, Building & Construction, Industrial, Commercial, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Type (Float Glass, Tempered Glass, Laminated Glass, Coated Glass, Armored Glass, Lacquered Glass, Satin Glass, and Others). The float glass segment accounted for USD 99.39 billion in 2025 and is anticipated to register the highest CAGR of 4.55% over the forecast period. The high clarity, smooth surface quality, versatility, cost-effectiveness, and durability make float glass preferable across building and construction, automotive, and industrial applications.

- By Distribution Channel (Direct Sales, Distributors / Wholesalers, Retail). The direct sales segment was valued at USD 134.64 billion in 2025 and is anticipated to register a CAGR of 5.29% over the forecast period. This robust growth is attributable to the presence of an immediate link between the manufacturer and the sales representative. This ensures the removal of intermediaries who are prone to altering marketing messages or misrepresenting flat glass products.

- By End Use (Automotive, Aerospace and Defense, Healthcare, Consumer Electronics, Building & Construction, Industrial, Commercial, Others). The building and construction segment accounted for a share of 42.10% and was valued at USD 136.26 billion in 2025. Rapid urbanization, infrastructure expansion, and rising demand for energy-efficient buildings, supported by government subsidies for green and sustainable construction projects, are creating strong demand for flat glass.

What Is The Market Scenario In Asia Pacific And European Region?

Based on region, the global flat glass market is split into North America, Europe, Asia Pacific, Middle East and Africa, and South America.

The Asia Pacific flat glass market share stood at 32.14% and was valued at USD 104.02 billion in 2025. Rising urbanization and high population growth necessitate development in the construction sector. The ongoing trend of smart city projects in China (like Nanjing, Zhuhai, Shenzhen, Hangzhou, Chongqing, Beijing, Shanghai, Chengdu), India (Smart Cities Missions), South Korea (Incheon smart city plan, Seoul smart city initiatives), and other parts of the region act as significant drivers propelling regional market expansion.

Additionally, the presence of major tech companies, robust IT infrastructure, and investments in AI, cloud computing, and digitization applications in the region further act as significant drivers for the market.

- In December 2025, India registered a boost in the development of Global Capability Centres (GCCs), transforming from basic support units into major innovation and R&D hubs. According to the Government of India, approximately 1,700 GCCs were registered as of FY 2025, supported by policy reforms, improved ease of doing business, and strong digital infrastructure. This positions India as a global hub for innovation and strategic enterprise operations, with continued expansion anticipated through 2030.

The Europe flat glass market is set to register the fastest CAGR of 5.62% over the forecast period. This rapid growth is fostered by rising emphasis on energy-efficient buildings. Countries in the European Union like the UK, Germany, France, and Spain have set ambitious goals under the European Green Deal, which ensures net-zero greenhouse gas emissions by 2050. The adoption of double-glazed and low-emissivity flat glass in Europe acts as a major contributor to enhancing thermal insulation in commercial and residential buildings, thereby supporting the achievement of climate goals.

- In April 2026, EU Energy Performance of Buildings Directive (EPBD) released a framework to decarbonize the EU’s building stock by 2050. The directive directly benefits the market by accelerating demand for energy-efficient building materials used in renovation and new construction and further supporting wider adoption of high-performance glazing solutions such as double and triple glazing, Low-E coated glass, and solar control glass.

Regulatory Frameworks

- In the U.S., the Environmental Protection Agency (EPA) issues Glass Manufacturing Effluent Guidelines and Standards (40 CFR Part 426), which regulate wastewater discharges from the glass manufacturing industry. The guidelines are applicable to both direct and indirect dischargers through permit and pretreatment programs and cover various glass manufacturing sectors, including flat glass, fiberglass, containers, and automotive glass, while setting limits for pollutants such as ammonia, fluoride, lead, oil, and suspended solids.

- In Europe, the Carbon Border Adjustment Mechanism (CBAM) ensures fair carbon pricing on imported carbon-intensive goods like flat glass. The framework prevents “carbon leakage” by making imports face similar carbon costs under the EU Emissions Trading System (ETS). It further ensures cleaner industrial production in the European region while simultaneously supporting the climate and decarbonization goals of the region.

- In China, the Emission Standard of Air Pollutants for the Flat Glass Industry (GB 26453-2011) framework strengthens environmental protection and regulates air pollutant emissions from flat glass manufacturing facilities. The standard defines emission limits, monitoring requirements, and compliance measures for both existing plants and new construction projects.

Competitive Landscape

Key players in the flat glass market are launching innovative solutions to cater to diverse end-use industries, including the building and construction, automotive, and industrial sectors. Innovations targeted at improving energy efficiency, automation, precision, and production flexibility, while supporting high-performance and lightweight glass applications, are gaining traction in the market.

- In March 2026, Glaston showcased its latest flat glass processing innovations at China Glass 2026, focusing on efficiency, automation, and sustainability. The company showcased innovations such as the ULTRA TPS system for ultra-thin insulating glass, the TC Series with Chinook technology for faster and cost-efficient tempering, and the CHAMP EVO & MATRIX EVO solutions for high-precision mobility glass processing.

Additionally, market players are prioritizing the integration of sustainability initiatives, including the reduction of carbon footprints, achieving net-zero effluent emissions, and the adoption of renewable or green energy solutions in flat glass manufacturing.

- In August 2025, AGC Group laid down plans for a reduction in its carbon footprint by 30% by 2030 and to achieve net-zero carbon emissions for Scopes 1 and 2 by 2050. The company implemented a comprehensive decarbonization roadmap covering the entire value chain, with key initiatives comprising the enhanced use of renewable and low-carbon electricity, the expansion of its glass recycling program, and achieving ISO 50001 certification across all Architectural Upstream production sites.

Key Companies in The Flat Glass Market

- Asahi India Glass Limited

- Taiwan Glass Industries Corp.

- CSG HOLDING CO., LTD.

- FUYAO GROUP

- Nippon Sheet Glass Co., Ltd.

- Saint-Gobain

- Şişecam

- Central Glass Co., Ltd.

- AGC Inc.

- Trulite

- SCHOTT

- Cevital

- CHINAGLASSHOLDING

- Euro Glass

- Fuyao Glass Industry Group Co., Ltd.

Recent Developments

- In March 2025, AGC Glass Europe S.A. inaugurated the refurbished flat glass production line at the AGC Barevka plant in Teplice. The facility features a pilot furnace using the world's first innovative flat glass production technology. The project has been named the Volta R&D Project and is developed in collaboration between AGC and Saint-Gobain, and is financially supported by the EU Innovation Fund.

- In January 2025, NSG Group announced the conversion of an existing float glass line at its Pilkington North America facility in Rossford, Ohio, to produce transparent conductive oxide (TCO), a type of functional flat glass. The investment is targeted at expanding First Solar’s strategy and strengthens the long-standing partnership between the two companies in thin-film photovoltaic technology.

- In January 2025, NSG Group inaugurated a new solar flat glass production line in Ohio to support First Solar’s cadmium telluride (CdTe) thin-film photovoltaic manufacturing expansion. The project involves the development of a transparent conductive oxide (TCO) flat glass production facility, utilizing online coating technology. This is anticipated to enable the production of durable and cost-effective, high-volume TCO flat glass for solar applications.