Market Definition

The NAND flash market refers to the ecosystem of non-volatile storage technology, which is widely utilized in solid-state drives (SSDs), USB flash drives, and memory cards. The scalable, cost-effective, and high-performance capabilities of NAND flash drive its adoption across end-use verticals, spanning consumer electronics, enterprise IT, and hyperscale cloud data centers. The booming data center landscape in the U.S. further fuels the demand for high-performance, energy-efficient storage solutions to handle data-intensive workloads.

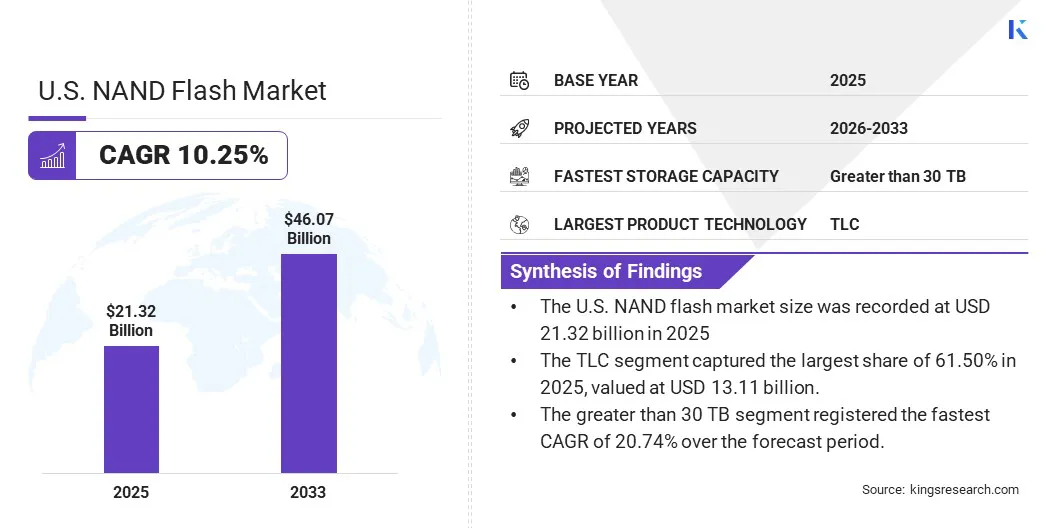

U.S. NAND Flash Market Overview

The U.S. NAND flash market size was valued at USD 21.32 billion in 2025 and is projected to reach USD 46.07 billion by 2033, representing a CAGR of 10.25% over the forecast period. This growth is mainly propelled by the ability of NAND flash to deliver faster read/write speeds, higher storage capacity, and improved power efficiency compared to conventional storage solutions. Additionally, the surge in data center development to support AI infrastructure, cloud computing, and edge applications across the commercial and industrial landscape of the U.S. is creating growth opportunities.

Key players operating in the market, including Samsung, Micron Technology, Inc., SK Hynix Inc., KIOXIA Corporation, Western Digital Corporation, SanDisk Corporation, Kingston Technology, Seagate Technology LLC, Marvell, and Transcend Information, Inc., are focusing on developing AI-optimized solid-state drives and next-generation NAND technologies to address the rising AI computing demands from enterprises and hyperscale data centers.

- In June 2026, SK Hynix announced plans to invest approximately USD 66 billion to expand NAND flash production and strengthen advanced packaging capabilities for high-bandwidth memory (HBM). The plan involves investments in semiconductor cluster expansion to address the growing demand from AI data center projects.

Key Market Highlights:

- The U.S. NAND flash market size was recorded at USD 21.32 billion in 2025.

- The market is projected to grow at a CAGR of 10.25% from 2026 to 2033.

- The TLC segment captured the largest share of 61.50% in 2025, valued at USD 13.11 billion.

- The greater than 30 TB segment registered the fastest CAGR of 20.74% over the forecast period.

- The internal storage segment garnered the largest share of 77.50% in 2025 and was valued at USD 16.52 billion.

- The automotive segment is anticipated to register the highest CAGR of 20.95% over the forecast period, reaching a value of USD 5.90 billion in 2033.

How is the adoption of artificial intelligence and machine learning driving market growth?

AI training and inference workloads process enormous datasets, which create unprecedented demand for enterprise-grade solid-state drives that rely on advanced high-layer NAND flash technologies. The expansion of AI computing infrastructure by major cloud service providers (CSPs), including Microsoft, Amazon, and Google, to train large language models (LLMs) further boosts the demand for high-end NAND-based SSDs. The evolution of the AI ecosystem from model training to real-time inference and the deployment of LLMs is presenting growth opportunities.

Inference AI workloads operate continuously to generate responses and predictions across millions of connected devices, resulting in substantially higher requirements for memory bandwidth, storage capacity, and energy efficiency. This evolving workload characteristic creates demand for NAND flash memory technologies that offer high-speed performance with minimal power consumption.

- In June 2026, Micron Technology launched products to address the rising memory bandwidth, storage capacity, and power efficiency requirements associated with large-scale AI inference and reasoning workloads. The company introduced HBM4 36GB 12H, 256GB SOCAMM2, 256GB DDR5 RDIMM based on 1γ technology, the Micron 9650 PCIe Gen6 SSD, and the Micron 6600 ION SSD to support AI data center workloads.

- In May 2025, Pure Storage partnered with memory provider SK Hynix to deliver QLC (Quad-level cell) flash storage products to hyperscale data centers. The solution involves providing rack-dense and scalable systems to address demanding storage scalability requirements, while lowering energy consumption and operating costs.

How is the price hike in NAND flash negatively impacting the U.S. market?

The sharp rise in the prices of NAND flash and DRAM in the global semiconductor industry is attributed to constrained supply, shifting capacity allocation, and surging AI and data center demand, which is highlighting the need for enterprise-grade, high-capacity, and high-performance storage solutions. Furthermore, chipmakers are reallocating wafer capacity towards more profitable AI-related memory products, including HBM (High Bandwidth Memory), thereby tightening the general-purpose NAND supply.

For instance, Samsung announced plans to hike NAND flash prices by up to 100% in Q2 2026, following similar increases in Q1 2026, resulting in an overall rise of more than 200% in NAND prices during 2026. Similarly, Kingston reported a 246% increase in NAND wafer pricing compared to Q1 2025, with a 70% price increase occurring within 60 days, resulting in significant hikes in NAND flash prices. Additionally, KIOXIA reported a complete sell-out of its NAND flash production for 2026, with the supply-demand imbalance expected to persist until 2027 due to the global AI boom. Moreover, NAND flash production expansion from Chinese manufacturers, due to their domestic substitution policies and intensifying global market competition, further intensifies pricing pressure. This dual pressure from surging AI demand and limited production capacity is fueling the significant upward trend in NAND flash pricing in the U.S.

To address this challenge, market players are transitioning to higher-stacked cell layers, which enable higher-capacity NAND chips and eventually reduce costs and the number of chips required in solid-state drives (SSDs).

- In May 2026, Samsung introduced a 900-layer 3D NAND prototype by stacking two 450-layer strings, which marks a major leap beyond current industry technology. The prototype successfully reads and writes data while using new techniques to control wafer warpage, improve alignment, and reduce power consumption.

- In November 2024, SK Hynix commenced mass production of its 321-Layer 4D NAND flash with a storage capacity of 1 Tb. The product incorporates the “Three Plugs” process technology for stacking and improves speed and power efficiency.

How is the adoption of high bandwidth flash emerging as a notable trend in the U.S. NAND flash market?

High bandwidth flash (HBF) memory architecture offers high-storage capacity, enhanced energy efficiency, improved thermal stability. This fuels its applicability in emerging AI workloads and high-performance computing. HBF architectures utilize parallelism, advanced logic scaling, and custom stacking techniques to deliver low latency and high bandwidth, enabling large language models to stream data at near-DRAM speeds. This property further enhances their applicability across AI data centers, enterprise AI infrastructure, edge AI devices, cloud computing platforms, and other data-intensive applications, thereby creating new growth opportunities. Moreover, the migration of artificial intelligence (AI) workloads from hyperscale data centers to enterprise-grade environments and the network edge is presenting growth opportunities.

- In August 2025, Kioxia Corporation launched a 5 TB High-Bandwidth Flash (HBF) memory module prototype that delivers 64 GB/s bandwidth using a PCIe 6.0 interface. The module offers high bandwidth with power consumption below 40 W and is designed for Mobile Edge Computing (MEC) servers, generative AI support solutions, IoT, and big data analytics, as it enables low-latency, high-capacity memory at the network edge.

- In February 2026, Sandisk Corporation and SK hynix collaborated to standardize high bandwidth flash (HBF) as a next-generation memory solution designed for the AI inference era. The companies will establish a dedicated workstream under the Open Compute Project (OCP) to advance HBF standardization efforts.

Additionally, the introduction of advanced QLC (Quad-Level Cell) and 200+ layer 3D NAND architectures is further transforming the NAND flash market dynamics in the U.S.

- In June 2026, Transcend launched a new range of industrial SSDs and memory cards built with 218-Layer 3D NAND storage solutions to support AI computing and edge applications. The offerings include high-performance PCIe Gen5 and Gen4 SSDs, delivering faster speeds, enhanced durability, and hardware encryption for secure and reliable data storage.

- In January 2026, Micron Technology launched the 3610 NVMe SSD, which is the first PCIe Gen5 G9 QLC SSD for client computing. The product is developed on the G9 NAND architecture and offers up to 11,000 MB/s sequential read speeds and 9,300 MB/s sequential write speeds, making it ideal for AI-capable devices.

NAND Flash Market Report Snapshot

|

Segmentation

|

Details

|

|

By Product Technology

|

SLC, MLC, TLC, QLC, Others

|

|

By Storage Capacity

|

Less than 128 GB, 128 GB - 512 GB, 512 GB - 2 TB, 2 TB - 8 TB, 8 TB - 30 TB, Greater than 30 TB

|

|

By Application

|

Internal Storage (eMMC-based Storage, UFS-based Storage, SSD, Others), Portable Storage (External SSDs, USB Flash Drives, SD Cards, microSD Cards, Others)

|

|

By End-Use Industry

|

Consumer Electronics (Smartphones, Tablets, PCs/Laptops, Gaming Consoles, Wearables & Cameras, Others), Enterprise IT, Cloud & Hyperscale, Automotive, Industrial & Telecom, Aerospace & Defense, Others

|

|

By Country

|

U.S.

|

Market Segmentation

- By Product Technology (SLC, MLC, TLC, QLC, and Others). The TLC segment captured the largest share of 61.50%, with an estimated valuation of USD 13.11 billion in 2025. The high demand for TLC NAND is attributed to its low cost and higher energy density, which lead to larger capacities and a lower cost per gigabyte.

- By Storage Capacity (Less than 128 GB, 128 GB - 512 GB, 512 GB - 2 TB, 2 TB - 8 TB, 8 TB - 30 TB, and Greater than 30 TB). The greater than 30 TB segment is likely to grow at the fastest CAGR of 20.74% over the forecast period, reaching USD 2.88 billion in 2033. The high growth rate is attributed to the rising adoption of AI infrastructure and data center build-outs, which handle massive data workloads and require high-density.

- By Application (Internal Storage (eMMC-based Storage, UFS-based Storage, SSD, and Others), Portable Storage (External SSDs, USB Flash Drives, SD Cards, microSD Cards, and Others). The internal storage segment garnered the highest share of 77.50% in 2025, with a valuation of USD 16.52 billion. The utilization of NAND flash in internal storage of smartphones, tablets, and consumer electronics to ensure quick app launches, high-capacity media storage, reliable data retention when powered off, and efficient portable data transfer contributes to its high share.

- By End Use Industry (Consumer Electronics (Smartphones, Tablets, PCs/Laptops, Gaming Consoles, Wearables & Cameras, and Others), Enterprise IT, Cloud & Hyperscale, Automotive, Industrial & Telecom, Aerospace & Defense, and Others). The automotive segment is anticipated to register the highest CAGR of 20.95% over the forecast period, reaching USD 5.90 billion in 2033. This growth is fueled by the notable shift toward autonomous and electrically powered vehicles, which require a centralized vehicle architecture equipped with high-performance, high-bandwidth, stable, and secure memory.

The U.S. is designated as a major hub for data centers, which drive artificial intelligence computing infrastructure. Artificial intelligence (AI) chips are crucial to training, deploying, and improving AI models. The demand for high computing power from AI companies is transforming the NAND flash memory market in the country.

The development of advanced LLMs and increasing applicability of generative AI across the commercial and industrial landscape of the U.S. further fuel the demand for high-capacity and high-speed storage solutions capable of handling rising computing workloads. Additionally, market players are operationalizing artificial intelligence, transitioning beyond pilot projects to embed AI directly into core business operations. This trend is propelling demand for efficient storage and processing solutions, thereby boosting the demand for NAND flash storage in the U.S.

- In March 2024, Western Digital Corporation announced the separation of its HDD and Flash businesses by creating two independent, market-specific companies. The move is aimed at positioning each business unit to foster innovative technology and product development.

Regulatory Frameworks

- The Semiconductor Superiority Act amends the CHIPS and Science Act and extends Section 48D tax credits to space-based semiconductor manufacturing. The Act is targeted at boosting U.S. investment in microgravity chip production and strengthening domestic semiconductor capabilities, improving supply chain resilience, and enhancing global competitiveness.

- The SEMI S2 guidelines specify requirements for maintaining chemical emissions from semiconductor equipment at extremely low levels, such as less than 1% of the American Conference of Governmental Industrial Hygienists (ACGIH) threshold limit value (TLV) or permissible exposure limit (PEL), during normal equipment operation.

Competitive Landscape

Key players operating in the U.S. NAND flash market are focusing on strategic mergers, acquisitions, and technical collaborations to strengthen their competitive positioning, capture a larger market share, and leverage NAND flash shortages in the U.S. Market players are prioritizing storage density enhancement through 3D NAND layer stacking and exhibiting extreme production discipline to maintain high margins.

For instance, Samsung reduced its annual NAND wafer target from 4.9 million to 4.68 million, while SK Hynix reduced its annual NAND wafer target from 1.9 million in 2025 to 1.7 million in 2026. This artificial tightening reflects the strategic allocation of limited wafer supply and helps keep NAND supply constrained.

- In February 2025, Samsung Electronics ceased 2D NAND flash production and converted the production facility into a back-end-of-line (BEOL) facility handling processes such as DRAM metallization.

Industry players are further phasing out legacy NAND production and adopting innovative memory architectures capable of handling AI workloads and advanced computing workloads.

- In February 2025, Samsung launched its 10th-generation V-NAND flash memory with over 400 active layers and a 5.6 GT/s interface speed.

- In February 2025, Kioxia and Sandisk unveiled their 10th generation 3D flash memory technology with a 4.8Gb/s NAND interface speed and enhanced power efficiency and density.

Key Companies In The U.S. NAND Flash Market:

- Exascend

- Kingston Technology

- KIOXIA Corporation

- Marvell

- Micron Technology, Inc.

- PATRIOT MEMORY, INC.

- PNY Technologies Inc.

- Samsung

- SanDisk Corporation

- Seagate Technology LLC

- SK Hynix Inc.

- Solidigm Inc.

- Transcend Information, Inc.

- Western Digital Corporation

- Winbond

Recent Developments

- In March 2025, SMART Modular Technologies, Inc. introduced a next-generation Non-Volatile CXL Memory Module (NV-CMM) to Tier 1 OEMs, based on the CXL 2.0 standard. The product combines high-performance non-volatile DRAM memory, persistent flash memory, and an energy source in a single removable EDSFF form factor to deliver superior reliability and serviceability for data-intensive applications.

- In November 2024, SK Hynix commenced the mass production of the first triple-level cell-based 321-high 4D NAND Flash with a 1Tb capacity. The product offers a 12% improvement in data transfer speed, 13% higher read performance, and 10% greater power efficiency during data reading.