Market Definition

The High Bandwidth Memory (HBM) market refers to the ecosystem of volatile storage technology with wide applications across AI/ML workloads, high-performance computing, and high-end graphics applications. The high bandwidth, and lower latency property of HBMs drives their adoption across cloud computing, and hyperscale data center infrastructure in the U.S. This is driving manufacturers to scale production and develop high-capacity, low-latency memory solutions for next-generation computing applications.

High Bandwidth Memory (HBM) Market Overview

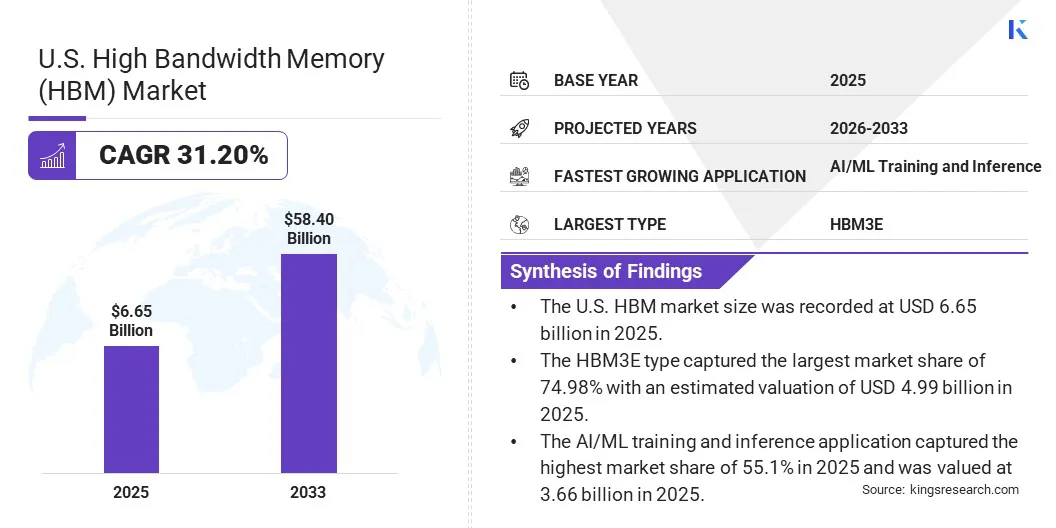

The U.S. High Bandwidth Memory (HBM) market size was valued at USD 6.65 billion in 2025 and is projected to reach USD 58.40 billion by 2033, representing a CAGR of 31.20% over the forecast period (2026-2033). HBMs are high-performance, high-throughput, massive-bandwidth architecture memory chips that are made by stacking DRAM dies on a base die to deliver memory bandwidth. The process results in the generation of a memory of high bandwidth, which is widely adopted across AI accelerators and high-performance computing (HPC) applications. Furthermore, the process is enabling DRAM manufacturers to allocate DRAM facilities towards HBM production owing to the high revenue per die yield of HBMs.

The evolution of AI memory chips to address high-speed data processing for AI training and inference is driving demand for HBM in the U.S. The integration of HBM with AI logic chips eliminates data bottlenecks, which enables large-volume, high-speed data transmission. The adoption of high-performance computing further positions HBM in a transformative state that addresses the critical bottleneck of memory bandwidth. HBM leverages advanced 2.5D and 3D architectures which enables delivery of massive throughput, high-power efficiency, improved thermal management, and scalability for next-generation workloads. The data transfer rate doubling to 16 Gb/s by HBM4E and enhanced reliability and flexibility position HBM as a critical part of AI, HPC, and data-intensive applications.

Key players operating in the market include SK Hynix Inc., Samsung Electronics, and Micron Technology, Inc., which capture more than 95% market share in 2026. The HBM market ecosystem is further driven by companies including NVIDIA, AMD, Intel Corporation, Rambus Inc. and others, which provide hardware and software solutions including AI accelerators, memory interface IP, HBM memory controllers, or high-speed interconnect technologies that drive HBM adoption across AI, HPC, and data center applications.

- In June 2026, Samsung and SK Hynix announced an investment of over USD 590 billion to expand High Bandwidth Memory (HBM) chip production. The plan involves four new chip manufacturing plants to address rising demand for AI and high-bandwidth memory (HBM) chips.

Key Market Highlights:

- The U.S. High Bandwidth Memory (HBM) market size was recorded at USD 6.65 billion in 2025.

- The market is projected to grow at a CAGR of 31.20% from 2026 to 2033.

- The HBM3E type captured the highest market share of 74.98% with an estimated valuation of USD 4.99 billion in 2025.

- The AI/ML training and inference application captured the highest market share of 55.1% in 2025 and was valued at USD 3.66 billion.

How is the deployment of AI training and inference infrastructure driving growth of High Bandwidth Memory (HBM) market in the U.S.?

Processors in the current generation are held back by their inability to access data quickly which hampers their adaptability in handling AI workloads, which include enormous datasets processing. The training of AI models by a GPU requires constant access to billions of data points, which results in memory delay, emphasizes processor idling and data waiting. HBM provides increased bandwidth (e.g. HBM3 delivers speeds up to 6.4 Gb/s) which reduces latency through stacked architecture, and improves power efficiency. Furthermore, their compact form is favorable for space-constrained applications.

The rise in hyperscale investments and high-performance computing applications in the U.S. drives the market growth of HBM for advanced GPUs and AI applications. Market players including Samsung Electronics, SK Hynix, and Micron Technology collectively capture a significant share of the global HBM market. The companies have directed research and production towards developing higher architectures of HBM to address rising demand for AI-optimized memory solutions.

Moreover, the exponential growth of AI accelerators across AI technology developers and cloud service providers requiring high-bandwidth memory to run computationally intensive machine learning and generative AI workloads further drives market growth. AI accelerators leverage predictable data access patterns through hardware techniques such as data prefetching to provide high memory bandwidth and low latency required to sustain these workloads efficiently. Companies including NVIDIA and Google are relying on HBM for their H100 and TPU v5p to feed massive transformer models.

- In July 2026, Perplexity declared adoption of Vera Rubin CPU of NVIDIA, which reports up to 1.5x faster performance for agentic coding workloads. The adoption by Perplexity is targeted at lowering inference costs and support the growing demand for AI-powered search and agentic features at scale.

- In May 2026, NVIDIA Corporation commenced full-scale production of its Vera Rubin platform, which acts as foundation for next-generation AI factories with up to 10x higher agent throughput than the previous Grace Blackwell platform.

- In March 2026, Micron Technology, Inc. announced the high-volume production of its HBM4 36GB 12H memory which is designed for Vera Rubin platform of NVIDIA. The product delivers over 2.8 TB/s bandwidth and improved power efficiency for AI workloads.

How is the HBM supply crisis poised to hamper AI infrastructure in the U.S.?

DRAM supply constraints are providing the suppliers pricing power in HBM market. The sharp rise in prices is attributed to limited supply, shifting manufacturing capacity allocation from DRAM towards high-bandwidth memory, and surging AI and data center demand. HBM consumes a disproportionate amount of advanced DRAM wafer capacity, which further involves extreme precision stacking process that is difficult to replicate or scale consistently. This results in lower yield and leads to limited supply.

Furthermore, the ramping up of HBM production capacities by SK Hynix, Samsung, and Micron, is leading to an average lead time of 12-18 months in deliveries, further causing supply concentration and limited production. Hence, market players gain significant pricing power, which leads to scaling up of prices by 20-40% year-over-year. The expansion of AI infrastructure reshapes this supply, pricing dynamics and investment strategies across the U.S. semiconductor industry. AI model training, deployments and inference workloads require high memory, which further increases reliance on high-performance GPUs that process large volumes of high-speed data to train and operate complex AI models.

To address the challenge and accelerate next-generation HBM production, manufacturers are expanding capacity, prioritizing AI-focused memory over conventional DRAM, adopting alternative technologies, and increasing investments in advanced packaging technologies.

- In June 2026, Qualcomm Technologies Inc. introduced Qualcomm High Bandwidth Compute (HBC) technology, which breaks memory wall with lower energy per token. HBC leverages a hybrid design stacking LPDDR memory in a 3D space thus offering power-efficient and massive amounts of bandwidth and up to 768GB of stacked memory for AI workloads.

- In April 2026, NEO Semiconductor demonstrated proof-of-concept for its 3D X-High Bandwidth Memory (HBM) technology by validating its manufacturability using existing 3D NAND fabrication infrastructure and achieving key HBM performance benchmarks.

- In December 2024, Marvell launched a new custom HBM compute architecture that enables XPUs to deliver more compute and memory density. The technology offers up to 70% lower interface power and 25% more savings compared to standard HBM interfaces.

How is the adoption of higher-bandwidth memories poised to create growth avenues in the U.S. HBM market?

The transition to higher HBM generations is attributed to the higher bandwidth delivery compared to conventional DDR memory. Each new HBM generation is designed to deliver roughly double the bandwidth of its predecessor. For instance, HBM3E delivers 896–1,280 GB/s bandwidth per stack with up to 48 GB capacity in 16-high configurations, which acts as the baseline for AI accelerators in 2026. This leads to lower latency, improved energy efficiency, and higher compute performance, resulting in faster AI model training and inference and further extending its applicability in next-generation AI accelerators and high-performance computing (HPC) workloads.

The deployment of AI models across commercial and industrial enterprises is further poised to fuel the demand for higher bandwidth memory chips. The demand is anticipated to be fueled by AI model requirements for higher memory bandwidth exceeding 1,000 GB/s to handle massive AI/ML workloads where HBM facilitates efficient data transfer between memory and processing units including GPUs, or AI accelerators.

- In March 2026, Samsung Electronics showcased the first physical model of its next-generation HBM5 memory at Computex 2026. The company has previously completed verification of HBM4E and is targeting mass production of HBM5 around 2028.

High Bandwidth Memory (HBM) Market Report Snapshot

|

Segmentation

|

Details

|

|

By Type

|

HBM2E, HBM3, HBM3E, HBM4, Others

|

|

By Application

|

AI/ML Training and Inference, High-Performance Computing (HPC), Gaming and Graphics, Others

|

|

By Country

|

U.S.

|

Market Segmentation

- By Type (HBM2E, HBM3, HBM3E, HBM4, Others). The HBM3E captured the highest market share of 74.98% with an estimated valuation of USD 4.99 billion in 2025. The higher memory bandwidth and improved power efficiency compared to older architectures contribute towards its applicability in next-generation AI accelerators and high-performance computing workloads.

- By Application (AI/ML Training and Inference, High-Performance Computing (HPC), Gaming and Graphics, Others). The AI/ML training and inference application is forecasted to capture the highest market share of 55.1% in 2025 with a valuation of USD 3.66 billion in 2025. The increasing deployment of AI accelerators and GPUs requiring high-bandwidth, low-latency memory to process large-scale AI models and data-intensive workloads fuels the segment growth.

What is the scenario in the U.S. High Bandwidth Memory (HBM) market?

The U.S. is designated as a premier hub for data centers and artificial intelligence (AI) computing infrastructure which fuels the market growth of high-performance computing hardware required to drive the workloads. The development of advanced LLMs and increasing Generative AI applicability across the commercial and industrial landscape of the U.S. further fuels high capacity and high-bandwidth memory chips. Commercial business entities are operationalizing AI by transitioning it beyond pilot projects and embedding it directly into the core business operations. This is driving the demand for high performance memory requirements, leading to growth avenues across the U.S. HBM market.

- In April 2026, the Semiconductor Equipment and Materials International (SEMI) projected investments exceeding USD 151 billion by 2027 in 300 mm memory fab equipment. The high demand is to be driven by strong AI-led demand for advanced memory technologies including HBM, DDR5, and 3D NAND. HBM equipment spending is further anticipated to reach USD 37 billion driven by rising adoption of AI accelerators and cloud infrastructure.

Regulatory Frameworks

- The SEMI S2 guidelines specify that chemical emissions from semiconductor equipment must be kept extremely low in the air, at less than 1% of the American Conference of Governmental Industrial Hygienists (ACGIH) threshold limit value (TLV) or permissible exposure limit (PEL) during normal equipment operation.

- The Semiconductor Superiority Act amends the CHIPS and Science Act and extends Section 48D tax credits to space-based semiconductor manufacturing. The Act is targeted at boosting the U.S. investment in microgravity chip production and strengthening domestic semiconductor capabilities, improving supply chain resilience, and enhancing global competitiveness.

Competitive Landscape

Key players operating in the market are expanding production capacities to strengthen their market position and capture a larger share of the growing AI memory market. Companies are further entering strategic partnerships with technology providers to accelerate HBM technology development, commercialization and secure long-term supply agreements to mitigate supply constraints and ensure uninterrupted access to high-bandwidth memory amid rising demand.

- In June 2026, NVIDIA signed a multi-year supply agreement with SK Hynix to co-develop next-generation memory technologies, including HBM4 for its future AI platforms. The partnership is aimed at addressing extended HBM development cycles, improve supply chain visibility, and ensure stable demand amid rapidly growing AI infrastructure requirements.

- In April 2024, SK Hynix released plans for the development of a HBM (High Bandwidth Memory) production line and advanced packaging R&D facility in West Lafayette, Indiana (U.S.) with an investment of USD 3.87 billion. The company received USD 458 million funding from S. Department of Commerce in direct funding under the CHIPS and Science Act and is scheduled to be operational by 2028.

Key Companies In The U.S. High Bandwidth Memory (HBM) Market:

- Micron Technology, Inc.

- SK Hynix Inc.

- Samsung Electronics Co., Ltd.

Other Ecosystem Players:

- Advanced Micro Devices, Inc.

- Amkor Technology, Inc.

- Applied Materials, Inc.

- ASE Technology Holding Co. Ltd.

- Broadcom Inc.

- Cadence Design Systems, Inc.

- GlobalFoundries Inc.

- Huawei Technologies Co., Ltd.

- Intel Corporation

- Marvell Technology, Inc.

- NVIDIA Corporation

- Powertech Technology Inc.

- Qualcomm Incorporated

- Rambus Inc.

- Siliconware Precision Industries Co. Ltd.

- Synopsys, Inc.

- Taiwan Semiconductor Manufacturing Company Limited

Recent Developments

- In June 2026, Samsung Electronics showcased its next-generation AI semiconductor portfolio including HBM4E, SOCAMM2, and AI-optimized SSDs, designed to support the complete AI memory and storage hierarchy. The company also introduced HBM4E with its new Heat Path Block (HPB) technology to improve thermal management, performance, and scalability for future AI workloads.

- In April 2026, Intel Corporation and SoftBank, through their subsidiary Saimemory, introduced HB3DM memory, which offers as an alternative technology to HBM. It is based on Z-Angle Memory (ZAM) technology and offers higher bandwidth and capacity for memory modules used with powerful AI accelerators.

- In March 2026, SK Hynix unveiled plans to procure USD 8 billion of extreme ultraviolet (EUV) equipment from Dutch chipmaker ASML Holding to address rising chip shortages. The move is attributed to rising demand in high-bandwidth memory (HBM) market thereby prompting memory makers to reallocate capacity away from conventional DRAM.

- In January 2026, Samsung Electronics and SK Hynix released plans to expand High-Bandwidth Memory (HBM) production capacity in 2026 to address rising demand from AI applications and data centers. The companies are investing in new fabrication facilities and infrastructure owing to the ongoing memory shortages driven by rapid AI growth.

- In September 2025, SK Hynix completed the development of its HBM4 memory which is designed for AI accelerators through the use of Advanced Mass Reflow Molded Underfill (MR-MUF) method. The memory features a 2,048-bit interface and 10 GT/s data transfer speed which exceeds JEDEC industry standards by 25%.

- In September 2025, Huawei Technologies introduced two self-developed HBM technologies notably HiBL 1.0 and HiZQ 2.0 which are planned to enhance the performance of its Ascend AI processors. The development is undertaken in response to the restrictions imposed on China in accessing foreign HBM chips.