Market Definition

The DRAM market refers to the ecosystem of volatile storage technology widely utilized in consumer electronics, automotive, and high-end computing applications. Its highly scalable, cost-effective, and fast performance drives its adoption across diverse end-use verticals in the U.S. The deployment of artificial intelligence (AI), cloud computing, and hyperscale data center infrastructure is creating growth avenues for the market, enabling manufacturers to scale capacity and develop high-capacity, low-latency memory solutions for next-generation DRAM applications.

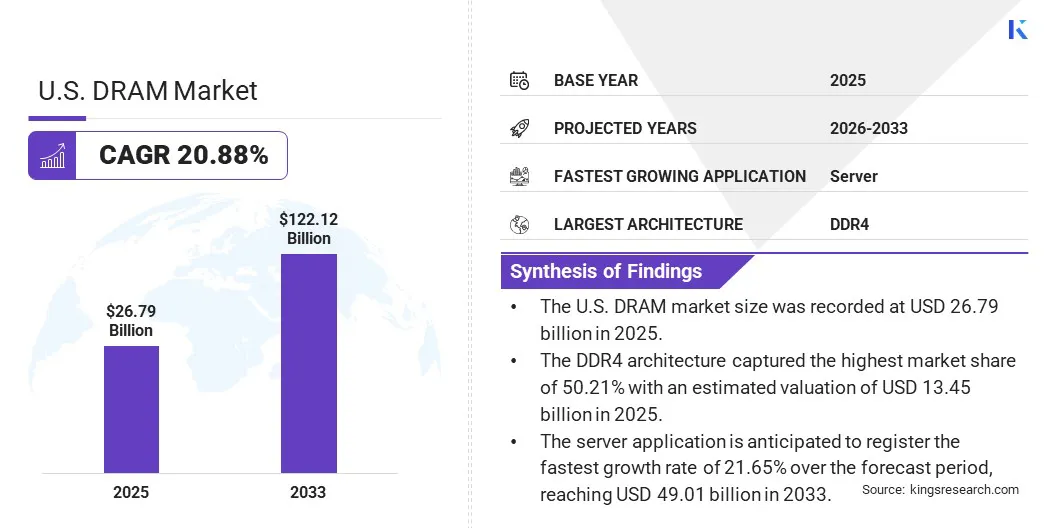

DRAM Market Overview

The U.S. DRAM market size was valued at USD 26.79 billion in 2025 and is projected to reach USD 122.12 billion by 2033, representing a CAGR of 20.88% over the forecast period. The market growth is driven by the surge in memory, such as LPDDR5 in AI data center infrastructure and cloud computing. The market is further driven by the growth in hyperscale data centers, which are pushing DRAM prices higher, resulting in the transforming market dynamics for DRAM in traditional computing and consumer electronics sector of the U.S.

Key players operating in the market include Micron Technology, Inc., Kingston Technology, SK Hynix Inc., Samsung Electronics, PNY Technologies Inc., Sabrent; PATRIOT MEMORY, INC., CORSAIR, Lexar, VisionTek, and others. Companies are planning to ramp up production by strategic capacity expansion in order to address the shortages in the DRAM supply across the U.S.

- In June 2026, Samsung and SK Hynix declared an investment of over USD 590 billion to expand DRAM chip production. The plan involves four new chip manufacturing plants to address rising demand for AI and high-bandwidth memory (HBM) chips.

- In May 2026, Micron Technology, Inc. commenced manufacturing of 1α (1-alpha) DRAM for critical industries, including automotive, defense and aerospace, industrial, networking and medical devices. The 1α node will increase DDR4 wafer supply four times at its Manassas (U.S.) facility, thus strengthening a reliable domestic supply of long-life DDR4 and LP4 memory for consumers.

Key Market Highlights:

- The U.S. DRAM market size was recorded at USD 26.79 billion in 2025.

- The market is projected to grow at a CAGR of 20.88% from 2026 to 2033.

- The DDR4 architecture captured the highest market share of 50.21% with an estimated valuation of USD 13.45 billion in 2025.

- The server application is anticipated to register the fastest growth rate of 21.65% over the forecast period, reaching USD 49.01 billion in 2033.

How is the adoption of artificial intelligence and data center expansion driving growth in the U.S. DRAM market?

AI training and inference workloads process enormous datasets, which creates unprecedented demand for enterprise-grade solid-state drives relying on advanced DRAM technologies. The expansion of AI computing infrastructure by major cloud service providers (CSPs) including Microsoft, Amazon, and Google to train Large Language Models (LLMs) further drives the demand for DRAM in the U.S. Inference AI workloads operate continuously to generate responses and predictions across millions of connected devices, which results in substantially higher requirements for memory bandwidth, storage capacity, and energy efficiency. This growing characteristic creates demand for DRAM technologies that offer high-speed performance with minimal power consumption.

Additionally, the ability of DRAM to provide temporary, high-speed memory; handle multiple workloads; and facilitate smooth operations in complex contexts, including AI processing or high-performance computing, drives their applicability. Diverse DRAM technologies are identified as ideal for cloud computing, real-time data analysis, GDDR in high-performance graphics, AI workloads, and autonomous vehicles. Advanced DRAM technologies as LPDDR5X further find applications in mobile, edge devices, wearable tech, leading to their increased demand in the U.S.

- In June 2026, Micron Technology, Inc. and General Motors signed a strategic customer agreement to secure a long-term supply of automotive memory and storage for next-generation vehicle platforms of GM. The deal covers LPDRAM, NOR, and UFS NAND, supporting AI-enabled in-cabin experiences, ADAS, and software-defined vehicles.

How is the price hike in DRAM negatively impacting the U.S. market?

The sharp rise in DRAM prices in the global semiconductor industry is attributed to constrained supply, shifting manufacturing capacity allocation, and surging AI and data center demand. The DRAM market is driven by the rapid expansion of AI infrastructure, which is reshaping supply dynamics, pricing, and investment strategies across the U.S. semiconductor industry. AI model training, deployments and inference systems lead to increased memory requirements, as high-performance GPUs rely on large volumes of high-speed memory to process complex AI models. This accelerates demand for advanced memory technologies and influences capacity allocation across the global memory market.

Chipmakers are reallocating wafer capacity towards more profitable AI-related memory products, including HBM (High Bandwidth Memory), thereby tightening the DRAM supply. Samsung Electronics, SK hynix, and Micron Technology collectively account for more than 95% of the global DRAM market and have tightened DRAM supply owing to shifting production capacity towards high-margin, high-bandwidth memory (HBM) for AI servers. This is enabling tech firms to shift DRAM procurement from Samsung Electronics, SK Hynix, and Micron to alternative low-cost domestic DRAM manufacturers in the U.S. Additionally, the U.S. declaration to include DRAM process equipment below 18 nanometers in export controls to China further leads to restricted technology access, price escalations, and increased supply-chain disruptions in the global DRAM and memory ecosystem.

To address the challenge, market players are transitioning towards adopting high-margin AI memory products such as High Bandwidth (HBM) while reducing emphasis on conventional DRAM output. Companies are further investing in advanced process technologies and expanding next-generation fabrication capacity to enhance production.

- In April 2026, NEO Semiconductor demonstrated proof-of-concept for its 3D X-DRAM technology by validating its manufacturability using existing 3D NAND fabrication infrastructure and achieving key DRAM performance benchmarks.

How is the adoption of high-bandwidth memory emerging as a notable DRAM market trend in the U.S. market?

HBM is a high-performance, low-latency architecture built from stacks of advanced DRAM. Their demand in the U.S. is fueled by AI accelerator production and hyperscaler capital investment cycles, which have different cyclical dynamics than conventional PC and smartphone DRAM demand. Chipmakers are transitioning towards HBM to provide the massive amounts of memory required for AI applications. Moreover, the low pricing volatility of HBM compared to commodity DRAM and low latency and fast random data access of DRAM are less crucial for AI inference, as AI workloads follow predictable data access patterns and reduce delays using techniques such as data prefetching. This is leading to new growth opportunities for the HBM memory architectures in the U.S. DRAM market. Additionally, the migration of artificial intelligence (AI) workloads from hyperscale data centers to enterprise-grade and network edge is creating new growth avenues for HBM memory in the U.S.

- In March 2026, Micron Technology, Inc. announced the high-volume production of its HBM4 36GB 12H memory, which is designed for the Vera Rubin platform of NVIDIA. The product delivers over 2.8 TB/s bandwidth and improved power efficiency for AI workloads.

DRAM Market Report Snapshot

|

Segmentation

|

Details

|

|

By Architecture

|

DDR4, DDR5, Others

|

|

By Application

|

Gaming Console, PCs/Laptop, Automotive, Mobile Phone, Server, Others

|

|

By Country

|

U.S.

|

Market Segmentation

- By Architecture (DDR4, DDR5, others). The DDR4 captured the highest market share of 50.21% with an estimated valuation of USD 13.45 billion in 2025. The low cost compared to DDR5 and the reliance of enterprise, industrial, and automotive systems on hardware compatible with DDR4 fuel its demand.

- By Application (Gaming Console, PCs/Laptop, Automotive, Mobile Phone, Server, Others). The server application is forecasted to register the highest growth rate of 21.65% over the forecast period, reaching USD 49.01 billion valuation. The combined effect of surging AI demand and supply contraction is driving demand for DRAM for AI servers in the U.S market.

What is the scenario in the U.S. DRAM market?

The U.S. is designated as a premier hub for data centers, which drives the artificial intelligence (AI) computing infrastructure. AI chips are crucial to train, deploy, and improve AI models. The development of advanced LLMs and increasing generative AI applicability across the commercial and industrial landscape of the U.S. further fuels high-capacity and fast memory processing chips capable of handling the computing workloads. Additionally, market players are operationalizing AI, enabling its transition beyond pilot projects towards embedding it directly into the core business operations. This further drives the demand for efficient data processing solutions, creating growth avenues for DRAM in the U.S. market.

- In April 2026, the Semiconductor Equipment and Materials International (SEMI) projected investments exceeding USD 151 billion by 2027 in 300 mm memory fabrication equipment. The high demand is driven by strong AI-led demand for advanced memory technologies, including HBM, DDR5, and 3D NAND. DRAM equipment spending is further anticipated to reach USD 37 billion, driven by rising adoption of AI accelerators and cloud infrastructure.

Regulatory Frameworks

- The SEMI S2 specifies guidelines for maintaining chemical emissions from semiconductor equipment to be kept in the air extremely low, as less than 1% of the American Conference of Governmental Industrial Hygienists (ACGIH) threshold limit value (TLV) or permissible exposure limit (PEL) during normal equipment operation.

- The Semiconductor Superiority Act amends the CHIPS and Science Act and extends Section 48D tax credits to space-based semiconductor manufacturing. The Act is targeted at boosting the U.S. investment in microgravity chip production, strengthening domestic semiconductor capabilities, improving supply chain resilience, and enhancing global competitiveness.

Competitive Landscape

Key players operating in the market are incorporating strategic mergers, acquisitions, and technical collaborations to strengthen their competitive positioning and capture a larger share of the market. The players are prioritizing the development of new DRAM production facilities to address rising demand from end-use verticals comprising industrial, automotive and information technology. The market is witnessing enhanced focus on supply chain localization and long-term capacity planning to improve stability and reduce disruptions. Additionally, companies are engaging in strategic partnerships and new players are marking entry in the highly competitive DRAM market of the U.S.

- In May 2026, ASUSTeK Computer Inc. launched its first ROG-branded DDR5 RAM kit, thus marking a strategic expansion during a period of global memory shortage. The product developed with Biwin features enthusiast-grade specifications, including EXPO/XMP support, and an exclusive “ROG Mode” for one-click overclocking up to DDR5-8000.

- In January 2026, Micron Technology, Inc. signed a Letter of Intent for the acquisition of the P5 fabrication site of PSMC in Tongluo, Taiwan, for USD 1.8 billion. The acquisition is targeted at expanding the DRAM production and addressing rising global demand for memory solutions.

Key Companies In The U.S. DRAM Market :

- Micron Technology, Inc.

- Kingston Technology

- SK Hynix Inc.

- Samsung

- PNY Technologies Inc.

- Sabrent

- PATRIOT MEMORY, INC.

- Transcend Information, Inc.

- AXIOM

- CORSAIR

- Exascend

- Lexar

- VisionTek

- Mushkin Enhanced MFG

- Eltron Technology, Inc.

Recent Developments

- In March 2026, SK Hynix unveiled plans to procure USD 8 billion of extreme ultraviolet (EUV) equipment from Dutch chipmaker ASML Holding to address rising chip shortages. The move is attributed to intensifying competition in high-bandwidth memory (HBM) prompting memory makers to reallocate capacity away from conventional DRAM.

- In March 2026, V-Color launched new 1+1 DDR5 Value Pack memory kits, which include one functional DDR5 DIMM and one RGB dummy module. The products are available in 16GB and 24GB modules, giving systems the appearance of dual-channel memory.