Market Definition

Sustainable packaging refers to the use of materials that are environmentally friendly such as paper, recycled plastics, and metal to reduce environmental harm. It is an amalgamation of hard and soft formats in the primary, secondary, and tertiary layers across food, healthcare, and retail sectors. The market includes recyclable, reusable, and biodegradable processes in order to spur resource efficiency and support the global circular economy.

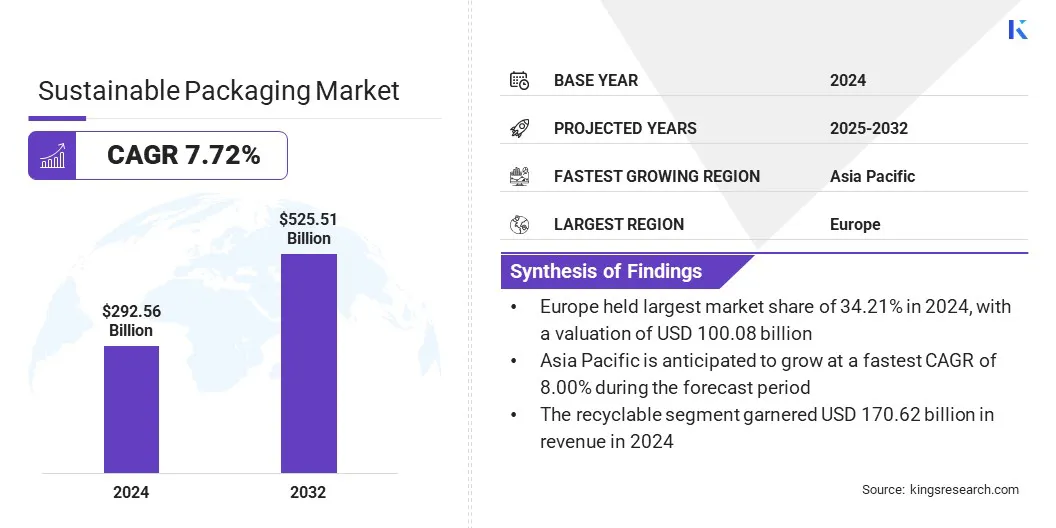

Sustainable Packaging Market Overview

The global sustainable packaging market size was valued at USD 292.56 billion in 2024 and is projected to grow from USD 312.31 billion in 2025 to USD 525.51 billion by 2032, exhibiting a CAGR of 7.72% during the forecast period. This expansion is fueled by the fact that packaging producers and brand owners are compelled to fulfill stringent compliance demands imposed by global environmental regulations and single-use plastic prohibitions.

Meanwhile, the market is experiencing a major trend in the development of barrier designs for humidity-sensitive goods, as high-performance mono-materials are substituting laminates.

Major companies operating in the global sustainable packaging market are Huhtamaki, 3M, Nampak Ltd., ITC Limited, Stora Enso, Smurfit Westrock, Crown Holdings, Inc., Packmile Pvt. Ltd., Ball Corporation, Tetra Pak International S.A., Elopak AS, NaturTrust, UPM Global, Amcor Group, and Mondi.

There is an uptake of more complex manufacturing methods by companies to manufacture ultra-thin high-strength packaging steel. These improvements aim at decreasing the weight of the steel packages without compromising high standards of structural strength and product barrier properties required for food and aerosol applications. They contrast with traditional steel production techniques, which in many cases led to heavier packaging and increased carbon footprints at the time of transportation.

Hydrogen-based steelmaking and electric arc furnace technologies are being embraced by the sustainable packaging sector, as producers strive to provide low-carbon steel technology, making this a widely used initiative in metal packaging.

- In January 2026, Tata Steel Nederland installed a new production line of sustainable packaging steel using its patented Trivalent Chromium Coating Technology (TCCT). The plant creates environmentally friendly materials that meet future REACH regulation requirements on chemical substances and do not require more layers of lacquer during manufacturing.

Key Market Highlights

- The global sustainable packaging market size was USD 292.56 billion in 2024.

- The market is projected to grow at a CAGR of 7.72% from 2025 to 2032.

- Europe held a share of 34.21% in 2024, valued at USD 100.08 billion.

- The paper & paperboard segment garnered USD 172.35 billion in revenue in 2024.

- The rigid segment is expected to reach USD 303.05 billion by 2032.

- The primary packaging segment is projected to generate USD 259.42 billion by 2032.

- The recyclable segment is likely to reach USD 303.05 billion by 2032.

- The food & beverages segment is estimated to register a revenue of USD 270.78 billion by 2032.

- The Asia-Pacific is anticipated to grow at a CAGR of 8.00% over the forecast period.

How is the increasing regulatory pressure influencing the adoption of eco-friendly solutions?

The sustainable packaging market is expanding steadily to fulfill the demand for compliance with global environmental mandates and single-use plastic bans. This demand helps businesses mitigate financial risks, including non-compliance penalties, plastic taxes, and waste management costs. To meet increasing regulatory pressure, companies are launching innovative offerings that prioritize material circularity and standardized recycling benchmarks. These developments improve efficiency across the supply chain and serve as the foundation for national zero-waste initiatives and advanced manufacturing.

- In June 2025, Mondi and Saga Nutrition announced their partnership to launch a new recyclable mono-material packaging solution for dry pet food. The collaboration focused on changing traditional non-recyclable materials with the re/cycle FlexiBag, ensuring freshness of the product and also supporting a circular economy by meeting CEFLEX recycling guidelines.

How are high material costs and supply chain volatility negatively impacting the sustainable packaging market?

The market is facing major challenges due to the high cost of post-consumer recycled (PCR) resins and bio-based feedstock. Because such materials need specialized collection and sophisticated chemical treatment, they are more likely to be priced at a premium compared to traditional virgin plastics. The scarcity of food-grade recycled content also poses bottlenecks in the supply chain, thus making it hard to scale production.

To address these issues, manufacturers are relying on long-term sourcing contracts and investing in vertically integrated recycling facilities to ensure the stable supply of raw materials. They are also adopting advanced technologies in recycling low-quality waste into high-quality resins using light-weighting techniques to decrease material usage. Companies are reducing price barriers and making sustainable solutions more economically viable by designing their packaging to be more material-efficient and collaborating on circular collection systems.

How do the advancements in barrier design for humidity-sensitive goods reshape the sustainable packaging market?

One of the trends in the sustainable packaging industry is the growing popularity of high-performance mono materials and bio-coating to shield delicate products. These superior designs are designed to protect commodities like food and pharmaceuticals against moisture and environmental degradation. They do not resemble conventional multi-layer laminates that are hard to separate and recycle because of their complicated chemical structure.

The market is increasingly relying on the use of new barrier technologies, as they provide global brands with alternatives to non-recyclable foils, namely compostable or fiber-based solutions. These solutions are also becoming a universally adopted innovation in the industry to guarantee the shelf life of products and achieve the goals of the circular economy.

- In June 2025, Mondi launched a high-performance re/cycle PaperPlus Bag Advanced, which is a paper bag designed to cushion humidity-sensitive goods with less plastic content. This solution has a 20 um barrier film which shields powdery products and has 60 percent less plastic than other 50 um variants. The packaging, developed in cooperation with UZIN, is also recyclable based on CEPI and 4Evergreen standards and can be fitted to existing industrial filling and sealing lines.

Sustainable Packaging Market Report Snapshot

|

Segmentation

|

Details

|

|

By Material

|

Paper & Paperboard, Plastics, Glass, Metal

|

|

By Type

|

Rigid, Flexible

|

|

By Packaging

|

Primary Packaging, Secondary Packaging, Tertiary Packaging

|

|

By Process

|

Recyclable, Reusable, Biodegradable

|

|

By Application

|

Food & Beverages, Personal Care & Cosmetics, Healthcare, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Material (Paper & Paperboard, Plastics, Glass, and Metal): The paper & paperboard segment earned USD 172.35 billion in 2024, mainly due to its high recyclability, biodegradable properties, and its extensive use as an alternative to single-use plastic, which is sustainable. Retailers and e-commerce providers prefer to use these materials because they enable them to lower their carbon footprints without compromising structural integrity during transit.

- By Type (Rigid and Flexible): The rigid segment held a share of 47.81% in 2024, as the material has better protection and strength for use in heavy-duty food, beverage, and medical industries. Hard surfaces such as glass jars, metal cans, and durable plastic containers offer a great deal of protection against contamination and physical damage.

- By Packaging (Primary Packaging, Secondary Packaging, and Tertiary Packaging): The Primary Packaging segment is projected to reach USD 259.42 billion by 2032, owing to the rising demand for sustainable materials, which directly interact with consumer goods. With increasing safety regulations, manufacturers are putting their money into new bio-coatings and resins with recycled content to be chemical safe and moisture-proof.

- By Process (Recyclable, Reusable, and Biodegradable): The recyclable segment is projected to reach USD 303.05 billion by 2032, owing to the introduction of strong global recycling systems and the implementation of mandatory recycling laws. The majority of waste management systems, which are international, are optimized for mechanical and chemical recycling, so recyclable mono-materials are the most economically feasible option for large-scale production.

- By Application (Food & Beverages, Personal Care & Cosmetics, Healthcare, and Others): The food & beverages segment is projected to reach USD 270.78 billion by 2032, owing to the highly eco-friendly nature of the solutions demanded by the segment, which have to adhere to strict food-contact safety and hygiene standards. The high increase in the takeaway and packaged food industries has increased the need to find better alternatives to traditional service ware such as compostable and plastic-free options.

What is the market scenario in Asia Pacific and Europe?

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

The Europe sustainable packaging market accounted for a substantial share of 34.21% in 2024, with a valuation of USD 100.08 billion. This dominance is reinforced by the high concentration of key industry players who are strategically adopting circular economy practices to comply with strict regional environmental requirements. These companies are at the forefront of the shift to incorporate closed loop systems and modern recycling into their business models.

The leadership in the region is also driven by the existence of a well-established network of producers and brand owners that focus on material recovery and the reduction of single-use plastics to gain a competitive edge in the global market.

- In July 2025, Mars Inc. announced the launch of its new recyclable mono-polypropylene pouches under the WHISKAS brand in the UK and Germany. By converting the traditional multi-material packaging into this mono-material solution, which is heat resistant, high temperature sterilization can be performed, and recycling infrastructure compatibility is enhanced. The carbon footprint of the packaging is reduced by 46 percent through this innovation, contributing to the overall Sustainable in a Generation Plan, which aims to help the company progress toward a circular economy.

The Asia-Pacific sustainable packaging market is expected to register the fastest CAGR of 8.00% over the forecast period. This growth is attributed to the high concentration on localized innovation and the rapid expansion of manufacturing plants that focus on sustainable packaging production.

Emerging economies are increasing their industrial potential to generate biodegradable substitutes and high-grade recycled resins in order to achieve growing domestic and foreign demand. Moreover, conversion plants are being upgraded on a large scale, positioning the region as a global center of cost-effective and environmentally friendly solutions in the e-commerce and consumer goods industries.

- In October 2025, Henkel and the China Packaging Federation announced the opening of RecycLab in Shanghai, a dedicated establishment to promote localized sustainable packaging innovation. The collaboration aims at testing adhesive solutions and modeling industrial recycling to reinforce design-for-recycling systems. This effort will help to speed up the transition to a circular economy by providing crucial data to optimize packaging and fostering a shared ecosystem.

Regulatory Frameworks

- In the U.S., the SB 54 of California mandates that all packaging become recyclable or compostable by 2032 and requires producers to finance state recycling programs. The FTC Green Guides offer federal enforcement to prevent misleading environmental claims, whereby the biodegradable labels are subject to verified scientific standards.

- In Europe, the European Union has a law on packaging and packaging waste known as the Packaging and Packaging Waste Regulation (PPWR), but the current law is shifting toward mandatory requirements, under which 100% recyclability of packaging needs to be achieved by 2030. This framework proposes serious Recyclability Performance Grades and establishes particular targets for recycled content in plastic beverage bottles and contact-sensitive packaging.

- In China, a staged ban on non-degradable single-use plastics has been enforced in the retail and catering industries by the National Development and Reform Commission (NDRC). The new Green Packaging Standards specifically target the e-commerce sector and introduce restrictions on over-packaging, along with promoting the adoption of reusable delivery boxes.

- The Plastic Waste Management Rules in India include a centralized digital portal, where a brand and a manufacturer are subject to the Extended Producer Responsibility (EPR). The amendments of 2022 have created a complete prohibition of 19 high-littering plastic objects and set increasing targets for the mandatory use of post-consumer recycled resin.

- In Japan, the Plastic Resource Circulation Act (2022) promotes design-for-environment principles, which require businesses to voluntarily cut down on 12 types of single-use plastics. This system has an integrated linkage with the Container and Packaging Recycling Law, which allocates recycling costs between the private sector and local municipalities.

Competitive Landscape

Major players operating in the sustainable packaging sector are actively establishing international contacts and increasing investments in capital and material science to achieve a competitive edge. Large-scale producers are working with biopolymer producers to incorporate renewable feedstock, which allows the creation of high-performance carbon-neutral substitutes for conventional plastics.

Simultaneously, the providers of packaging solutions are commercializing sophisticated recycling infrastructure, automated sortation systems, and closed-loop logistics to fast-track the shift to a fully circular economy. Such investments and expansion of global footprints assist in strengthening supply chains, moving to zero-waste requirements, and accelerating the implementation of plastic-free solutions in the global markets.

- In February 2026, Wipak launched its 2030 business model that incorporates both sustainability and digital innovation across the food and healthcare packaging industries. The roadmap aims at the reduction of carbon emissions, expansion of circular economy designs, and enhancement of DigitalChoice technology to improve supply chain transparency and recycling processes. The initiative will lower material complexity and enhance the global footprint of the company in Europe and Asia, supported by approximately USD 218 billion of recent asset and infrastructure investments.

Key Companies In Sustainable Packaging Market

- Huhtamaki

- 3M

- Nampak Ltd.

- ITC Limited

- Stora Enso

- Smurfit Westrock

- Crown Holdings, Inc.

- Packmile Pvt. Ltd.

- Ball Corporation

- Tetra Pak International S.A.

- Elopak AS

- NaturTrust

- UPM Global

- Amcor Group

- Mondi

Recent Developments (Partnerships/Agreements/New Product Launch)

- In March 2026, Siegwerk revealed HorizonNOW 2030, the next phase of its sustainable business agenda. Building on its 2021 HorizonNOW strategy, the project defines quantifiable targets in procurement, operations, and product development. It ensures that at least 65 percent of its products will support its circular packaging initiative by the year 2030.

- In July 2025, Huhtamaki launched a new brand of compostable ice cream cups, which adds to its international range of sustainable food packaging. The new product is made of certified paperboard with a bio-based coating to significantly decrease the use of fossil-based plastics. The cups are designed to be both recyclable and compostable at home and industrial levels and are expected to aid the industry in transitioning to a circular economy.

- In December 2025, Tetra Pak and Garcia Carrion announced that they would work together to introduce a paper-based barrier for juice packaging. The collaboration launched the Tetra Brik Aseptic carton, which is used in the Don Simon brand, with a design that replaces aluminum foil with sustainable fiber and plant-based polymers. The innovation makes the packing material 92 percent renewable and reduces the carbon footprint relative to conventional aseptic containers.

- In April 2024, Amcor and Kimberly-Clark announced their collaboration on a new packaging solution for Huggies Eco Protect diapers in Peru. The joint venture aims to create a flexible plastic bag with a 30 percent post-consumer recycled (PCR) content that will facilitate a circular economy.