Market Definition

The market includes materials and solutions designed to protect, contain, and transport products safely across supply chains and end-use applications. These packaging solutions offer strength, durability, and barrier protection to prevent damage, contamination, or product loss during storage and transportation.

The report covers segmentation by packaging type, material, end-use industry, and region. Paper and paperboard packaging solutions are widely used across consumer goods, food and beverage, e-commerce, industrial, and public sector applications. These solutions ensure product safety, meet regulatory standards, support sustainability goals, and reduce operational and environmental risks.

Paper and Paperboard Packaging Market Overview

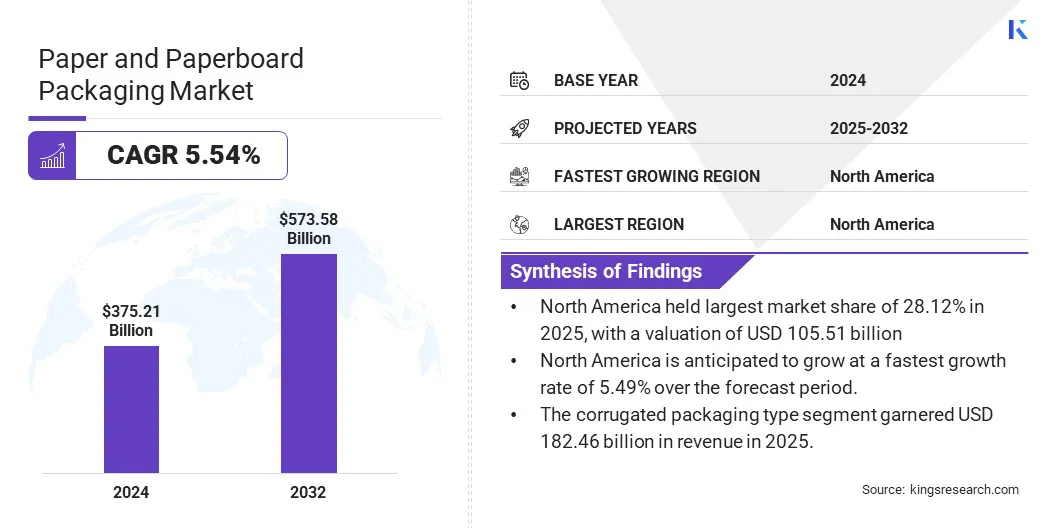

The global paper and paperboard packaging market size was valued at USD 375.21 billion in 2025 and is projected to grow from USD 393.26 billion in 2026 to USD 573.58 billion by 2032, exhibiting a CAGR of 5.54 % over the forecast period (2026-2033).

Market growth is primarily driven by the rising demand for sustainable and recyclable packaging, increased usage across food & beverage, e-commerce, and consumer goods sectors, and growing regulatory and consumer emphasis on eco-friendly, lightweight, and circular packaging solutions.

Major companies operating in the paper and paperboard packaging industry are Mondi, International Paper, Smurfit Westrock, DS Smith, Packaging Corporation of America, Stora Enso, Georgia-Pacific LLC, Oji Holdings Corporation, Rengo Co., Ltd., Saica, Mayr-Melnhof Karton AG, Cascades Inc., Novolex, Amcor plc, and YFY Inc.

The market is experiencing notable growth, mainly due to the increasing adoption of paper mailers, corrugated boxes, and paper fillers across large-scale logistics and fulfillment operations in order to structurally reduce plastic usage while improving packaging efficiency.

- In July 2025, Amazon reported a 28% reduction in North American shipments containing single-use plastic packaging, as outlined in its 2024 sustainability report. This reflects a strategic shift toward paper-based packaging solutions. The company increased the use of paper mailers, cardboard boxes, and paper fillers, and retrofitted automated packing systems to support made-to-fit paper packaging.

Key Highlights:

- The paper and paperboard packaging market size was recorded at USD 375.21 billion in 2025.

- The market is projected to grow at a CAGR of 5.54% from 2026 to 2033.

- North America held a share of 28.12% in 2025, valued at USD 105.51 billion.

- The corrugated packaging segment generated USD 182.46 billion in revenue in 2025.

- The recycled paper/ paperboard material segment is expected to reach USD 111.33 billion by 2033.

- The food and beverage end-use industry is anticipated to witness the fastest CAGR of 6.9% over the forecast period.

- Europe is anticipated to grow at a CAGR of 5.49% through the projection period.

How are regulatory restrictions on single-use plastics driving demand for paper and paperboard packaging?

Regulatory restrictions on single-use plastics are accelerating the transition to paper and paperboard packaging by limiting or banning plastic-based formats across key markets. As governments promote recyclable, biodegradable, and renewable materials, brands are increasingly adopting paper-based alternatives to ensure regulatory compliance and sustain consumer acceptance.

This regulatory push, combined with rising demand for sustainable packaging, is boosting adoption across end-use industries such as food and beverage, e-commerce, pharmaceuticals, consumer goods, and industrial packaging. Growth in e-commerce, demand for lightweight and cost-efficient materials, and advancements in paperboard strength, barrier properties, and printing technologies are further supporting this shift.

- In December 2025, Tetra Pak partnered with García Carrión to launch the first juice carton with a paper-based barrier. The Tetra Brik Aseptic carton contains up to 92% renewable content and achieves a 43% lower carbon footprint than conventional aseptic cartons, highlighting the need for advanced paper-based packaging solutions.

How is raw material price volatility impacting the paper and paperboard packaging market?

Raw material prices are highly sensitive to changes in forestry regulations, energy and logistics costs, recycling rates, and global supply–demand dynamics, creating cost uncertainty for manufacturers. This volatility pressures margins and complicates long-term pricing strategies, particularly for high-volume and price-sensitive end-use industries such as food, e-commerce, and consumer goods.

To mitigate this challenge, market players are securing long-term supply agreements, increasing the use of recycled fiber, optimizing material usage through light weighting and process efficiency improvements, and investing in automation and energy-efficient technologies. Some companies are prioritizing vertical integration and supplier diversification to reduce exposure to raw material price fluctuations.

How is the shift toward sustainable and smart packaging innovations positively influencing the paper and paperboard packaging market?

The increasing adoption of sustainable, recyclable, and smart packaging solutions is a key trend propelling the market, as it aligns with evolving regulatory requirements and changing consumer preferences. The rising use of sustainable coatings, biodegradable inks, and higher recycled fiber content is further supporting this trend, enabling manufacturers to meet environmental regulations while maintaining performance standards.

At the same time, the integration of smart and functional features such as QR codes, digital watermarks, and NFC tags is enhancing product traceability, strengthening anti-counterfeiting measures, and improving consumer engagement. These innovations add value for brand owners, support transparency across supply chains, and expand the application scope of paper and paperboard packaging, thereby reinforcing long-term market growth.

- In August 2025, Graphic Packaging International launched CleanClose paperboard laundry pod packaging with ChildBlock, the first certified child-resistant, curbside-recyclable solution made with 50% recycled fiber. This innovation replaces conventional plastic and advances sustainability and functionality in paperboard packaging.

Paper and Paperboard Packaging Market Report Snapshot

|

Segmentation

|

Details

|

|

By Packaging Type

|

Folding Cartons & Boxes, Corrugated Packaging, Sleeves and Wraps, Others

|

|

By Material

|

Virgin Paper/ Paperboard, Recycled Paper / Paperboard, Others

|

|

By End-Use Industry

|

Food and Beverage, Consumer Goods, Healthcare, E-Commerce & Retail, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Packaging Type (Folding Cartons & Boxes, Corrugated Packaging, Sleeves and Wraps, and Others). The corrugated packaging segment accounted for the highest share of 48.63% in 2025 and is anticipated to grow at a CAGR of 4.21% over the forecast period. The high share is largely attributed to its strength, durability, versatility, and ability to protect goods during transport, support customization, meeting e-commerce and retail demand.

- By Material (Virgin Paper/ Paperboard, Recycled Paper / Paperboard, and Others). The recycled paper/paperboard segment is estimated to register a CAGR of 5.16% over the forecast period. This growth is propelled by the cost-efficiency, scalability, and flexible applicability of recycled paper/paperboard across diverse end-use sectors to implement eco-conscious and cost-effective packaging.

- By End-Use Industry (Food and Beverage, Consumer Goods, Healthcare, E-Commerce & Retail, and Others). The food and beverage segment is projected to grow at a CAGR of 6.90% over the forecast period. primarily fueled by the increasing demand for sustainable and eco-friendly packaging solutions in food products to ensure product safety, extend shelf life, and enhance consumer convenience.

What is the market scenario in North America and Europe region?

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

The North America paper and paperboard packaging market share stood at 28.12% in 2025 and is anticipated to grow at a CAGR of 6.88% over the forecast period. This growth is mainly propelled by strong demand for sustainable packaging solutions from the food and beverage, e-commerce, retail, and consumer goods sectors.

This rising demand is further boosted by high disposable incomes, expanding retail and e-commerce infrastructure, and increasing consumer preference for sustainable and recyclable packaging solutions. Additionally, rising environmental awareness and regulatory initiatives promoting eco-friendly packaging practices are further boosting the adoption of paper and paperboard materials across industries in North America.

- In November 2025, International Paper (IP) acquired DS Smith as part of a broader strategic expansion. The initiative included the construction of a new box plant in Waterloo, Iowa, and a USD 250 million investment in the Selma, Alabama containerboard mill, aimed at promoting sustainable packaging and improving customer value in North America.

The Europe paper and paperboard packaging industry is projected to grow at a CAGR of 5.49% over the forecast period. This growth is fostered by rapid urbanization, rising disposable incomes, expanding e-commerce and logistics activities, and stricter regulations on plastic packaging across the UK, Germany, France, and other European countries.

The surge in consumer awareness regarding sustainable and recyclable packaging solutions, along with government initiatives promoting eco-friendly materials, and the growing manufacturing base are contributing to higher adoption of durable, cost-effective paper and paperboard packaging.

- In June 2025, the UK revised the Plastic Packaging Tax rate, raising the rate to USD 9 per tonne for plastic packaging containing less than 30% recycled content. This change compels companies to reassess packaging strategies to reduce costs and align with sustainability goals.

Regulatory Frameworks

- In the U.S., the FDA Food Contact Regulations (21 CFR 176.170 & 176.180) 176.170 of Title 21 CFR regulates the safe use of substances as components in paper and paperboard contacting aqueous and fatty foods. The regulation permits listed substances that include GRAS (Generally Recognized as Safe) items, prior-sanctioned materials, and those with specific limitations on food-contact surfaces, often exempting them from extractives testing if compliant.

- In Europe, the EU Directive 94/62/EC harmonizes packaging and packaging waste regulations to protect the environment while safeguarding the internal market. It applies to all packaging and packaging waste, defines primary, secondary, and tertiary packaging levels, and sets essential requirements focused on waste prevention, minimized volume and weight, and improved reusability and recoverability.

- In India, Food Safety and Packaging Regulations govern food packaging materials to ensure safety and quality. The regulation mandate that all primary food-contact packaging be food-grade, and compliant with prescribed Indian Standards, including Schedules I-III covering paper and board, metals, and plastics.

Competitive Landscape

Companies operating in the paper and paperboard packaging industry are investing heavily in research and development to create advanced packaging solutions that are more sustainable, lightweight, and compliant with global environmental regulations. They are focusing on innovations such as high-barrier paper structures, eco-friendly coatings, biodegradable inks, and higher recycled fiber content to improve performance while reducing environmental impact.

Additionally, players are incorporating digital and smart packaging technologies, including QR codes, digital watermarks, and NFC-enabled features into paperboard packaging to improve traceability, ensure regulatory compliance, increase operational efficiency, and boost consumer engagement.

- In April 2024, DS Smith collaborated with BeFC to accelerate the development of smart, recyclable paper-based packaging solutions. The partnership focuses on integrating biofuel cell-powered smart tags into corrugated cardboard to enable real-time product tracking, freshness monitoring, and improved supply chain efficiency. The initiative aims to replace conventional batteries with fully recyclable paper-based energy sources, supporting waste reduction and circular economy goals.

Key Companies in Paper and Paperboard Packaging Market:

- Mondi

- International Paper

- Smurfit Westrock

- DS Smith

- Packaging Corporation of America

- Stora Enso

- Georgia-Pacific LLC

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Saica

- Mayr-Melnhof Karton AG

- Cascades Inc.

- Novolex

- Amcor plc

- YFY Inc.

Recent Developments

- In November 2025, Mondi expanded its corrugated and solid board food packaging portfolio in Europe, adding solid board solutions and advanced digital printing to support sustainability, EU regulatory compliance, shelf visibility, and regional supply reliability.

- In September 2025, Stora Enso introduced Ensovelvet, an uncoated SBS paperboard for luxury packaging, offering a smooth surface, high stiffness, and strong printability to meet growing demand for premium and circular packaging.

- In June 2025, DS Smith, in partnership with Matas Group, launched a paper-based Wavebag envelope for e-commerce, replacing plastic bubble wrap with a lightweight, fully recyclable alternative for fragile goods.

- In May 2025, International Paper commissioned a new corrugated box plant in Waterloo, Iowa, to strengthen its North American operations and supply sustainable packaging solutions, particularly for the protein segment.