Market Definition

The polymer foam market includes the global manufacturing and commercial exchange of cellular plastic materials used across diverse industrial sectors. It encompasses different chemical formulations such as polyurethane, polystyrene, phenolic, polyolefin, PVC, and melamine foams. The market serves essential industries, including the building and construction, automotive, packaging, and furniture sectors. It focuses on enhancing product performance, energy efficiency, and structural safety through the use of specialized foam solutions.

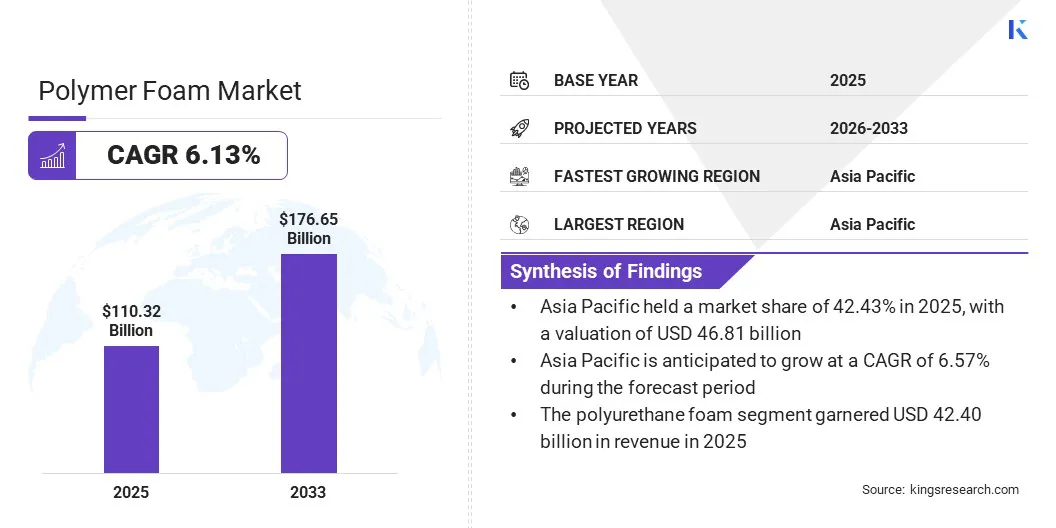

Polymer Foam Market Overview

The global polymer foam market size was valued at USD 110.32 billion in 2025 and is projected to grow from USD 116.44 billion in 2026 to USD 176.65 billion by 2033, exhibiting a CAGR of 6.13% during the forecast period. This growth is mainly driven by the increasing requirement for advanced fire-resistant casings for electric vehicle batteries across the automotive industry.

Additionally, biodegradable polymer materials are increasingly being adopted to replace conventional petroleum-based products, allowing for better waste management and alignment with circular economy goals.

Major companies operating in the global polymer foam industry are BASF, Rogers Corporation, Dow, Sealed Air Corporation, Saint-Gobain, JSP, Huntsman International LLC, SABIC, Recticel, Covestro AG, Carpenter Co., Wanhua, Armacell, Zotefoams plc, and SEKISUI CHEMICAL CO., LTD.

Polymer foam companies are working on spray polyurethane foam to mimic high-performance insulation seals in building envelopes. The material helps eliminate energy leakage before it occurs by forming a smooth thermal insulation and reducing air penetration. Spray foam applied on-site enhances the efficiency of buildings and makes it less challenging to integrate complex architectural designs.

It allows greater flexibility in filling irregular structural voids, meeting the requirements of different types of building projects, resulting in more accurate and faster construction of energy-efficient buildings.

- In December 2025, BASF declared the introduction of WALLTITE RSB, a new generation spray polyurethane foam aimed at promoting sustainability in the construction sector. The closed-cell insulation incorporates recycled and renewable raw materials, resulting in a lower carbon footprint compared to traditional formulations, with third-party validated benefits, including lower embodied carbon and higher building energy efficiency.

Key Market Highlights

- The global polymer foam market size was USD 110.32 billion in 2025.

- The market is projected to grow at a CAGR of 6.13% from 2026 to 2033.

- Asia Pacific held a share of 42.43% in 2025, valued at USD 46.81 billion.

- The polyurethane foam segment garnered USD 42.40 billion in revenue in 2025.

- The building and construction segment is expected to reach USD 63.21 billion by 2033.

- North America is anticipated to grow at a CAGR of 6.38% over the forecast period.

How is the growing demand for fire-resistant battery casings fueling market growth?

The polymer foam market is expanding due to the rising need for high-performance protective enclosures for electric vehicle batteries. The material can help manufacturers create lightweight battery housings to reduce the risk of thermal runaway by ensuring a stable flame barrier.

These dedicated foams also ensure thermal regulation and impact resistance, which serve to protect the vulnerable battery cells against external harm and temperature variations. They allow for more effective management of energy storage units and guarantee the viability of the vehicle power system.

Polymer foams can also reduce the total vehicle weight and increase the range of the vehicles, while also improving passenger safety in case of a fire. The material promotes the design of safer and more resilient battery designs that satisfy global safety standards. This practical advantage promotes mass-scale manufacturing of electric transportation, and specialized foams are significant contributors to modern car manufacturing.

- In July 2025, Covestro introduced the Baysafe BEF series, a high-performance flame-retardant encapsulation foam designed to enhance electric vehicle battery safety. This solution is a polyurethane-based solution that aims to curb thermal propagation between cells to ensure that fires do not occur in case of battery failure.

How does the volatility of raw material prices present a significant challenge to polymer foam market development?

Raw materials used in the production of polymer foams such as isocyanates and polyols are petrochemicals and are often prone to price fluctuations. Such erratic price fluctuations tend to slow down market growth because producers find it difficult to maintain stable profit margins and cope with complicated supply chain interruptions.

One of the ways to address this is by incorporating sustainable and bio-based solutions into the production process to eliminate dependence on traditional petroleum sources. This approach allows manufacturers to diversify their material sourcing and mitigate the effect of sudden spikes in the oil and gas industry. Another general practice is the investment by organizations in advanced recycling facilities in order to reclaim and reuse scrap material, which reduces waste generation and helps stabilize long-term operational costs.

How is the shift toward biodegradable materials positively influencing the polymer foam market?

There is a growing trend toward the adoption of biodegradable polymer materials that aid in mitigating the environmental effects of plastic waste while boosting sustainability. These green foams use vegetable polyols and renewable feedstock, which help manufacturers produce materials that break down naturally at the end of their lifecycle.

This capability enables companies to respond promptly to the increasing demand for green packaging and sustainable construction materials, while also improving brand image and environmental compliance.

The shift to biodegradable polymers indicates a move toward more responsible and sustainable manufacturing practices. These processes aim to reduce reliance on oil-based substances and improve waste management.

- In April, 2024, it was announced that Sony Corporation had selected Kaneka Corporation as its Green Planet foam molded product to cushion its large-screen BRAVIA televisions. This is a biopolymer fully derived from biomass, providing the necessary strength and resilience to protect large electronics during transportation. Moreover, it naturally decomposes in soil and seawater.

Polymer Foam Market Report Snapshot

|

Segmentation

|

Details

|

|

By Type

|

Polyurethane Foam, Polystyrene Foam, Polyolefin Foam, PVC Foam, Phenolic Foam, Melamine Foam, Others

|

|

By Application

|

Building and construction, Automotive, Packaging, Furniture, Appliances, Apparel, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Type (Polyurethane Foam, Polystyrene Foam, Polyolefin Foam, PVC Foam, Phenolic Foam, Melamine Foam, and Others): The polyurethane foam segment earned USD 42.40 billion in 2025, attributed to its versatile physical properties and extensive use in comfort and insulation applications. This dominance is supported by the growing demand for high-performance cushioning in the furniture and automotive sectors to enhance user experience and durability. Industries characterized by high-volume production are experiencing a rise in demand for custom polyurethane formulations to achieve specific thermal and acoustic requirements.

- By Application (Building and construction, Automotive, Packaging, Furniture, Appliances, Apparel, and Others): The building and construction segment held a share of 38.43% in 2025, driven by the increasing presence of stringent energy efficiency standards and sustainable building codes globally. Polymer foam insulation helps achieve lower energy consumption of energy by stabilizing indoor temperatures and minimizing thermal bridging. Lightweight and moisture-resistant materials are being increasingly preferred in modern construction projects, as they enhance the longevity of structures and minimize the cost of future maintenance.

What is the market scenario in Asia Pacific and North America?

Based on region, the polymer foam market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Asia Pacific accounted for a substantial share of 42.43% in 2025, valued at USD 46.81 billion. This dominance is reinforced by rapid industrialization and urbanization in countries such as China, India, and Japan. The region has a strong manufacturing ecosystem that enables large-scale production across automotive, electronics, and construction industries. In particular, the growth of the building industry in China generates a steady demand for high-performance insulation materials to comply with modern energy efficiency requirements.

The North America polymer foam market is expected to register the fastest CAGR of 6.38% over the forecast period. This rapid growth is facilitated by the presence of major industry players and their focus on introducing new products to meet the increasing demand for high-quality, durable materials. To ensure compliance with stringent environmental regulations, these organizations are prioritizing sustainability and low-emission solutions, including bio-based foams.

Significant investments in electric vehicle manufacturing are also promoting the use of specialized foams in battery thermal management and lightweight structural components.

- In September 2025, Rogers Corporation launched PORON 40 V0, a high-performance polyurethane foam used for filling and cushioning critical gaps. It has a UL 94 V-0 flame rating, and high compression set resistance, ensuring long-term reliability under harsh conditions.

Regulatory Frameworks

- In the U.S., the Environmental Protection Agency has provided the Significant New Alternatives Policy to assist in replacing ozone-depleting substances with less harmful blowing agents in the production of foams. The Occupational Safety and Health Administration also provides safety standards to make sure that the workers are not exposed to the diisocyanates, which are used in the production of polyurethane foams.

- In Europe, the registration and evaluation of chemicals used in polymer foam applications are regulated under the REACH regulation, which ensures a high level of protection for human health. The Waste Framework Directive and the EU Circular Economy Action Plan demonstrate high standards for recyclability and sustainability of foam-based packaging and construction materials.

- In Japan, the environmental impact of chemical additives is controlled by the Act on the Evaluation of Chemical Substances and Regulation of their Manufacture. The Ministry of Economy, Trade and Industry also provides guidelines on the management of industrial waste to encourage the effective recovery of plastic foam resources.

Competitive Landscape

Companies operating in the polymer foam market are developing specialized digital tools to speed up the process of creating sustainable material designs. These enterprises are developing cloud-based modeling systems that are integrated with molecular simulation software to enable virtual experimentation of bio-based polyols and recycled additives.

They are favoring solutions that forecast the environmental impact and structural behavior of new foam formulations prior to the start of physical production.

Firms are focusing on digital twin systems that can be integrated into chemical processing units and used to adjust manufacturing parameters based on real-time flow of materials. These companies are collaborating to enhance the capabilities of life cycle assessment tools. This innovation is a response to increasing need for transparent data on the carbon footprint of foam products.

- In January 2026, Covestro introduced the CQ-Configurator, a digital platform designed to streamline the development of sustainable polyurethane foam solutions. The tool is used to assess the environmental performance of rigid and flexible foam applications by manufacturers, offering real-time carbon emissions and insights into sustainable material content. It uses proven life cycle assessment data to support decision-makers in aligning with strict regulatory requirements and corporate sustainability goals without requiring highly technical skills.

Key Companies in The Polymer Foam Market

- BASF

- Rogers Corporation

- Dow

- Sealed Air Corporation

- Saint-Gobain

- JSP

- Huntsman International LLC

- SABIC

- Recticel

- Covestro AG

- Carpenter Co.

- Wanhua

- Armacell

- Zotefoams plc

- SEKISUI CHEMICAL CO., LTD.

Recent Developments (New Product Launch)

- In May 2025, Fraunhofer IAP proposed a shape-memory polyurethane film foam, FOIM, for use in industrial applications, making them safer and more efficient. It is stored as a compact film and thermally activated into a working foam, which requires no on-site handling of isocyanate, and offers bespoke properties tailored to specific sectors such as construction and automotive.

- In April 2024, Huntsman Corporation introduced its SHOKLESS polyurethane foam systems designed specifically to secure and shield the battery cells of electric vehicles. The portfolio also comprises low- to high-density foams, which offer the necessary thermal insulation and structural integrity when subjected to impact or thermal stress.