Market Definition

The cybersecurity for AI infrastructure market involves the use of artificial intelligence to strengthen an organization’s ability to detect, investigate, and mitigate security threats and to safeguard systems, data, and workflows that support the development, deployment, and operation of AI. The process involves providing cyber defense systems for critical data pipelines, model artifacts, and runtime environments. The rising demand for artificial intelligence across diverse end-use sectors is boosting market growth.

The market comprises integrated software, hardware, and services designed to protect AI infrastructure systems, data pipelines, models, APIs, and related infrastructure from evolving cyber threats. The security types include network security, endpoint security, cloud security, and application security, which leverage AI and machine learning, behavioral analytics, automated threat detection, and real-time response capabilities to defend critical AI infrastructure across end-use verticals, including banking, financial services, and insurance (BFSI), government & defense, healthcare, industrial, and IT & telecommunications.

Cybersecurity for AI Infrastructure Market Overview

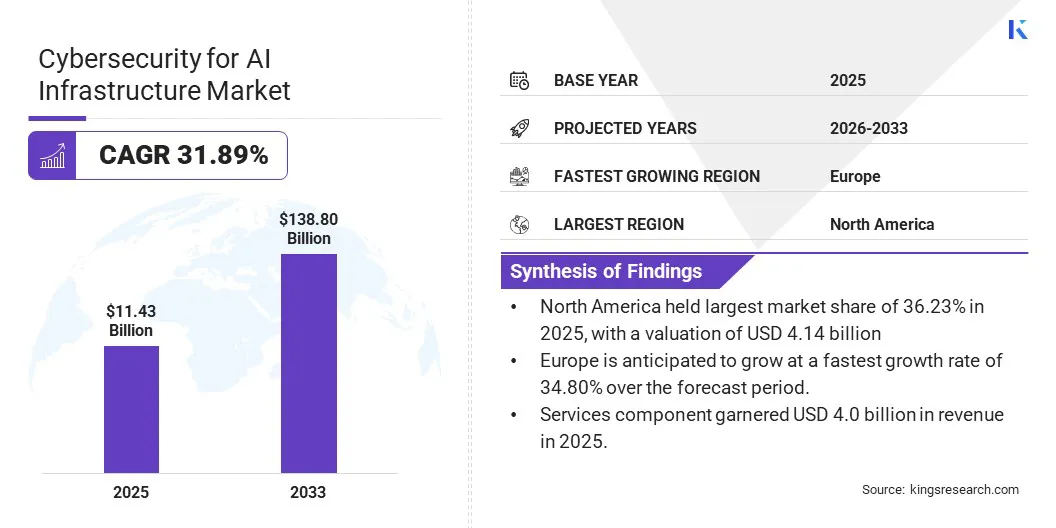

The global cybersecurity for AI infrastructure market size was valued at USD 11.43 billion in 2025 and is projected to grow from USD 15.16 billion in 2026 to USD 138.76 billion by 2033, exhibiting a CAGR of 37.21% during the forecast period (2026–2033). This expansion is largely attributed to the widespread adoption of AI systems across industrial and commercial establishments, which is increasing exposure to cyberattacks.

Additionally, stringent regulatory frameworks like GDPR, NIS2, and emerging AI‑specific standards are compelling market players to invest in specialized AI security solutions that ensure compliance and protect sensitive infrastructure data.

Major companies operating in the global cybersecurity for AI infrastructure industry are CrowdStrike, Inc., Palo Alto Networks Inc., Bitdefender, IBM Corporation, Cisco Systems, Inc., Fortinet, Inc., Check Point Software Technologies Ltd., SentinelOne, Darktrace Holding Limited, Wiz, Inc., Vectra AI, Inc., Cyera, Abnormal AI, Inc., and Proofpoint, Nozomi Networks Inc.

Market players are moving beyond traditional perimeter-based defenses, actively innovating AI-native, agentic security platforms that autonomously detect and investigate potential cyber threats. Leading vendors are converging observability and security into unified platforms, deploying tools such as AI Security Posture Management (AI-SPM) and Data Security Posture Management (DSPM) to address critical visibility gaps across cloud-native AI infrastructure.

- In August 2025, Google launched Big Sleep, which combines automation with human oversight to ensure ethical and transparent protection, thereby transforming cybersecurity from reactive defense to proactive, predictive protection. The system detects and neutralizes cyber threats such as the critical SQLite vulnerability CVE-2025-6965.

Key Market Highlights

- The global cybersecurity for AI infrastructure market size was USD 11.43 billion in 2025.

- The market is projected to grow at a CAGR of 37.21% from 2026 to 2033.

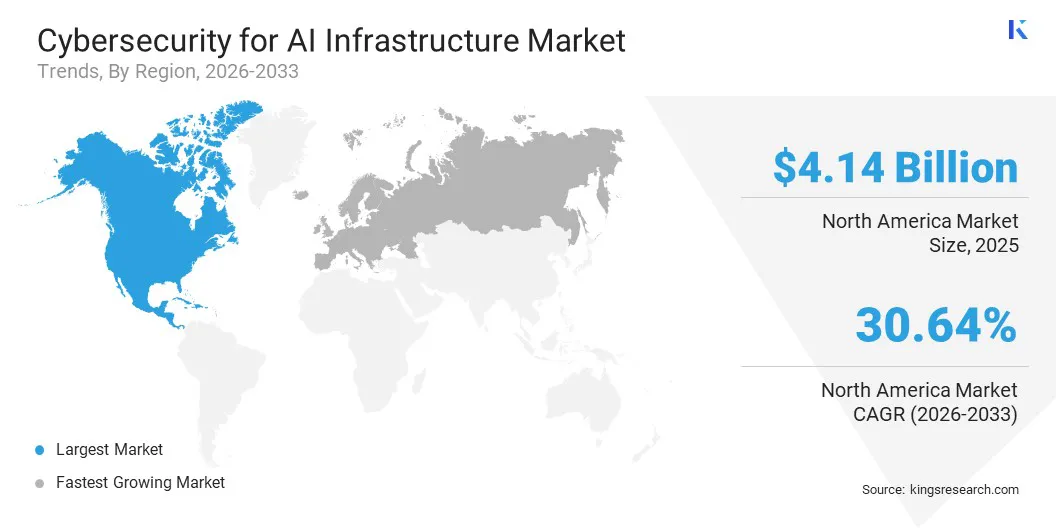

- North America held a share of 35.73% in 2025, valued at USD 4.14 billion.

- The hardware segment garnered USD 2.51 billion in revenue in 2025.

- The network security segment is estimated to register the fastest CAGR of 39.51% over the forecast period.

- The large enterprises segment is expected to reach USD 72.47 billion by 2033.

- The cloud-based segment is likely to generate a revenue of USD 6.54 billion by 2026.

- The banking, financial services, and insurance (BFSI) segment is anticipated to grow at a CAGR of 42.03% and is expected to reach USD 35.61 billion by 2033.

- Europe is anticipated to register a CAGR of 40.68% from 2026 to 2033.

How is the rising frequency of AI-targeted cyberattacks driving the demand for cybersecurity solutions across AI infrastructure?

The rise in cyberattacks specifically targeting AI infrastructure has emerged as a primary catalyst driving investments in AI-focused cybersecurity solutions. The widespread inclusion of artificial intelligence in critical operations across diverse end-use sectors makes them vulnerable to cyberattacks carried out on machine learning pipelines, agentic AI models, and autonomous execution environments.

Adversarial manipulation of AI agents, model poisoning, and data exfiltration targeting AI systems expose enterprises to unprecedented operational and reputational risks, compelling them to adopt purpose-built security frameworks that extend well beyond conventional IT defenses.

Companies are evolving defensive tools to handle cyber threats and safeguard critical infrastructure systems. The process involves the integration of operational technology and industrial control systems to enhance real-time threat detection and enable counter-responses. AI-driven, edge-based security solutions aid in maintaining operational performance and uptime while strengthening security across different end-use sectors.

- In February 2026, NVIDIA partnered with Siemens to develop AI-powered protection for operational technology (OT) and industrial control systems (ICS), which offer enhanced real-time threat detection and response across critical infrastructure. The BlueField DPUs solutions are designed to cater to energy, manufacturing, and transportation sectors while maintaining performance and uptime.

How do Large Language Models (LLMs) introduce cybersecurity challenges in AI infrastructure and affect data security and organizational risk?

Large Language Models (LLMs) deployed within organizations rely on vast amounts of training data, including sensitive enterprise information, which creates significant risks related to data privacy. The ability of LLMs to unintentionally reproduce parts of their training data can lead to the exposure of confidential data and make them vulnerable to threats such as data interception and poisoning attacks.

Such processes can result in the manipulation of model behavior and model exfiltration, where attackers steal model weights and replicate or exploit the system. The growth in the AI user base is further increasing the complexity of handling sensitive data, managing attacks, thereby making the security of AI infrastructure a complex challenge.

To address this challenge, market players are developing AI-native cybersecurity solutions, including LLM firewalls, real-time threat detection systems, and comprehensive AI security platforms. These approaches enable organizations to focus on securing models, data, and applications through continuous monitoring, vulnerability scanning, and protection against threats like prompt injection, data leakage, and model exfiltration.

- In July 2025, CyCraft launched XecGuard, a plug-and-play LLM firewall designed to secure AI models against threats like prompt injection, data extraction, and jailbreak attacks. The product enables real-time protection and seamless integration across cloud and on-premise environments, thus helping enterprises deploy AI securely.

- In April 2025, Palo Alto Networks introduced Prisma AIRS, a comprehensive AI security platform designed to protect the entire AI ecosystem, including applications, models, agents, and data. The model helps detect vulnerabilities, prevent threats such as prompt injection and data leaks, and ensure secure AI deployment.

How is the surging adoption of agentic AI positively influencing the cybersecurity for AI infrastructure market?

Innovations such as the adoption of agentic AI are revolutionizing cybersecurity by deploying autonomous, multi-agent systems that autonomously detect and mitigate threats within Security Operations Centers (SOCs). AI agents analyze vast threat intelligence datasets and reduce false positives via contextual insights from specialized models. The integration of agents in cybersecurity enables faster mitigation of emerging threats while adapting personalized protocols to specific vulnerabilities.

These innovations support proactive defenses such as dynamic access management aligned with zero-trust principles, continuous anomaly monitoring for insider threats, and automated vulnerability remediation throughout the software development lifecycle, thus fueling growth opportunities.

- In March 2026, CrowdStrike launched Charlotte AI AgentWorks Ecosystem, a no-code platform that enables organizations to build, deploy, and scale AI-powered security agents. The ecosystem integrates advanced AI models to enhance security operations and automate threat detection and response.

- In September 2024, ReliaQuest launched autonomous AI security agent GreyMatter, which processes security alerts 20 times faster and improves threat detection accuracy by 30%. The autonomous AI agent for security operations automates 98% of security alerts and reduces threat containment time to under 5 minutes.

Cybersecurity for AI Infrastructure Market Report Snapshot

|

Segmentation

|

Details

|

|

By Component

|

Hardware, Software, Services

|

|

By Security Type

|

Network Security, Endpoint Security, Cloud Security, Application Security, Others

|

|

By Organization Size

|

Large Enterprises, Small and Medium Enterprises (SMEs)

|

|

By Deployment Mode

|

Cloud-based, On-Premises

|

|

By End-User Industry

|

Banking, Financial Services, and Insurance (BFSI), Government & Defense, Healthcare, Industrial, IT & Telecommunications, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Component (Hardware, Software, and Services): The hardware segment captured the highest share in 2025 and is estimated to register a CAGR of 26.11% over the forecast period. This growth is mainly fueled by the high dependency of industrial automation on on-site processing devices such as industrial PCs, sensors, GPUs, and edge gateways to drive onboard artificial intelligence systems.

- By Security Type (Network Security, Endpoint Security, Cloud Security, Application Security, and Others): The network security segment is estimated to register the fastest CAGR of 39.51% over the forecast period. The rise of AI-driven systems, cloud adoption, and connected devices across organizations to safeguard sensitive communication data and maintain infrastructure integrity is leading to an expansion of network vulnerabilities, which requires advanced monitoring solutions.

- By Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)): The small and medium enterprises (SMEs) segment is projected to reach USD 18.82 billion by 2033. The high share is due to the rapid adoption of edge devices and scalable solutions in small and medium-scale industrial manufacturing sectors in order to automate production. The lower entry barriers for edge AI deployment enable SMEs to implement real-time automation without heavy cloud infrastructure investments.

- By Deployment Mode (Cloud-based and On-Premises): The cloud-based deployment held 52.07% market share in 2025. The deployment of cloud in edge AI for industrial automation is attributed to its applicability in streamlining supply chains, product lifecycles, and quality control, and its ability to enable real-time data access, cost savings, scalability, and smart Industry 4.0 manufacturing.

- By End-User Industry (Banking, Financial Services, and Insurance (BFSI), Government & Defense, Healthcare, Industrial, IT & Telecommunications, and Others): The banking, financial services, and insurance (BFSI) segment captured the largest share of approximately 42.03% in 2025. This growth is fueled by the high dependency on AI for fraud detection, risk assessment, and real-time transaction processing.

What is the market scenario in the North America and Europe regions?

Based on region, the cybersecurity for AI infrastructure market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America accounted for a substantial market share of 36.23% in 2025, valued at USD 4.14 billion. This high share is attributable to the U.S.’s position as a global leader in AI-driven cybersecurity, along with the high volume of financial transactions, which gives rise to a critical cyber threat environment. The interconnected economy in the region, which spans power grids, manufacturing end-use verticals, and supply chain operations, fuels the demand for cyber-resilient infrastructure.

Market players in the region are developing advanced solutions comprising AI-powered security platforms and cloud-native AI assistants to manage high volumes of attacks such as ransomware and web compromises. The U.S. accounts for the largest share in North America, propelled by its advanced technological capabilities, significant investments in cybersecurity infrastructure, and a high concentration of leading tech firms developing AI-driven security solutions.

- In April 2026, Linx Security raised USD 50 million in a Series B round to drive global expansion, scale go-to-market efforts, and accelerate its autonomous identity governance solutions. The company offers an AI-driven platform, Linx Autopilot, which manages and secures all types of organizational identities for large enterprises.

- In March 2026, Palo Alto Networks announced a security ecosystem for AI Factories, which is designed to protect both physical and digital infrastructure while enabling enterprises to scale AI safely. The move involves partnerships with Nokia, U Mobile, Aeris, and Celerway, targeted at extending AI-powered security across critical infrastructure.

The Europe market is anticipated to register the fastest growth, with a projected CAGR of 40.68% over the forecast period. This rapid growth is fueled by strategic investments under the European Defense Fund (EDF) 2025. This program funds cutting-edge research in AI-powered threat detection, autonomous cybersecurity solutions, and post-quantum cryptography.

The dual-use nature of these technologies strengthens cyber resilience across critical infrastructure, including energy grids, healthcare networks, banking systems, and transportation. Additionally, the rise in cyberattacks, sophisticated ransomware, and state-sponsored threats accelerates the demand for AI-driven security solutions, thereby positioning Europe as a cyber-secure ecosystem for AI infrastructure.

- In November 2025, SAP entered into a partnership with France’s AI ecosystem, including Bleu, Capgemini, and Mistral AI, to advance Europe’s digital sovereignty. The collaboration focuses on secure, scalable, AI-driven cloud solutions across AI infrastructure to protect data and intellectual property while supporting innovation.

Regulatory Frameworks

- In the U.S., the Cyber Incident Reporting for Critical Infrastructure Act (CIRCIA) creates a mandatory cybersecurity incident reporting system for critical infrastructure sectors. It requires organizations to report major cyber incidents within 72 hours and ransomware payments within 24 hours to improve national threat visibility.

- In Europe, the Cyber Resilience Act (CRA) mandates that manufacturers of digital products integrate cybersecurity features throughout the product lifecycle. It requires secure-by-design development, regular security updates, and clear vulnerability disclosure mechanisms to address risks proactively. The law further introduces compliance requirements and penalties, aiming to strengthen consumer protection and reduce systemic cyber risks across the EU market.

- In China, the Cyberspace Administration of China (CAC) regulates the provision of AI services in the country, thus promoting responsible AI development while also protecting national security, public interests, and user rights.

- In Japan, the framework built on the “Society 5.0” vision promotes a human-centered, data-driven society supported by AI and robotics. The 2025 AI Promotion Act focuses on supporting AI development, transparency, and risk mitigation rather than imposing heavy restrictions across diverse end-use sectors.

Competitive Landscape

Key players operating in the cybersecurity for AI infrastructure market are strengthening their capabilities through strategic mergers and acquisitions in order to capture a significant market share. Large technology firms and cybersecurity providers are acquiring niche AI security startups to enhance expertise in areas such as threat detection, data protection, and model security. This move further contributed to the rising complexity of AI ecosystems and the need for end-to-end security solutions.

- In September 2025, Check Point Software Technologies Ltd. acquired Lakera to strengthen its AI security capabilities. The acquisition aims to create a comprehensive, end-to-end AI security platform that protects the entire AI lifecycle, including models, data, and autonomous agents.

- In July 2025, Palo Alto Networks acquired Protect AI, which provides a unified platform to secure AI and machine learning (ML) systems, supporting MLSecOps practices. The acquisition is targeted at strengthening its position in AI security and enabling comprehensive protection across the entire AI lifecycle.

Key Companies in The Cybersecurity for AI Infrastructure Market

- CrowdStrike, Inc.

- Palo Alto Networks Inc.

- Bitdefender

- Cisco Systems, Inc.

- Fortinet, Inc.

- Check Point Software Technologies Ltd.

- SentinelOne

- Darktrace Holding Limited

- Wiz, Inc.

- Vectra AI, Inc.

- Cyera

- Abnormal AI, Inc.

- Proofpoint

- Nozomi Networks Inc.

- IBM Corporation

Recent Developments

- In March 2026, Google acquired Wiz and integrated it into Google Cloud. The move is aimed at strengthening Google Cloud security capabilities by combining Wiz’s cloud and AI security platform with Google’s infrastructure and AI expertise.

- In March 2026, SentinelOne launched AI security tools for securing AI agents, conducting AI red teaming, and automating investigations through its Purple AI platform. The tools enable faster threat detection, automated response and allow organizations to manage growing AI-related risks.

- In December 2025, BlackFog launched ADX Vision to address growing risks from shadow AI. The solution enhances its ADX platform by providing real-time visibility, detecting unauthorized AI activity, and preventing data exfiltration directly on endpoints.