DNA Sequencing Market Size

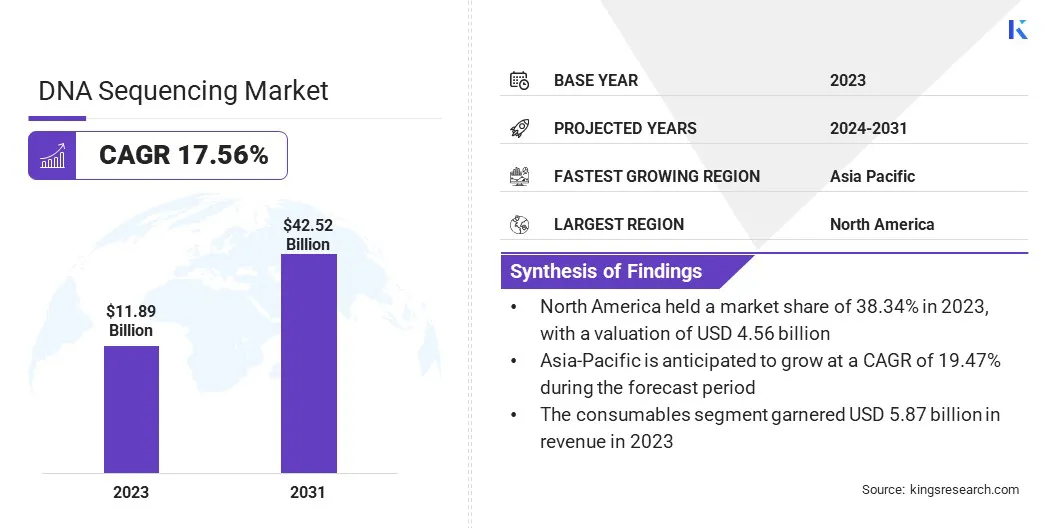

The global DNA Sequencing Market size was valued at USD 11.89 billion in 2023 and is projected to grow from USD 13.70 billion in 2024 to USD 42.52 billion by 2031, exhibiting a CAGR of 17.56% during the forecast period. The market is experiencing rapid expansion, mainly driven by advancements in technology and increasing applications in the healthcare sector.

Innovations in diagnostic panels and assays, aimed at detecting various genetic and infectious diseases, are fueling market growth. These developments cater to the rising demand for accurate and personalized healthcare solutions, thereby solidifying DNA sequencing's role in modern medical diagnostics and treatment strategies.

In the scope of work, the report includes solutions offered by companies such as Thermo Fisher, Scientific, Inc, Agilent Technology, Illumina, Inc., QIAGEN, F. Hoffmann-La Roche Ltd., Macrogen, Inc., PerkinElmer Genomics, PacBio, BGI, Bio-Rad Laboratories, Inc., and others.

The DNA sequencing market is experiencing robust growth, mainly due to increasing demand for precision medicine, ongoing advancements in technology, and the rising prevalence of genetic disorders and chronic diseases such as cancer. Innovations such as next-generation sequencing (NGS) and the launch of new diagnostic kits and assays are expanding the applications of DNA sequencing in oncology, genetic screening, and prenatal testing. Growing investments in research and development by both private and public sectors are further propelling market expansion.

- For instance, in July 2023, Integrated DNA Technologies, Inc. launched the xGen Respiratory Virus Amplicon Panel. This single panel is capable of detecting various viral respiratory variants, including SARS-CoV-2, Respiratory Syncytial Virus (RSV) A, RSV B, Influenza A H1N1, Influenza A H3N2, and Influenza B.

Such innovative product developments highlight the critical role that advancements in diagnostic panels play in propelling market growth by meeting the increasing demand for comprehensive and efficient testing solutions in infectious disease management.

DNA sequencing is the process of determining the precise order of nucleotides such as adenine, cytosine, guanine, and thymine, within a DNA molecule. It allows scientists to accurately read the genetic information encoded within an organism's DNA, providing valuable insights into genetic variations, mutations, and their potential implications for health, disease, and evolutionary relationships.

DNA sequencing is fundamental in numerous fields, including medical diagnostics, genetic research, evolutionary biology, and forensic science. It continues to advance rapidly, spurred by ongoing innovations in sequencing technologies that enhance accuracy, speed, and cost-effectiveness, thereby expanding its applications in understanding and manipulating genetic information.

Analyst’s Review

Strategic initiatives adopted by industry players for expanding the usage of DNA sequencing technologies in emerging markets are anticipated to propel market growth in the coming years.

- For instance, in January 2024, Orchid launched a commercially available whole genome sequencing service called preimplantation genetic testing (PGT) to understand the risk of genetic diseases in IVF embryos. Furthermore, in May 2023, Thermo Fisher Scientific Inc. and Pfizer Inc. collaborated to improve access to DNA testing for breast and lung cancer patients in more than 30 countries across Asia, Latin America, and the Middle East & Africa.

These efforts highlight the role of partnerships and the introduction of new service in boosting the global adoption and the expansion of the DNA sequencing market.

Key players in the DNA sequencing industry are aiming to take strategic initiatives such as expanding partnerships and collaborations. By forming alliances with healthcare providers, research institutions, and regulatory bodies, companies are improving accessibility to DNA testing services globally. Investing in research and development to innovate new sequencing technologies and diagnostic applications tailored to specific regional needs is facilitating the adoption of advanced technologies in the market.

DNA Sequencing Market Growth Factors

The increasing prevalence of chronic diseases and cancer globally is fueling the demand for DNA sequencing in diagnostics and treatment development. By decoding the genetic mechanisms of diseases, DNA sequencing allows for precise diagnoses and the creation of targeted therapies. Such personalized approaches enhance treatment effectiveness and patient outcomes, making it a crucial tool in modern medicine.

- The National Cancer Institute of the United States projects that 2,001,140 new cancer cases are anticipated to be diagnosed in the country by the end of 2024, with 611,720 individuals expected to succumb to the disease.

The growing reliance on DNA sequencing for understanding and combating these diseases is propelling market growth, as healthcare providers and researchers invest in advanced sequencing technologies to meet the rising demand for personalized healthcare solutions.

The DNA sequencing market faces significant challenges, primarily due to the high costs associated with advanced sequencing technologies and the complexities involved in interpreting large volumes of genomic data. These factors limit accessibility to sequencing services and hinder widespread adoption across healthcare systems and research institutions.

Despite these challenges, key players such as Illumina, Inc. and Thermo Fisher Scientific Inc. are contributing significantly to market growth through continuous innovation. These players are developing more efficient and cost-effective sequencing platforms, forging strategic partnerships to expand their market reach, and investing heavily in research and development.

Such efforts aid in enhancing sequencing accuracy, scalability, and affordability, thereby overcoming barriers and catalyzing the broader adoption of DNA sequencing in clinical diagnostics, personalized medicine, and scientific research globally.

DNA Sequencing Market Trends

The rising number of liquid biopsy tests for cancer detection, carrier screening to prevent genetic diseases, and non-invasive prenatal screening are fostering the growth of the DNA sequencing market. These advanced diagnostic techniques offer non-invasive, accurate, and early detection of various conditions, thereby enhancing patient care and outcomes.

Additionally, the continuous launch of new kits and assays for target and gene-specific sequencing has broadened the applications of next-generation sequencing (NGS). This expansion is resulting in increased demand and the widespread adoption of NGS technologies across different medical fields.

- For instance, in September 2023, Pillar Biosciences Inc. launched the oncoReveal Core LBx, a next-generation sequencing (NGS) kit designed for liquid biopsy-based tumor profiling.

Moreover, growing investment in research and development by both private companies and government agencies is fueling significant innovations in DNA sequencing technologies and expanding their applications. These investments are leading to the development of advanced, efficient, and cost-effective sequencing methods, thereby enhancing both the accuracy and speed of genetic analysis.

As new technologies emerge, they expand the range of applications in fields such as oncology, genetics, and prenatal screening. This creates a positive feedback loop, where advancements in DNA sequencing lead to increased adoption and demand, thereby fueling investment and innovation.

Segmentation Analysis

The global market is segmented based on type, application, sequencing type, end-user, and geography.

By Type

Based on type, the DNA sequencing market is categorized into consumables, instruments, and services. The consumables segment garnered the highest revenue of USD 5.87 billion in 2023. This growth is propelled by the increasing adoption of DNA sequencing technologies across various applications such as clinical diagnostics, research, and agriculture.

As the demand for personalized medicine and precision healthcare grows, there's an increasing need for consumables that facilitate these advanced sequencing techniques. Additionally, ongoing advancements in sequencing platforms and the introduction of high-throughput systems require a constant supply of consumables, thereby presenting expansion opportunities for manufacturer.

By Application

Based on application, the market is divided into drug discovery & development, diagnostics, personalized machine, and others. The drug discovery & development segment captured the largest DNA sequencing market share of 48.67% in 2023. The segmental growth is augmented by its crucial role in accelerating biomedical research and pharmaceutical innovation.

DNA sequencing technologies play a pivotal role in identifying potential drug targets, understanding disease mechanisms at a molecular level, and optimizing therapeutic efficacy through personalized medicine approaches. By enabling comprehensive genomic profiling and molecular characterization of diseases, these technologies facilitate the discovery of novel biomarkers and drug candidates.

Moreover, advancements such as next-generation sequencing (NGS) have revolutionized genomic data generation, analysis, and interpretation, thereby enhancing the efficiency and success rate of drug development pipelines. As pharmaceutical companies increasingly integrate genomics into their R&D strategies, the demand for DNA sequencing technologies in drug discovery is rising, thereby boosting the growth of the segment.

By End-User

Based on end-use, the market is categorized into biotechnology & pharmaceutical companies, contract research organizations (CROs), academic & research institutes, and others. The biotechnology & pharmaceutical companies segment is expected to garner the highest revenue of USD 16.18 billion by 2031.

These companies utilize DNA sequencing technologies extensively to enhance understanding of disease mechanisms, identify therapeutic targets, and develop precision medicines tailored to individual genetic profiles. The segment benefits from substantial investments in research and development aimed at leveraging genomic data for innovative therapies and diagnostics.

Additionally, collaborations between biotech firms, major pharmaceutical coroporations, and academic institutions expand the application of sequencing technologies across diverse therapeutic areas, including oncology, rare diseases, and infectious diseases. As genomic insights continue to reshape drug discovery and clinical practices, the biotechnology and pharmaceutical companies segment is witnessing substantial growth.

DNA Sequencing Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

North America DNA sequencing market share stood around 38.34% in 2023 in the global market, with a valuation of USD 4.56 billion. North America market exhibits robust growth due to continual technological advancements and significant investments in research and development. Major players such as Thermo Fisher Scientific Inc., Illumina, Inc., and Agilent Technologies, Inc., play a pivotal role in advancing innovation across various applications such as whole genome sequencing, transcriptomics, and oncology diagnostics in the region.

- For instance, in January 2024, Illumina, Inc. and Janssen Research & Development, LLC, collaborated on a novel molecular residual disease (MRD) assay. This assay utilizes whole-genome sequencing to detect circulating tumor DNA (ctDNA) for multi-cancer research.

This regional focus on innovation and collaboration underscores North America's standing as a leading market for DNA sequencing technologies, which fuels advancements in personalized medicine and clinical research. Moreover, collaborations between industry leaders and research institutions propel regional market expansion.

Asia-Pacific is anticipated to witness notable growth at a CAGR of 19.47% over the forecast period. This growth is largely attributed to growing healthcare investments, burgeoning biotechnology sectors, and increasing applications in personalized medicine. Countries such as China, Japan, and India are contributing significantly to this growth by investing heavily in genomic research and expanding healthcare infrastructure.

Local and international players are introducing advanced sequencing technologies tailored to regional needs. Government initiatives and collaborations between academic institutions and biotech firms are fostering innovation, particularly in areas such as agricultural genomics and infectious disease diagnostics. Rising awareness regarding genetic diseases and the integration of genomics into clinical practices further bolster domestic market growth.

Competitive Landscape

The global DNA sequencing market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Companies are implementing impactful strategic initiatives, such as expanding services, investing in research and development (R&D), establishing new service delivery centers, and optimizing their service delivery processes, which are likely to create new opportunities for market growth.

List of Key Companies in DNA Sequencing Market

Key Industry Development

- September 2023 (Product Launch): Integrated DNA Technologies, Inc. introduced xGen NGS products tailored for the Ultima Genomics UG 100 platform. This product line includes primers, adapters, and universal blockers, each designed to support diverse applications. These innovations are propelling market growth by enhancing sequencing efficiency and reducing associated costs.

The global DNA sequencing market is segmented as:

By Type

- Consumables

- Instruments

- Services

By Application

- Drug Discovery & Development

- Diagnostics

- Personalized Machine

- Others

By Sequencing Type

- Sanger Sequencing

- Next-generation Sequencing

- Other Sequencing Types

By End-User

- Biotechnology & Pharmaceutical Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- Others

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America