ADAS Vehicles Market Size

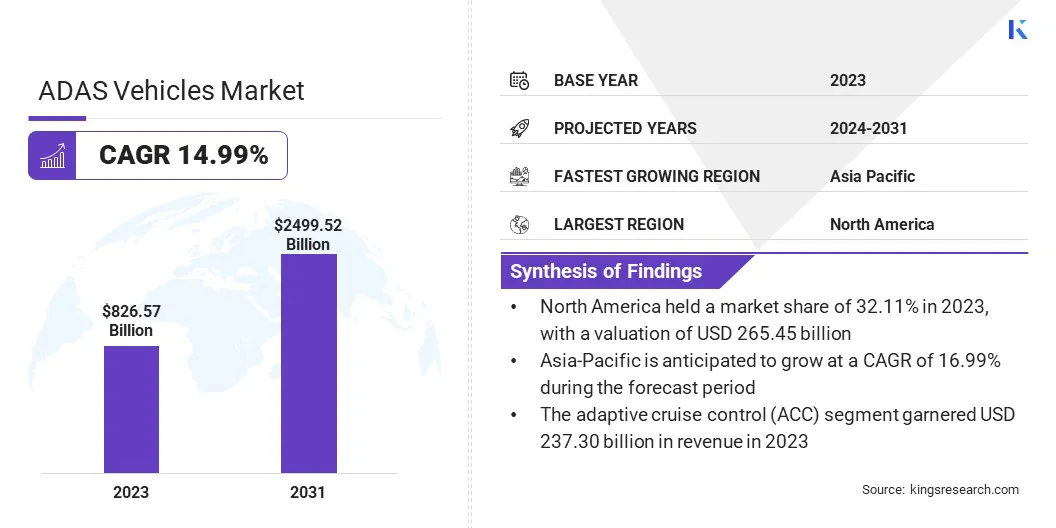

The global ADAS Vehicles Market size was valued at USD 826.57 billion in 2023 and is projected to reach USD 2,499.52 billion by 2031, growing at a CAGR of 14.99% from 2024 to 2031. In the scope of work, the report includes products offered by companies such as Continental AG, Robert Bosch GmbH, Aptiv PLC, Denso Corporation, Valeo SA, Magna International Inc., Mobileye N.V., NVIDIA Corporation, ZF Friedrichshafen AG, Hyundai Mobis Co., Ltd. and Others.

Consumer awareness of the benefits of advanced driver assistance systems (ADAS) in the automotive market has significantly increased in recent years. This is due to the growing emphasis on safety, with ADAS technologies being recognized as effective tools for enhancing road safety. Additionally, advancements in technology and the accessibility of information through various channels have contributed to raising consumer awareness of the capabilities and benefits of ADAS technologies.

Consumers are seeking to enhance their driving experiences, and ADAS technologies provide comfort and convenience features that reduce driver workload. Furthermore, the availability of ADAS features across different vehicle segments has made them more accessible to a wider range of consumers. These trends are expected to continue driving the demand for ADAS-equipped vehicles in the foreseeable future.

Analyst’s Review

In the upcoming years, futuristic trends in ADAS may revolutionize the automotive market. Integration of artificial intelligence (AI) may profoundly impact the driving experience. Advanced AI algorithms are able to analyze individual driving habits and preferences, providing tailored assistance that enhances safety and comfort.

Integrating ADAS systems with vehicle-to-everything (V2X) communication technologies may lead to improvements in road safety and efficiency. Real-time communication between vehicles and surrounding infrastructure may enable proactive responses to potential hazards, optimizing traffic flow and reducing accidents.

Ongoing research efforts are focused on achieving higher levels of autonomy. The development of Level 4 and Level 5 autonomy is foreseen to help build fully autonomous vehicles capable of operating without human intervention in specific conditions or environments, fundamentally transforming transportation and mobility. These emerging trends are anticipated to shape the advanced driver assistance systems (ADAS) market in the upcoming years, redefining the future of the automotive industry.

Market Definition

ADAS encompasses various technologies that enhance vehicle safety by assisting drivers and reducing the risk of accidents. These systems use sensors, cameras, and algorithms to monitor surroundings, detect hazards, and aid in driving. ADAS applications include adaptive cruise control, lane departure warning, automatic emergency braking, blind-spot detection, and parking assistance.

As ADAS technologies observe widespread adoption, governments worldwide have introduced regulations to ensure their safe implementation. Key regulations include UNECE Regulation No. 79 on steering equipment, the NHTSA FMVSS in the U.S., and the European Union's General Safety Regulation. Regulatory bodies like NHTSA, UNECE, and Japan's MLIT play vital roles in establishing and enforcing these regulations to promote vehicle safety and standardization.

ADAS Vehicles Market Dynamics

Continuous technological advancements, especially in sensor technologies, artificial intelligence (AI), and machine learning, have been pivotal in shaping the ADAS market. These innovations have greatly improved the capabilities of ADAS systems, making them more reliable, efficient, and sophisticated.

Advanced sensor technologies like radar and lidar enable better detection and interpretation of the vehicle's surroundings, enhancing the accuracy of ADAS functionalities. Additionally, AI and machine learning algorithms allow ADAS systems to learn and adapt to different driving scenarios, improving responsiveness and predictive capabilities.

As a result, consumers are increasingly opting for vehicles with advanced ADAS features, which is driving product demand. The rapid pace of technological innovation in this field promises even more developments, solidifying ADAS as a fundamental aspect of modern vehicle safety and automation.

Moreover, increasing safety regulations globally are pushing automobile manufacturers to integrate ADAS into vehicles. Governments worldwide are imposing strict safety standards to reduce road accidents and fatalities. Automakers are thus compelled to incorporate ADAS features like lane-keeping assistance, automatic emergency braking, and adaptive cruise control to meet regulatory requirements.

These technologies enhance vehicle safety while improving the overall driving experience. Compliance with safety regulations ensures that vehicles are equipped with advanced safety features, reducing the risk of accidents and injuries. Consequently, the ADAS Vehicles market is growing as manufacturers prioritize safety enhancements to meet evolving regulatory standards and consumer demand for safer vehicles.

However, the high cost of implementing ADAS presents a significant challenge to automakers and consumers. Integrating ADAS features into vehicles adds substantial expenses, potentially deterring price-sensitive consumers, especially in emerging economies. The cost implications arise from the sophisticated technology required for sensors, cameras, and computing systems, as well as the need for rigorous testing and validation processes. Automakers face the dilemma of balancing the demand for enhanced safety features with affordability.

Overcoming this challenge requires innovative approaches to cost reduction, such as economies of scale, advancements in manufacturing processes, and strategic partnerships to leverage shared resources and expertise. The surging focus of manufacturers on Making ADAS technology more accessible and affordable is fueling its widespread adoption and improving road safety globally.

Segmentation Analysis

The global market is segmented based on type, vehicle type, level of automation, sales channel, connectivity, and geography.

By Type

Based on type, the market is segmented into adaptive cruise control (ACC), lane departure warning (LDW) system, park assist, autonomous emergency braking (AEB), blind spot detection, and others. The adaptive cruise control (ACC) segment led ADAS vehicles market in 2023, reaching a valuation of USD 237.30 billion.

This dominance can be attributed to its widespread adoption across various vehicle segments, offering drivers enhanced convenience and safety by automatically adjusting vehicle speed to maintain a safe distance from preceding vehicles. ACC is utilized extensively to reduce driver fatigue and stress during long-distance travel, making it a sought-after feature in modern vehicles.

By Vehicle Type

Based on vehicle type, the market is classified into passenger vehicle and commercial vehicle. The passenger vehicle segment secured the largest ADAS Vehicles market share of 67.67% in 2023. This dominance is credited to the higher adoption rate of ADAS among passenger vehicle owners, driven by the increasing emphasis on safety, comfort, and convenience features.

Additionally, passenger vehicles, including sedans, SUVs, and hatchbacks, typically have a larger consumer base compared to commercial vehicles. The rising demand for ADAS-equipped passenger vehicles is further solidifying their leading position in the market.

By Level of Automation

Based on level of automation, the market is classified into level 1 (driver assistance), level 2 (partial automation), level 3 (conditional automation), level 4 (high automation), and level 5 (full automation). The level 4 (high automation) segment is anticipated to experience remarkable growth at a CAGR of 34.60% over the forecast period.

This progress is attributed to the increasing focus on developing fully autonomous vehicles capable of operating without human intervention in specific conditions or environments. Level 4 automation offers advanced features, allowing vehicles to handle most driving tasks autonomously, which appeals to consumers seeking enhanced safety, convenience, and efficiency. Moreover, ongoing technological advancements are foreseen to further fuel the expansion of the level 4 segment in the coming years.

ADAS Vehicles Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

The North America ADAS Vehicles Market share stood around 32.11% in 2023 in the global market, with a valuation of USD 265.45 billion. This dominance can be attributed to ADAS adoption rates, supportive regulatory frameworks, and increasing consumer awareness of vehicle safety technologies. With a robust automotive industry and growing demand for ADAS-equipped vehicles, the regional market is set to record high revenue growth.

Asia-Pacific is projected to observe rapid growth over the forecast period at a CAGR of 16.99%. This growth is driven by increasing urbanization, rising disposable incomes, and expanding automotive markets in countries like China, India, and Japan. Government initiatives promoting vehicle safety and advancements in technology adoption further contribute to the demand for ADAS in the region.

Competitive Landscape

The ADAS vehicles market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Manufacturers are adopting a range of strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, to strengthen their market standing.

List of Key Companies in ADAS Vehicles Market

Key Industry Developments

- January 2024 (Partnership): Foretellix and Nuro partnered to expedite the safe deployment of autonomous vehicles. The collaboration aimed to leverage Foretellix's verification and validation solutions with Nuro's autonomous technology expertise. By combining their resources, they sought to enhance the safety and efficiency of autonomous vehicle operations.

- September 2023 (Partnership): BMW collaborated with Amazon and Qualcomm to develop smart autonomous cars. This partnership aimed to integrate Amazon's Alexa voice assistant and Qualcomm's Snapdragon automotive cockpit platform into BMW vehicles. The initiative sought to enhance in-car connectivity, navigation, and entertainment experiences for users.

The global ADAS Vehicles Market is segmented as:

By Type

- Adaptive Cruise Control (ACC)

- Lane Departure Warning (LDW) System

- Park Assist

- Autonomous Emergency Braking (AEB)

- Blind Spot Detection

- Others

By Vehicle Type

- Passenger Vehicle

- Commercial Vehicle

By Level of Automation

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

By Sales Channel

By Connectivity

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America