Market Definition

The market covers the production, formulation, and distribution of raw vitamin compounds used in a wide range of end-use applications, including dietary supplements, food and beverages, pharmaceuticals, animal feed, and personal care products.

The ingredients in this market include both natural and synthetic forms of essential vitamins, such as vitamin A, B-complex, C, D, E, and K. These vitamins are critical for maintaining various aspects of health and wellness, including immune function, bone health, metabolism, and skin health.

The report examines critical driving factors, industry trends, regional developments, and regulatory frameworks impacting market growth through the projection period.

Vitamin Ingredients Market Overview

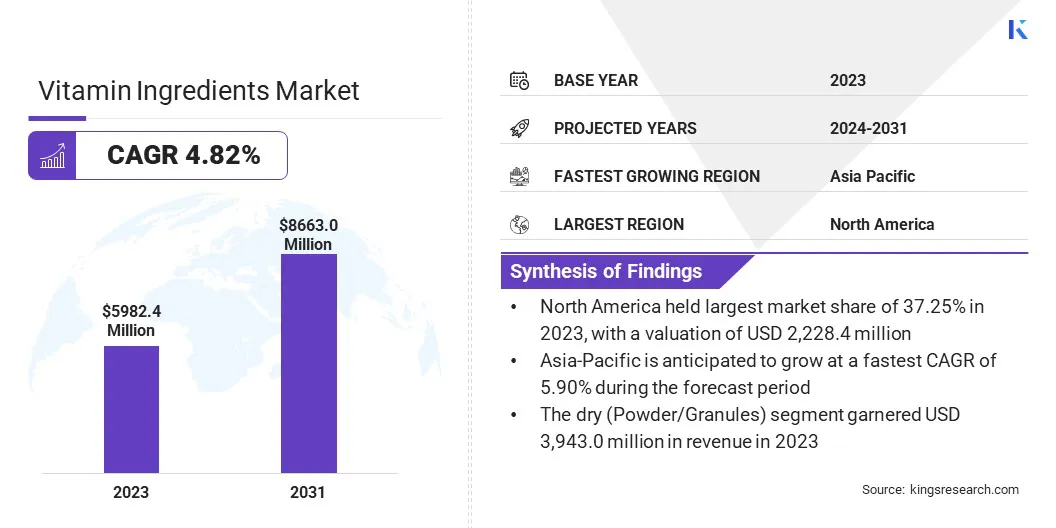

The global vitamin ingredients market size was valued at USD 5,982.4 million in 2023 and is projected to grow from USD 6,232.9 million in 2024 to USD 8,663.0 million by 2031, exhibiting a CAGR of 4.82% during the forecast period. The market is experiencing steady growth, driven by rising consumer focus on preventive healthcare and increasing demand for fortified foods and dietary supplements.

Growing awareness of the role of vitamins in maintaining overall health and addressing nutritional deficiencies is a key factor boosting market expansion. In addition, the pharmaceutical sector is witnessing heightened use of vitamin ingredients in therapeutic and preventive formulations, further driving growth.

Key Market Highlights

- The vitamin ingredients industry size was valued at USD 5,982.4 million in 2023.

- The market is projected to grow at a CAGR of 4.82% from 2024 to 2031.

- North America held a market share of 37.25% in 2023, with a valuation of USD 2,228.4 million.

- The vitamin D segment garnered USD 2,039.4 million in revenue in 2023.

- The chemical synthesis segment is expected to reach USD 4,774.5 million by 2031.

- The natural segment is anticipated to witness the fastest CAGR of 5.98% during the forecast period.

- The dry (powder/granules) segment garnered USD 3,943.0 million in revenue in 2023.

- The pharmaceuticals segment is anticipated to witness the fastest CAGR of 5.18% during the forecast period.

- The market in Asia Pacific is anticipated to witness the fastest CAGR of 5.90% during the forecast period.

Major companies operating in the vitamin ingredients market are Herbalife International Inc., Abbott, BASF, AMWAY, NOW Foods, Bayer AG, Pfizer Inc., GSK plc., dsm-firmenich, Lonza, RBK Nutraceuticals, ADM, Nutraceuticals Group Ltd, Glanbia plc, and Evonik Industries AG.

The market also benefits from technological advancements in vitamin synthesis and encapsulation, which enhance ingredient stability and bioavailability. Moreover, supportive government initiatives promoting health and nutrition, along with the expanding trend of personalized nutrition, are creating new opportunities for vitamin ingredient manufacturers.

- In October 2024, dsm-firmenich introduced Dry Vit A Palmitate for early life nutrition. This innovation enhances stability and bioavailability, ensuring better incorporation of essential vitamin A in infant formulas and meeting the growing demand for high-quality, sustainable ingredients.

Rising Health Awareness and Preventive Healthcare Trends

The vitamin ingredients market is experiencing steady growth, primarily driven by rising health awareness and the growing emphasis on preventive healthcare. As the global incidence of chronic diseases such as diabetes, cardiovascular disorders, and obesity continues to rise, consumers are increasingly shifting their focus toward maintaining health through balanced nutrition and supplementation.

In this context, vitamins are recognized as essential nutrients that support immune function, energy metabolism, and overall well-being, leading to higher demand for vitamin-enriched foods, beverages, and dietary supplements.

Public health initiatives, greater access to health information, and an expanding wellness culture are further accelerating the adoption of vitamin-based products across diverse population groups.

- In November 2023, Abbott launched a new version of PediaSure featuring the Nutri-Pull system, designed to support children's growth and development. This system combines essential ingredients such as vitamin K2, vitamin D, vitamin C, and casein phosphopeptides (CPPs) to enhance nutrient absorption and promote catch-up growth in children.

Stability and Short Shelf Life of Vitamin Ingredients

A significant challenge in the vitamin ingredients market is the instability and short shelf life of certain vitamins. Vitamins like Vitamin C, Vitamin A, and some B vitamins are highly sensitive to environmental factors such as heat, light, and oxygen.

This sensitivity leads to degradation, resulting in a loss of potency and effectiveness over time. Additionally, ensuring stable and effective formulations often increases production costs, as specialized techniques are needed to protect vitamins from deterioration.

To overcome this, manufacturers are using encapsulation technology to protect vitamins from environmental factors. Additionally, advanced production methods, like nano-encapsulation and biotechnology, are being developed to produce more stable vitamins. Temperature-controlled storage and transportation are used to further reduce degradation risks.

Plant-Based and Vegan Vitamin Ingredients

The demand for plant-based and vegan vitamin ingredients is growing rapidly, driven by consumer interest in sustainable, ethical, and health-focused alternatives. A key trend is the increasing availability of plant-derived vitamins, such as vitamin D2 and vegan B12, which cater to the rising number of people adopting plant-based and vegan lifestyles.

These innovations are expanding the range of vegan-friendly vitamin products, allowing manufacturers to offer cleaner, more sustainable alternatives to traditional, animal-derived options. Additionally, plant-based vitamins are gaining popularity due to their perceived health benefits, including higher antioxidant content and better bioavailability.

As sustainability becomes a greater priority for consumers and manufacturers, the shift towards plant-based and vegan vitamin ingredients is further fueling the development of eco-friendly and ethical supplement solutions.

- In April 2025, International Flavors & Fragrances Inc. (IFF) Pharma Solutions announced that it will showcase its plant-based dietary supplement ingredients and technical capabilities at Vitafoods Europe 2025. The company will highlight groundbreaking solutions, including vegan softgel technologies like SeaGel and VERDIGE SC, as well as plant-based gummy ingredients such as GRINDSTED Pectin Premium, addressing the growing demand for sustainable and vegetarian-friendly supplement options.

Vitamin Ingredients Market Report Snapshot

|

Segmentation

|

Details

|

|

By Vitamin Type

|

Vitamin D, Vitamin C, Vitamin B Complex, and Others

|

|

By Manufacturing Technology

|

Chemical Synthesis, Fermentation-based, Enzyme/Biotech-based

|

|

By Source

|

Synthetic, Natural

|

|

By Form

|

Dry (Powder/Granules), Liquid (Oil/Suspension)

|

|

By Application

|

Pharmaceuticals, Dietary Supplements, Food & Beverages, Cosmetics & Personal Care

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Vitamin Type (Vitamin D, Vitamin C, Vitamin B Complex, and Others): The vitamin D segment earned USD 2,039.4 million in 2023 due to its growing demand for immune support and its widespread use in dietary supplements and fortified foods.

- By Manufacturing Technology (Chemical Synthesis, Fermentation-based, Enzyme/Biotech-based): The chemical synthesis segment held 56.09% of the market in 2023, due to its cost-effectiveness, scalability, and ability to meet the high demand for synthetic vitamin ingredients.

- By Source (Synthetic, Natural): The synthetic segment is projected to reach USD 5,232.3 million by 2031, owing to its lower production costs, consistent quality, and the ability to meet large-scale demand for vitamin ingredients.

- By Form (Dry (Powder/Granules), Liquid (Oil/Suspension)): The liquid (Oil/Suspension) segment is anticipated to witness the fastest CAGR of 5.41% during the forecast period, driven by increasing demand for liquid formulations in dietary supplements, functional foods, and beverages for their ease of use and better bioavailability.

- By Application (Pharmaceuticals, Dietary Supplements, Food & Beverages, Cosmetics & Personal Care): The pharmaceuticals segment earned USD 2,278.7 million in 2023 due to the increasing use of vitamins in therapeutic treatments, preventive healthcare, and the growing demand for vitamin-based pharmaceutical formulations.

Vitamin Ingredients Market Regional Analysis

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

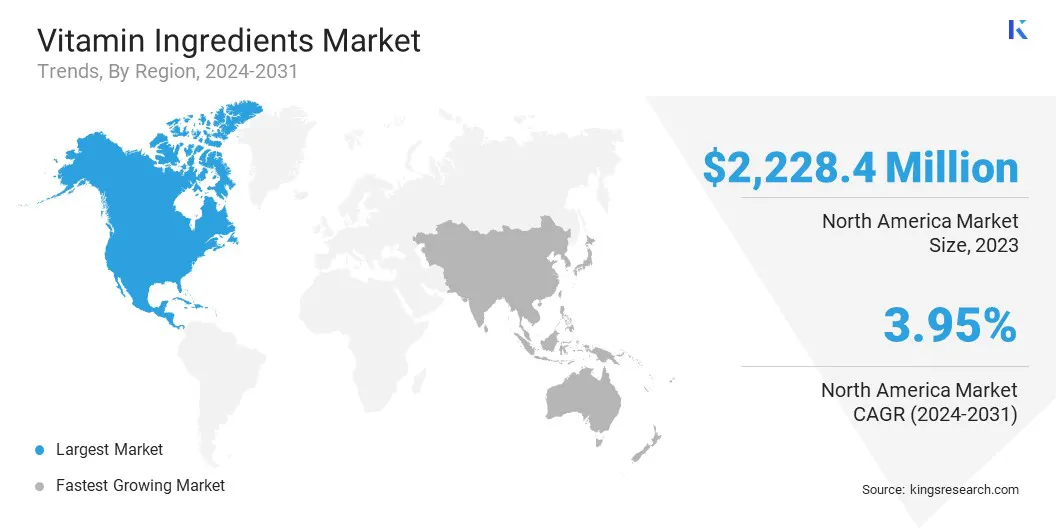

North America vitamin ingredients market share stood around 37.25% in 2023, with a valuation of USD 2,228.4 million. This dominant share is attributed to the region’s well-established healthcare sector, increasing consumer awareness regarding health and wellness, and high demand for dietary supplements and fortified foods.

North America vitamin ingredients market share stood around 37.25% in 2023, with a valuation of USD 2,228.4 million. This dominant share is attributed to the region’s well-established healthcare sector, increasing consumer awareness regarding health and wellness, and high demand for dietary supplements and fortified foods.

Additionally, the increasing prevalence of lifestyle-related diseases and the growing trend of preventive healthcare are driving the need for vitamin ingredients. North America is also home to numerous key players and significant investments in research and development, which further strengthens its position in the global market. The region's focus on innovation, along with a growing preference for clean-label and plant-based products, continues to fuel market expansion.

- In October 2024, Caldic North America unveiled a strategic partnership with Infusd Nutrition to launch the world’s first water-soluble vitamin D solution. This collaboration utilizes Infusd's innovative technology, enabling the integration of fat-soluble nutrients into beverages, aiming to combat widespread vitamin D deficiencies in North America.

The vitamin ingredients industry in Asia-Pacific is poised for significant growth at a robust CAGR of 5.90% over the forecast period. This growth is driven by the region's expanding population, and increasing health awareness, particularly in emerging economies like China and India.

The growing demand for dietary supplements, fortified foods, and functional beverages is contributing to this trend, as consumers increasingly focus on preventive healthcare and nutrition.

Additionally, the growing prevalence of chronic diseases and aging populations in several countries is further boosting the need for vitamins. The region's strong manufacturing capabilities and rising investments in the healthcare sector are also key factors supporting the market's expansion.

- In March 2025, Louis Dreyfus Company (LDC) launched its new plant-based Vitamin E product line at the Food Ingredients China exhibition in Shanghai. The products include various forms such as mixed tocopherols, acetate, and succinate, designed for use in food, pharmaceuticals, and cosmetics.

Regulatory Frameworks

- In the United States, the Food and Drug Administration (FDA) regulates dietary supplements under the Dietary Supplement Health and Education Act (DSHEA). This regulation governs the safety, labeling, and marketing of dietary supplements.

- In India, the Food Safety and Standards (Health Supplements, Nutraceuticals, Food for Special Dietary Use, Food for Special Medical Purpose, Functional Food, and Novel Food) Regulations, 2016 regulate the production, labeling, and marketing of health supplements and nutraceuticals.

- Globally, the Codex Alimentarius Guidelines for Vitamin and Mineral Food Supplements (CXG 55-2005) regulate the composition, labeling, and safety of vitamin and mineral supplements. These guidelines aim to ensure the safety, quality, and efficacy of supplements intended to supplement the normal diet by providing concentrated sources of essential vitamins and minerals.

Competitive Landscape

The vitamin ingredients industry is characterized by intense competition, with participation from both well-established multinational corporations and emerging regional players. Market dynamics are influenced by continuous product innovation, evolving consumer preferences, and a growing emphasis on sustainability and clean-label formulations.

Key players are focused on expanding their product portfolios through the development of bioavailable and stable formulations, particularly those derived from plant-based sources. Investment in research and development (R&D) remains a core strategy to enhance product efficacy, shelf life, and compliance with regulatory standards.

- In March 2025, The Vitamin Shoppe launched a unique supplement line designed specifically for individuals using GLP-1 medications such as Ozempic and Mounjaro. This new product range focuses on supporting weight loss, muscle maintenance, and overall health, complementing the benefits of these medications.

Key Companies in Vitamin Ingredients Market:

- Herbalife International Inc.

- Abbott

- BASF

- AMWAY

- NOW Foods

- Bayer AG

- Pfizer Inc.

- GSK plc.

- dsm-firmenich

- Lonza

- RBK Nutraceuticals

- ADM

- Nutraceuticals Group Ltd

- Glanbia plc

- Evonik Industries AG

Recent Developments (Partnerships/New Product Launch)

- In November 2024, DSM-Firmenich, in partnership with Rohto Pharmaceutical, introduced Vision R in Japan, a multivitamin solution featuring the patented Sprinkle It Technology (SIT). This innovative product is designed to address nutritional gaps and support healthy aging by seamlessly integrating essential micronutrients into the food of elderly individuals.