Market Definition

The market encompasses the full ecosystem of technologies, therapies, and systems designed to transport pharmaceutical agents directly to specific tissues, cells, or disease sites. This market includes solutions tailored to treat a wide range of diseases such as cardiovascular, pulmonary, infectious, endocrine, and oncological conditions.

It covers applications across first, second, and third order targeting approaches. The report outlines the primary drivers of the market, along with an in-depth analysis of emerging trends and evolving regulatory frameworks shaping the market trajectory.

Targeted Drug Delivery Market Overview

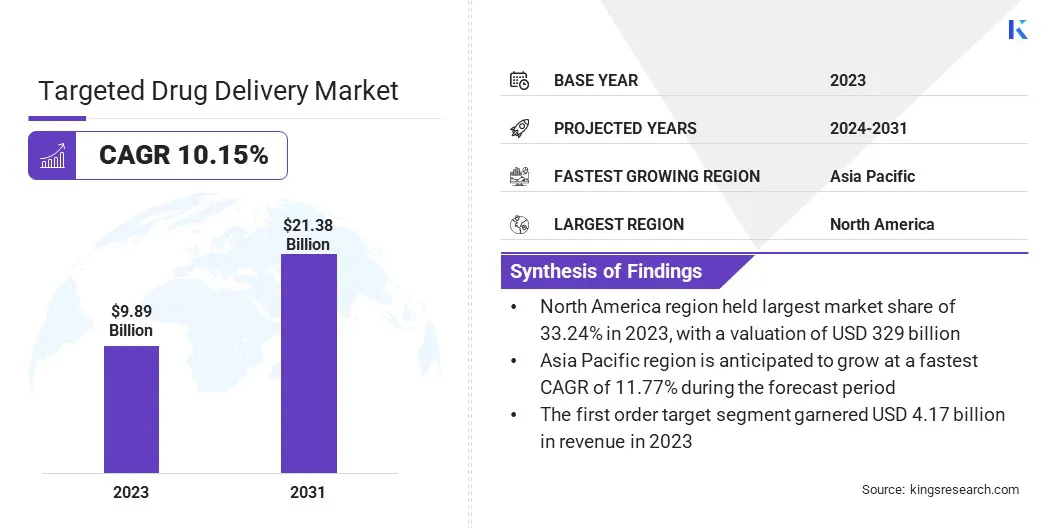

The global targeted drug delivery market size was valued at USD 9.89 billion in 2023 and is projected to grow from USD 10.87 billion in 2024 to USD 21.38 billion by 2031, exhibiting a CAGR of 10.15% during the forecast period.

The growth is attributed to the advancements in nanotechnology, which have enabled the development of more precise and efficient drug delivery systems. The increasing prevalence of chronic diseases, cancer, and autoimmune disorders has amplified the demand for specialized therapies that target specific areas of the body, enhancing treatment efficacy and reducing side effects.

Major companies operating in the targeted drug delivery industry are EVONIK, DelSiTech Ltd., RenovoRx, Arrowhead Pharmaceuticals, Inc., Eligo Bioscience, Resyca BV, AbbVie, F. Hoffmann-La Roche Ltd, Boston Scientific Corporation, Re-Vana Therapeutics, Oakwood Labs, Sanofi, Adaptimmune, EyePoint Pharmaceuticals, Phosphorex.

Moreover, a significant trend in the market is the growing adoption of advanced drug delivery technologies, such as nanoparticles, liposomes, and microspheres. These innovations are allowing for more precise and efficient drug delivery, improving patient outcomes.

The increased focus on biologics, biosimilars, and minimally invasive procedures is further accelerating the development and adoption of targeted drug delivery systems.

- In April 2025, Redwire Corporation launched the Golden Balls experiment, which seeks to produce gold nanospheres in space for potential use in early cancer detection, targeted drug delivery, and enhanced therapy.

Key Highlights:

- The targeted drug delivery market size was valued at USD 9.89 billion in 2023.

- The market is projected to grow at a CAGR of 10.15% from 2024 to 2031.

- North America held a market share of 33.24% in 2023, with a valuation of USD 3.29 billion.

- The cardiovascular segment garnered USD 2.70 billion in revenue in 2023.

- The first order targeting segment is expected to reach USD 8.92 billion by 2031.

- The hospitals segment is expected to reach USD 8.23 billion by 2031.

- The market in Asia Pacific is anticipated to grow at a CAGR of 11.17% during the forecast period.

Market Driver

Rising Prevalence of Chronic Diseases

The market is registering strong growth driven by the rising prevalence of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions. These conditions demand long-term treatments that are effective and safe.

Targeted delivery systems meet this need by focusing the drug directly on the affected area, reducing exposure to healthy tissues. This improves treatment precision and lowers the risk of side effects.

The growing global burden of chronic illnesses is prompting healthcare systems and pharmaceutical companies to prioritize treatment approaches that improve outcomes and reduce long-term costs. This is leading to increased investment in targeted delivery platforms, including nanoparticles, antibody-drug conjugates, and lipid-based carriers.

- In October 2024, according to the Centers for Disease Control and Prevention (CDC), heart disease remained the leading cause of death in the U.S. for men, women, and people across most racial and ethnic groups. One person dies every 33 seconds from cardiovascular disease, highlighting the critical need for more effective and targeted treatment solutions.

Market Challenge

Biological Barriers Hindering the Precise Delivery

A key challenge in the targeted drug delivery market is overcoming the body's biological barriers, such as the blood-brain barrier, which can hinder the precise delivery of drugs to the targeted site. This leads to inconsistent therapeutic outcomes, as drugs may not reach the target or may be eliminated too quickly.

A potential solution lies in nanotechnology, where nanoparticles can be designed to cross these barriers more effectively. Additionally, smart delivery systems that respond to specific biological signals could improve the accuracy and reliability of drug delivery, addressing this challenge.

Market Trend

Adoption of Non-invasive Delivery Platforms

The market is registering the growing trend of adopting non-invasive delivery platforms, driven by the demand for patient-friendly treatment options. These platforms such as intranasal sprays, transdermal patches, and inhalable systems enable the delivery of drugs without the need for injections or surgical procedures.

This shift is particularly important in chronic disease management, where long-term treatment adherence is critical. Non-invasive methods improve patient compliance by reducing discomfort and minimizing the risk of complications associated with invasive procedures.

They allow for more consistent drug absorption and are being increasingly explored for complex applications, including nose-to-brain therapies and systemic delivery through mucosal membranes.

- In October 2024, Aero Pump and Resyca collaborated to launch the Ultra Soft Nasal Pump Spray. The device leverages Medspray’s spray nozzle chip technology to deliver a uniform soft mist, enabling enhanced nasal cavity coverage for precise nasal drug delivery. Designed for nose-to-brain therapies and nasal vaccination, the system offers improved drug absorption, reduced irritation, and better patient comfort. The device supports aseptic filling and is suitable for multidose applications.

Targeted Drug Delivery Market Report Snapshot

|

Segmentation

|

Details

|

|

By Disease

|

Cardiovascular, Pulmonary, Infectious, Endocrine, Oncological

|

|

By Application

|

First Order Targeting, Second Order Targeting, Third Order Targeting

|

|

By End User

|

Hospitals, Clinics, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E. , Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation:

- By Disease (Cardiovascular, Pulmonary, Infectious, Endocrine, and Oncological): The cardiovascular segment earned USD 2.70 billion in 2023, due to the rising incidence of heart diseases and growing demand for site-specific drug delivery.

- By Application (First Order Targeting, Second Order Targeting, Third Order Targeting): The first order targeting segment held 42.17% share of the market in 2023, due to its effectiveness in delivering drugs to specific organs with minimal systemic exposure.

- By End User (Hospitals, Clinics, Others): The hospitals segment is projected to reach USD 8.23 billion by 2031, owing to high patient volume, advanced infrastructure, and increasing adoption of targeted therapies in clinical settings.

Targeted Drug Delivery Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America accounted for 33.24% share of the targeted drug delivery market in 2023, with a valuation of USD 3.29 billion. The dominance is attributed to the well-established healthcare systems, widespread access to advanced treatment options, and a high concentration of key market players.

The region benefits from strong government support for precision medicine and a high rate of adoption of next-generation drug delivery technologies. Ongoing clinical research, strategic partnerships between biotech firms and research institutions, and high healthcare spending are accelerating the development and commercialization of targeted therapies.

The targeted drug delivery industry in Asia Pacific is poised to grow at a significant growth at a CAGR of 11.17% over the forecast period. The growth is attributed to the rapid improvements in healthcare infrastructure, expanding patient populations, and increasing demand for personalized medicine.

Government-led health reforms, rising healthcare investments, and growing insurance coverage are improving access to advanced treatments. Countries such as China, India, South Korea, and Japan are emerging as key hubs for pharmaceutical manufacturing and clinical trials.

Additionally, a surge in academic and industry-led research initiatives, supported by public and private funding, is driving innovation in drug delivery systems tailored to regional healthcare needs.

- In January 2025, researchers from IIT Guwahati partnered with Bose Institute Kolkata to develop an innovative injectable hydrogel for targeted breast cancer therapy. The hydrogel, composed of ultra-short peptides, serves as a localized drug reservoir that releases anti-cancer drugs in response to high glutathione levels in tumor cells. This controlled delivery system reduces systemic side effects and improves drug uptake.

Regulatory Frameworks

- In the U.S., targeted drug delivery systems are regulated by the Food and Drug Administration (FDA) under the Center for Drug Evaluation and Research (CDER) and the Center for Biologics Evaluation and Research (CBER), depending on the product type. These systems must comply with the FDA’s Investigational New Drug (IND) application and New Drug Application (NDA) processes, which assess safety, efficacy, and manufacturing quality.

- In Europe, targeted drug delivery products are regulated by the European Medicines Agency (EMA). These systems must adhere to the centralized marketing authorization procedure for high-technology or innovative therapies. The EMA evaluates quality, safety, and therapeutic efficacy under frameworks such as the Advanced Therapy Medicinal Products (ATMP) regulation when applicable, particularly for gene or cell-based delivery approaches.

Competitive Landscape

Key market players are focusing on expanding their drug delivery portfolios through product development and technological advancements. A strong emphasis is placed on integrating nanotechnology, lipid-based carriers, and polymeric systems to improve targeting accuracy and therapeutic outcomes.

Strategic collaborations with academic institutions and biotech firms are used to accelerate pipeline development and enhance R&D capabilities. Many companies are entering into licensing agreements and joint ventures to co-develop novel delivery platforms and speed up regulatory approvals.

Clinical trial expansion and data-driven research are being leveraged to demonstrate the effectiveness of targeted therapies, which supports differentiation in a competitive landscape. Customization of delivery solutions based on therapeutic area, disease stage, and patient profile is becoming a key strategy to enhance market share and sustain long-term growth.

- In September 2024, Evonik expanded its EUDRACAP platform by launching EUDRACAP colon, the ready-to-fill only functional capsule designed for targeted drug delivery to the ileo-colonic region. Developed to address the need for delivering sensitive actives like live biotherapeutic products and oral biologics, the capsule is available in technical grade, with a GMP-grade version in development.

List of Key Companies in Targeted Drug Delivery Market:

- EVONIK

- DelSiTech Ltd.

- RenovoRx

- Arrowhead Pharmaceuticals, Inc.

- Eligo Bioscience

- Resyca BV

- AbbVie

- F. Hoffmann-La Roche Ltd

- Boston Scientific Corporation

- Re-Vana Therapeutics

- Oakwood Labs

- Sanofi

- Adaptimmune

- EyePoint Pharmaceuticals

- Phosphorex

Recent Developments

- In February 2025, RenovoRx presented pre-clinical data at the Society of Interventional Oncology Annual Conference, showcasing the potential of its Trans-Arterial Micro-Perfusion (TAMP) therapy platform. The study demonstrated that intra-arterial administration of a drug using the RenovoCath delivery system could improve localized drug delivery in difficult-to-treat cancers, particularly those with limited blood supply, such as pancreatic adenocarcinoma.