Sciatica Treatment Market Size

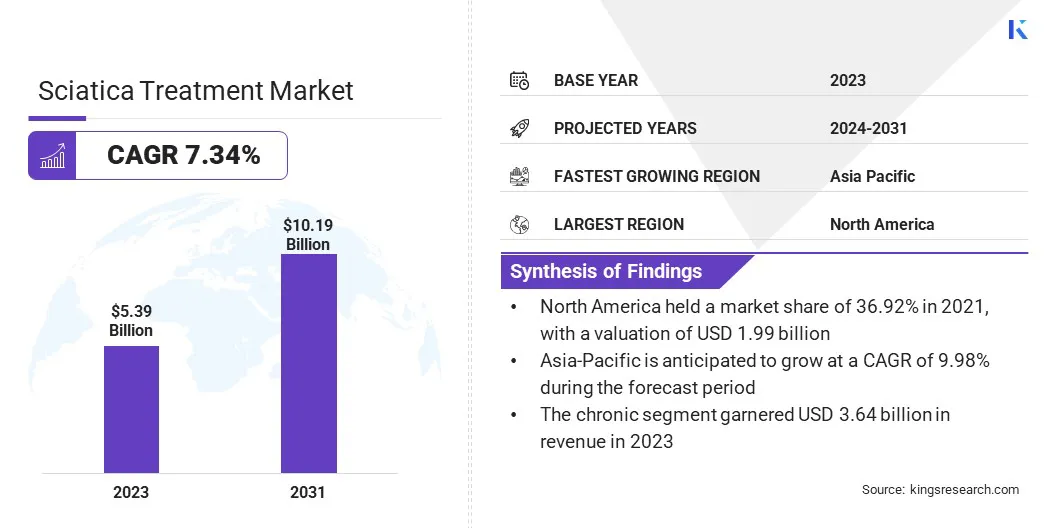

The global Sciatica Treatment Market size was valued at USD 5.39 billion in 2023 and is projected to grow from USD 5.78 billion in 2024 to USD 10.19 billion by 2031, exhibiting a CAGR of 7.34% during the forecast period. The market is evolving due to increasing awareness of treatment options and advancements in medical technology.

Growing emphasis on personalized medicine and holistic approaches is leading to a rise in non-invasive therapies. Additionally, the expansion of healthcare infrastructure and increasing access to specialized care are driving market growth. As patient preferences shift toward effective and safer treatment modalities, the market is poised to witness sustained expansion in the coming years.

In the scope of work, the report includes solutions offered by companies such as Teva Pharmaceutical Industries Limited, Abbott, Sun Pharmaceutical Industries Ltd., Aurobindo Pharma, Zydus Lifesciences Limited, Sorrento Therapeutics Inc., Amneal Pharmaceuticals LLC, Sinfonia Biotherapeutics, Johnson and Johnson, Alkem Laboratories Ltd, and others.

The sciatica treatment market is experiencing significant growth due to the rising incidence of of the condition, supported by several factors such as aging populations, sedentary lifestyles, and increasing obesity rates.

- A study published in the National Library of Medicine in August 2022 indicates that patients with chronic pain have poorer surgical outcomes compared to those with acute pain. While some studies report cure rates exceeding 75%, others show rates below 50%. However, recent orthopedic procedures for managing sciatica boast success rates of 70% and higher in the short term.

With these advances in treatment options, the demand for effective sciatica management is expected to continue to grow, thereby reshaping the landscape of the market. The integration of digital health solutions is enhancing patient engagement and adherence to treatment plans, thus propelling market expansion.

Sciatica treatment encompasses various medical interventions designed to relieve pain and discomfort caused by irritation or compression of the sciatic nerve. This condition is often charaterized by pain radiating from the lower back through the hips and down one leg.

Treatment options include non-surgical approaches such as physical therapy, chiropractic care, pain management techniques, and medications aimed at reducing inflammation and pain. In more severe cases, surgical interventions may be necessary. The primary goals of sciatica treatment are to alleviate symptoms, improve mobility, and enhance the patient's overall quality of life, by ensuring effective management of the condition.

Analyst’s Review

The growing shift toward improved research and collaboration is leading to notable market expansion. The establishment of the NIH Back Pain Consortium (BACPAC) Research Program highlights a concerted effort to enhance research and collaboration in the diagnosis and treatment of chronic lower back pain, including sciatica, thereby fostering advancements in the sciatica treatment market.

- In August 2023, the NIH Back Pain Consortium (BACPAC) Research Program was established as part of the HEAL initiative. This initiative encompasses a network of 14 funded entities dedicated to overcoming the challenges associated with the diagnosis and management of chronic lower back pain in the United States. By tackling these issues, BACPAC aims to enhance research collaboration and drive advancements in treatment approaches for conditions such as sciatica.

To propel market growth, key players should consider investing in innovative research and development, enhancing collaboration with healthcare providers, and focusing on integrating advanced technologies. By emphasizing patient-centered approaches and effective treatment strategies, these companies are strengthening their position in the sciatica treatment market.

Sciatica Treatment Market Growth Factors

The rising incidence of sciatica is significantly boosting the demand for effective treatment options, which is propelling market growth. This increase is further fueled by several factors such as aging populations, sedentary lifestyles, and rising obesity rates. As people age, the likelihood of developing conditions that contribute to sciatica, such as herniated discs and spinal stenosis, is increasing.

- According to the WHO, by 2030, 1 in 6 people worldwide are likely to be aged 60 years or older, with the population in this age group increasing from 1 billion in 2020 to 1.4 billion. By 2050, the number of individuals aged 60 and above is expected to double, reaching 2.1 billion. Additionally, the number of people aged 80 years or older is projected to triple between 2020 and 2050, reaching 426 million.

Additionally, modern sedentary lifestyles and prolonged periods of sitting are increasing pressure on the sciatic nerve, while obesity is further fueling this issue by placing additional strain on the spine. Moreover, there is a growing need for medical interventions, including medications, physical therapy, and surgical procedures, to manage and alleviate sciatica symptoms effectively. This heightened demand for diverse treatment options is continuously expanding the market.

A significant challenge impeding the development of the sciatica treatment market is the variability in treatment outcomes, leading to patient dissatisfaction and reduced trust in available therapies. Inconsistent success rates among different treatment modalities are creating uncertainty, making patients hesitant to pursue certain options.

Key players are mitigating this challenge by investing heavily in research to establish standardized treatment protocols and improve outcome predictability. They are further focusing on education initiatives for healthcare providers and patients while collaborating with research institutions to foster innovation and enhance the efficacy of treatments in the market.

Sciatica Treatment Market Trends

The growing trend toward non-surgical treatment options for sciatica, including physical therapy, chiropractic care, acupuncture, and various pain management techniques, is propelling market growth. Patients and healthcare providers are increasingly opting for these less invasive approaches, supported by the preference to avoid surgical risks and reduce recovery times.

This preference is leading to increased demand for non-surgical sciatica treatments, as more individuals are seeking safer and more convenient alternatives for managing their symptoms. The rising demand for non-surgical interventions is boosting the growth of the sciatica treatment market.

The integration of digital health technologies, such as telemedicine, mobile health applications, and wearable devices, is transforming the market landscape. These technologies enable remote monitoring and personalized treatment plans, which improve patient engagement and adherence to prescribed therapies.

By facilitating easier management of sciatica symptoms, these solutions are enhancing treatment outcomes and overall patient satisfaction. As more healthcare providers and patients adopt digital health solutions, the demand for innovative sciatica treatments is increasing, contributing to the expansion of the market.

Segmentation Analysis

The global market is segmented based on condition, treatment type, distribution channel, and geography.

By Condition

Based on condition, the sciatica treatment market is categorized into chronic and acute. The chronic segment garnered the highest revenue of USD 3.64 billion in 2023. The increasing prevalence of long-term pain conditions among the aging population and those with sedentary lifestyles are propelling segmental growth.

Patients with chronic sciatica often require ongoing treatment, leading to a consistent demand for effective therapies, including medications, physical therapy, and advanced surgical options. Ongoing innovations in treatment protocols, coupled with a proactive approach of healthcare providers to develop comprehensive care strategies, are further aiding the expansion of the segment.

Additionally, the growing focus on managing chronic pain is fostering collaboration among both researchers and clinicians, thus enhancing treatment outcomes and contributing to segmental expansion.

By Treatment Type

Based on treatment type, the market is categorized into prescription drugs, physical therapy, spinal injections, surgery, and alternative therapies. The prescription drugs segment was valued at USD 1.44 billion in 2023. This considerable growth is fostered by the rising demand for effective pain management solutions.

As awareness of available pharmacological options grows, healthcare providers are prescribing a range of medications, including NSAIDs, muscle relaxants, and corticosteroids, to alleviate symptoms and improve patient outcomes. The segment is further divided into steroids, NSAIDS, antidepressants, and others. The NSAIDs segment captured the largest sciatica treatment market share of 44.43% in 2023.

As these medications are widely prescribed due to their anti-inflammatory properties, their consistent demand is boosting sales and expanding market reach. Additionally, the growing awareness among healthcare providers and patients regarding the benefits of NSAIDs is leading to increased utilization, thereby reinforcing their pivotal role in the overall treatment strategy for sciatica.

By Distribution Channel

Based on distribution channel, the market is divided into hospitals & associated pharmacies, retail pharmacies, and online pharmacies. The hospitals & associated pharmacies segment is expected to garner the highest revenue of USD 4.31 billion by 2031.

Hospitals provide comprehensive care, including diagnosis and treatment, while pharmacies ensure the availability of essential medications such as NSAIDs and muscle relaxants. This collaboration enhances patient access to treatments and promotes adherence to prescribed therapies.

Additionally, as healthcare facilities increasingly adopt advanced technologies and integrated care models, they are fostering innovation in treatment approaches. This synergy between hospitals and pharmacies improves patient outcomes propels market growth by fostering a reliable infrastructure for sciatica management.

Sciatica Treatment Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

North America sciatica treatment market share stood around 36.92% in 2023 in the global market, with a valuation of USD 1.99 billion. The increasing aging population, combined with sedentary lifestyles, is contributing to a rising incidence of sciatica cases. Additionally, the region's strong focus on research and development, along with the availability of innovative treatment options, is enhancing patient access to effective therapies.

Furthermore, the collaboration between hospitals, pharmacies, and healthcare providers is facilitating comprehensive care, thus propelling regional market growth by ensuring that patients receive timely and effective sciatica management solutions.

Asia-Pacific is anticipated to witness robust growth at a CAGR of 9.98% over the forecast period. This growth is mainly propelled by the rising incidence of lower back pain among the population and increasing government initiatives aimed at early clinical management of acute episodes.

- Notably, in May 2022, Bayer AG announced the expansion of its over-the-counter product line to better meet the needs of Indian consumers. This expansion included the introduction of new line extensions for its pain management brands such as Saridon and Supradyn.

Such initiatives highlight the commitment to addressing the growing demand for effective pain relief solutions, thereby augmenting domestic market progress.

Competitive Landscape

The global sciatica treatment market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Companies are implementing impactful strategic initiatives, such as expanding services, investing in research and development (R&D), establishing new service delivery centers, and optimizing their service delivery processes, which are likely to create new opportunities for market growth.

List of Key Companies in Sciatica Treatment Market

- Teva Pharmaceutical Industries Limited

- Abbott

- Sun Pharmaceutical Industries Ltd.

- Aurobindo Pharma

- Zydus Lifesciences Limited

- Sorrento Therapeutics Inc.

- Amneal Pharmaceuticals LLC

- Sinfonia Biotherapeutics

- Johnson and Johnson

- Alkem Laboratories Ltd

The global sciatica treatment market is segmented as:

By Condition

By Treatment Type

- Prescription Drugs

- Steroids

- NSAIDs

- Antidepressants

- Others

- Physical Therapy

- Spinal Injections

- Surgery

- Alternative Therapies

By Distribution channel

- Hospitals & Associated Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America