Market Definition

The underwater robotics market refers to the industry encompassing the design, development, manufacturing, and deployment of robotic systems engineered to operate in underwater or subsea environments. These systems include Remotely Operated Vehicles (ROVs) and Autonomous Underwater Vehicles (AUVs). The market encompasses hardware, software, and associated services and is pertinent to Inspection, Repair & Maintenance (IRM), Surveying & Mapping, Exploration & Resource Assessment, Surveillance & Security, and Search & Recovery Operations. End users include oil and gas companies, defense organizations, research institutions, and maritime authorities.

U.S. Underwater Robotics Market Overview

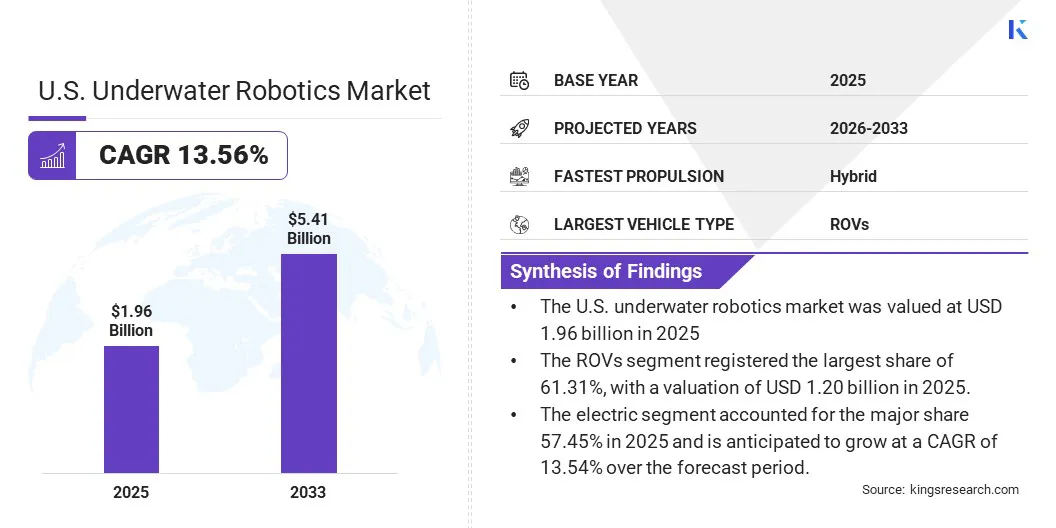

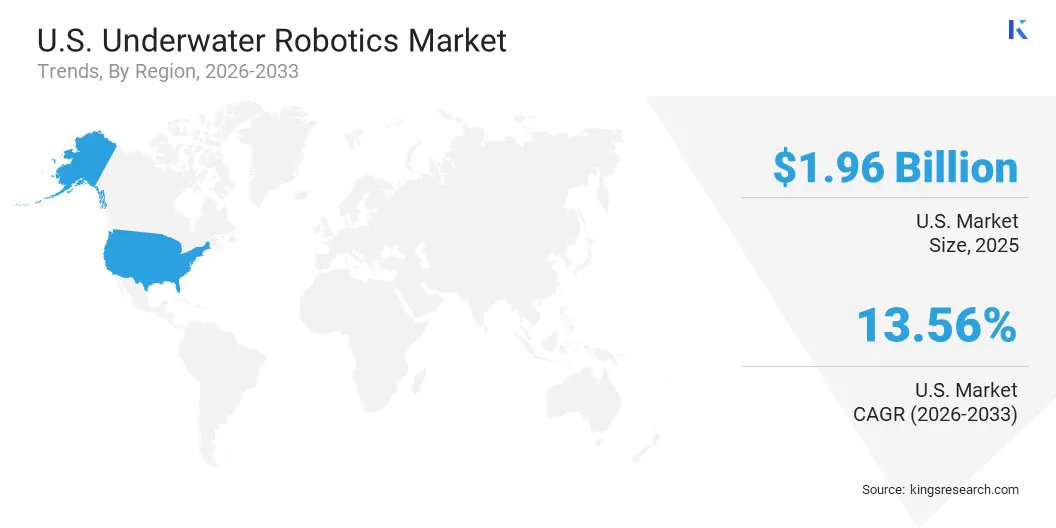

The U.S. underwater robotics industry size was valued at USD 1.96 billion in 2025 and is projected to reach USD 5.41 billion by 2033, exhibiting a CAGR of 13.56% during the forecast period. This growth is fueled by the increasing demand for subsea inspection, maintenance, and exploration in the offshore energy, defense, and scientific research sectors. Advancements in autonomous technologies and cost-efficient robotic platforms further support the growth.

Major companies operating in the U.S. underwater robotics market are General Dynamics Mission Systems, Inc, Boeing, HII (Huntington Ingalls Industries), Lockheed Martin Corporation, L3Harris Technologies, Inc., Oceaneering International, Inc., Teledyne, Anduril Industries, NAUTICUS ROBOTICS, Ocean Aero, Vatn Systems, VideoRay LLC, Blue Robotics Inc, Deep Ocean Engineering, Inc., and Terradepth.

Federal investments in maritime security, alongside rising initiatives in ocean exploration and environmental monitoring, are further accelerating market expansion. The introduction of next-generation remotely operated and autonomous vehicles is expected to transform operations in deepwater and harsh environments.

- In September 2023, Saab signed a licensing agreement with MBARI to manufacture and market the long-range autonomous underwater vehicle Tethys in the US. Tethys can travel more than a thousand kilometers for weeks, supports a variety of scientific and military missions, and allows remote shore-based operations without a support ship.

Key Market Highlights

- The U.S. underwater robotics market size was valued at USD 1.96 billion in 2025.

- The market is projected to grow at a CAGR of 13.56% from 2026 to 2033.

- The ROVs segment garnered USD 1.20 billion in revenue in 2025.

- The electric segment is expected to reach USD 3.11 billion by 2033.

- The surveillance & security segment is anticipated to witness the fastest CAGR of 15.03% during the forecast period.

- The offshore energy segment held a market share of 31.21% in 2025.

How is the expansion of offshore oil and gas operations driving consistent demand for underwater robotic systems in the U.S. market?

The offshore oil and gas industry is the primary driver of demand in the U.S. underwater robotics industry. Exploration in deeper and more remote subsea environments makes diving impractical and unsafe. ROVs and AUVs enable operators to conduct detailed inspections, maintenance, and repairs at depths and locations inaccessible or hazardous for humans, improving operational efficiency and safety.

This demand is reinforced by the extensive network of offshore platforms, with 3,728 active worldwide in 2025, including 1,641 in the Gulf of Mexico, according to the Cornell University database. All of these platforms require regular monitoring and maintenance. The ongoing pace of U.S. offshore drilling, combined with aging subsea infrastructure, ensures sustained and long-term demand for underwater robotics across major domestic oil and gas regions.

How are high initial investment and operational costs limiting the broader adoption of underwater robotic systems in the U.S. market?

Purchasing advanced ROVs and AUVs requires significant investment in specialized support vessels, subsea docking infrastructure, skilled operators, and ongoing maintenance. Such substantial financial commitments are typically feasible only for major oil and gas companies, large defense contractors, and government-funded research institutions.

This effectively excludes mid-sized operators and nascent application segments such as aquaculture and environmental monitoring. Consequently, leading U.S. manufacturers are turning to modular and scalable system architectures, while rental and leasing models are gaining popularity as affordable alternatives to outright ownership. This, in turn, lowers the financial barrier to entry for new market entrants.

How are advancements in artificial intelligence and autonomous navigation redefining operational capabilities in the U.S. underwater robotics market?

AI and autonomous advancements enable robots to control self-directed systems. These advancements are empowering the new generation of underwater robots that can adapt to unpredictable environments and execute complex tasks with minimal human intervention. As such, they can plan missions, take real-time decisions, avoid obstacles, and analyze data on their own. The technology is helping to reduce dependence on skilled operators and bandwidth-limited acoustic communication.

- In June 2024, researchers funded by the U.S. National Science Foundation (NSF) introduced autonomous underwater vehicles (AUVs) powered by artificial intelligence to enhance marine conservation. The open-source MeCO platform collects detailed ecosystem data, identifies invasive species, and creates habitat maps. This technology aims to transform environmental monitoring and support global efforts in preserving underwater ecosystems.

U.S. Underwater Robotics Market Report Snapshot

|

Segmentation

|

Details

|

|

By Vehicle Type

|

ROVs and AUVs

|

|

By Propulsion

|

Electric, Hydraulic, and Hybrid

|

|

By Application

|

Inspection, Repair & Maintenance (IRM), Surveying & Mapping, Exploration & Resource Assessment, Surveillance & Security, Search & Recovery Operations, and Others

|

|

By End User

|

Offshore Energy, Defense & Security, Research & Academia, Aquaculture & Fisheries, Commercial Service Providers, Mining, and Others

|

|

By Region

|

U.S.

|

Market Segmentation

- By Vehicle Type (ROVs and AUVs): The ROVs segment earned USD 1.20 billion in 2025, due to their widespread use in offshore oil and gas operations, subsea inspections, and maintenance tasks. Their reliability, operational depth, and advanced capabilities make ROVs essential for complex underwater missions.

- By Propulsion (Electric, Hydraulic, and Hybrid): The electric segment held a share of 57.45% of the market in 2025, due to its advantages in energy efficiency, lower maintenance requirements, and environmental friendliness. Electric propulsion enables quieter operation, extended mission duration, and is favored for both commercial and scientific underwater robotics applications.

- By Application (Inspection, Repair & Maintenance (IRM), Surveying & Mapping, Exploration & Resource Assessment, Surveillance & Security, Search & Recovery Operations, and Others): The inspection, repair & maintenance (IRM) segment is projected to reach USD 1.63 billion by 2033, owing to the aging offshore infrastructure and the growing need for regular monitoring and upkeep.

- By End User (Offshore Energy, Defense & Security, Research & Academia, Aquaculture & Fisheries, Commercial Service Providers, Mining, and Others): The defense & security segment is anticipated to grow at a CAGR of 14.56% through the projection period, driven by increased investments in maritime surveillance, underwater threat detection, and naval modernization.

What are the key use cases of underwater robotics in the U.S.?

The U.S. underwater robotics market includes a broad and growing range of application segments, reflecting the wide utility of ROVs, AUVs, and hybrid underwater systems across many industries. For example, the offshore oil and gas industry relies heavily on underwater robots to perform tasks such as pipeline inspection, wellhead monitoring, and subsea infrastructure maintenance at Gulf of Mexico facilities. At the same time, federal agencies such as NOAA and leading oceanographic research institutions deploy AUVs to map the deep sea, study biodiversity, and conduct climate research in U.S. waters.

The expansion of offshore wind energy along the U.S. East Coast is further broadening demand, with the U.S. Department of Energy reporting that the U.S. offshore wind project development and operational pipeline reached a potential generating capacity of 80,523 MW as of May 2024, a 53% increase from the previous year. This signifies the need for underwater robotic systems supporting cable inspection, foundation monitoring, and environmental assessment.

Regulatory Frameworks

- The U.S. Coast Guard regulates the operation and navigation of unmanned underwater vehicles to ensure maritime safety within U.S. waters. Its guidelines cover operational standards, collision avoidance, and compliance with maritime laws for both commercial and research missions.

- The National Oceanic and Atmospheric Administration (NOAA) oversees the collection of oceanographic data and environmental protection related to underwater robotics. NOAA’s regulations ensure that research and exploration activities are conducted responsibly and do not harm marine ecosystems.

Competitive Landscape

The U.S. underwater robotics market is characterized by a competitive landscape across ROV, AUV, and hybrid vehicle segments. It comprises established technology conglomerates, specialized subsea engineering firms, defense contractors, and emerging technology developers. Domestic players maintain a strong competitive edge, driven by robust defense procurement by the U.S. Navy and the Department of Defense, which continues to fund the development and deployment of advanced unmanned underwater systems for surveillance, mine countermeasures, and intelligence operations.

Strategic alliances with federal agencies, long-term service contracts with offshore energy operators, and joint development programs with leading oceanographic research institutions are driving competitive positioning in the U.S. underwater robotics market. At the same time, new entrants focused on miniaturized and affordable AUV platforms are gradually eroding the market dominance of incumbent leaders in commercial, defense, and scientific application segments.

- In April 2026, Booz Allen Ventures invested in Ulysses, a San Francisco-based robotics firm, to strengthen Booz Allen’s autonomous undersea capabilities. Ulysses develops cost-effective, high-volume autonomous surface and underwater vehicles, supporting advanced, scalable solutions for missions such as mine countermeasures, infrastructure inspection, and environmental monitoring.

Key Companies In The U.S. Underwater Robotics Market:

- General Dynamics Mission Systems, Inc.

- Boeing

- HII (Huntington Ingalls Industries)

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Oceaneering International, Inc.

- Teledyne

- Anduril Industries

- NAUTICUS ROBOTICS

- Ocean Aero

- Vatn Systems

- VideoRay LLC

- Blue Robotics Inc

- Deep Ocean Engineering, Inc.

- Terradepth

Recent Developments

- In March 2026, Cellula Robotics USA Inc., delivered a long-endurance, fuel cell-powered Guardian AUV prototype for the CAMP Defense Innovation Unit project. Collaborating with Metron Inc. and partners, this effort expands Cellula’s U.S. presence and advances scalable, autonomous maritime defense capabilities.

- In March 2026, Kraken Robotics announced a USD 615 million deal to acquire Covelya Group and its subsidiaries. The acquisition will enhance Kraken’s global subsea technology capabilities and its standing in defense and commercial markets, while broadening its product portfolio, technical expertise, and geographical presence in the maritime sector.

- In March 2026, Oceaneering International launched the Momentum Electric Work Class ROV at the Subsea Tieback Forum. The ROV features electric propulsion for greater efficiency and is designed for 30-day continuous operation. Advanced sensors and high payload capacity support extended offshore work. The system is compatible with Millennium Plus ROV infrastructure.

- In February 2025, Mahindra Group and Anduril Industries announced a partnership to co-develop autonomous maritime systems, advanced AI-enabled counter-drone technologies, and command and control software. The collaboration targets modular AUVs for security missions and aims to integrate multiple sensor technologies to enhance regional security and maritime operations.

- In January 2026, Vatn Systems acquired Crewless Marine to enhance its autonomous underwater vehicle acoustic sensing and signal processing capabilities. The acquisition strengthens Vatn’s position in naval and environmental applications, brings key experts to the team, and supports vertical integration for faster development and reduced supply chain dependencies.