Market Definition

The next generation sequencing (NGS) market refers to the industry that deals in the high-throughput sequencing of DNA and RNA, including instruments, consumables, and services. NGS allows rapid sequencing of DNA or RNA with reduced costs compared to traditional sequencing techniques. The market comprises applications such as oncology, rare genetic disorders, reproductive health, infectious disease testing, drug discovery, etc., with clinical laboratories & hospitals, biotechnology companies, academic institutions, and pharmaceutical companies operating nationwide.

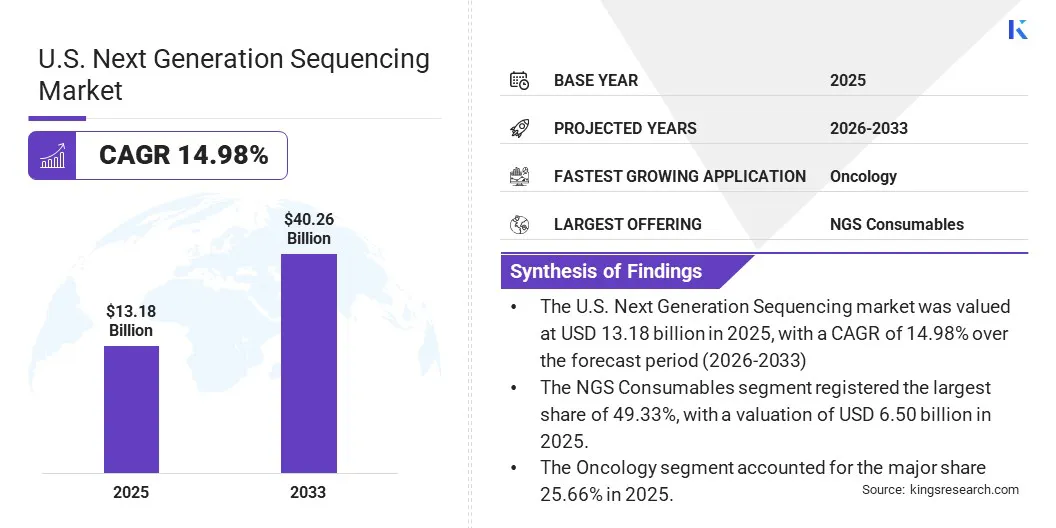

U.S. Next Generation Sequencing Market Overview

The U.S. next generation sequencing market size was valued at USD 13.18 billion in 2025 and is projected to reach USD 40.26 billion by 2033, exhibiting a CAGR of 14.98% during the forecast period. This significant growth is fueled by rapid advancements in sequencing technologies, increasing integration of NGS in clinical diagnostics, and rising demand for personalized medicine. The growth is also attributed to the expanding applications across oncology, rare disease detection, and reproductive health.

Major companies operating in the U.S. next generation sequencing market are Illumina, Inc., Agilent Technologies, Inc, DH Life Sciences, LLC., Bio-Rad Laboratories, Inc., BD (Becton, Dickinson and Company), Clear Labs, Inc., Ultima Genomics, Inc., Element Biosciences, Twist Bioscience, Oxford Nanopore Technologies plc., GENEWIZ, Thermo Fisher Scientific, Inc., 10x Genomics, QIAGEN, and Roche Diagnostics.

Additionally, supportive regulatory policies and ongoing investments in genomics research are further propelling market expansion. The entry of innovative players and the adoption of AI-driven sequencing workflows are expected to further accelerate the market’s evolution.

- In April 2025, Illumina and Tempus AI announced a partnership to accelerate clinical adoption of next generation sequencing and genomic AI. The partnership aims to produce evidence to support molecular profiling as a standard of care in the major diseases, with Illumina's AI and Tempus's multimodal data to benefit patient outcomes.

Key Market Highlights

- The U.S. next generation sequencing market size was valued at USD 13.18 billion in 2025.

- The market is projected to grow at a CAGR of 14.98% from 2026 to 2033.

- The NGS consumables segment garnered USD 6.50 billion in revenue in 2025.

- The sequencing segment is expected to reach USD 20.22 billion by 2033.

- The WGS segment is anticipated to witness the fastest CAGR of 15.60% during the forecast period.

- The oncology segment held a market share of 25.66% in 2025.

- The academic & government research institutes segment is expected to reach USD 4.93 billion in revenue in 2025.

How is the increasing incorporation of NGS into routine clinical decision making fueling the growth of the U.S. next generation sequencing market?

The increasing use of next generation sequencing (NGS) in routine clinical decision making is fueling the growth of the U.S. NGS market. Physicians can examine the patient’s genetic profile to determine disease risk, identify mutations, and select targeted therapies, instead of relying on symptoms to make a diagnosis, especially in oncology and rare disease treatment.

This shift toward precision medicine is driven by expanding test menus, improving reimbursement for clinical applications, and increasing physician confidence in genomic data. The use of NGS as a standard part of diagnosis and treatment planning, rather than just a research tool, results in a steady, recurring demand for sequencing instruments, reagents, and consumables. Clinical adoption is one of the most consistent long-term growth engines for the market.

- In May 2025, Roche partnered with Broad Clinical Labs to develop applications for their SBX sequencing technology, beginning with whole genome sequencing in critically ill newborns and their parents. The partnership is intended to bring rapid, scalable sequencing into routine use in neonatal care and biomedical research.

How does the growing complexity of genomic data hinder the growth of the U.S. next generation sequencing market?

The increasing use of sequencing is outpacing the ability of laboratories and healthcare organizations to store, integrate and analyze data, particularly where sophisticated bioinformatics infrastructure has not been established. This disconnects the collection of genetic information from its translation into clinically-driven insights.

The industry is addressing this challenge through better software and AI-enabled analysis platforms. The integration of advanced genomic intelligence tools into existing software suites and improvements to genomics analysis platforms are helping to make data interpretation easier and readily usable. The bioinformatics landscape is constantly innovating to help mitigate this challenge and ensure that data complexity does not sustain as a limiting factor for the market’s growth.

One of the most important trends in the U.S. NGS market is the increasing adoption of AI in the sequencing workflow. AI is being integrated into NGS to streamline workflows and data analysis, enhancing efficiency and accuracy across applications like oncology, drug discovery, and clinical diagnostics. By automating data interpretation, AI helps labs manage the massive volumes of genomic information generated during sequencing, easing the data complexity challenges the market faces today.

This shift is also evident in cloud and AI analytics that shorten sample-to-report times and improve data quality. As sequencing platforms continue to evolve alongside smarter software, AI is becoming integral and is transitioning from a supplementary tool to a core component of how NGS data is processed, interpreted, and applied in real-world clinical and research settings.

- In June 2026, Tempus AI announced the upcoming clinical availability of xH, a next generation sequencing (NGS) assay that uses whole-genome sequencing for blood cancers. xH showed high accuracy and precision and identified 40% more actionable findings than standard methods. Commercial launch is expected later this year.

U.S. Next Generation Sequencing Market Report Snapshot

|

Segmentation

|

Details

|

|

By Offering

|

NGS Consumables, NGS Platforms/Instruments, NGS Services, and Bioinformatics Software & Solutions

|

|

By Workflow

|

Pre-Sequencing, Sequencing, and Data Analysis

|

|

By Technology

|

WGS, Whole Exome Sequencing, Targeted Sequencing & Resequencing, and Others

|

|

By Application

|

Oncology, Reproductive Health, Infectious Disease, Rare Genetic Disorders, Pharmacogenomics & Drug Discovery, Agriculture & Animal Research, Consumer Genomics, and Others

|

|

By End User

|

Academic & Government Research Institutes, Clinical Laboratories & Hospitals, Pharmaceutical Companies, Biotechnology Companies, and Others

|

|

By Region

|

U.S.

|

Market Segmentation

- By Offering (NGS Consumables, NGS Platforms/Instruments, NGS Services, and Bioinformatics Software & Solutions): The NGS consumables segment accounted for USD 6.50 billion in 2025 due to the constant and frequent demand for reagents, kits, and other consumables in sequencing workflows. High test volumes and growing applications in the clinical and research sectors are other factors responsible for this market share.

- By Workflow (Pre-Sequencing, Sequencing, and Data Analysis): The sequencing segment held a market share of 51.83% in 2025 due to the central role of sequencing processes in generating high-throughput genomic data. The market's dominance was further strengthened by the use of advanced platforms and the rising number of samples.

- By Technology (WGS, Whole Exome Sequencing, Targeted Sequencing & Resequencing, and Others): The targeted sequencing & resequencing segment is projected to reach USD 17.63 billion by 2033, owing to cost-effectiveness, high sensitivity, and the ability to identify specific genetic variants. The rise in targeted panel usage in diagnostics and precision medicine is further propelling the segment’s growth.

- By Application (Oncology, Reproductive Health, Infectious Disease, Rare Genetic Disorders, Pharmacogenomics & Drug Discovery, Agriculture & Animal Research, Consumer Genomics, and Others): The oncology segment is projected to grow at a CAGR of 15.82% during the forecast period due to the increasing adoption of NGS for cancer diagnostics, selection of personalized treatment, and monitoring of minimal residual disease, which leads to better patient outcomes.

- By End User (Academic & Government Research Institutes, Clinical Laboratories & Hospitals, Pharmaceutical Companies, Biotechnology Companies, and Others): The academic & government research institutes segment accounted for USD 4.93 billion in 2025 owing to heavy funding for genomics research, large-scale sequencing projects, and high adoption of NGS platforms in academic institutes for scientific discovery and innovation.

What are the key use cases of next generation sequencing in the U.S.?

Next generation sequencing is finding applications across a wide range of real-world settings in the United States, reflecting its growing versatility beyond research environments. In oncology, NGS is being used through liquid biopsy to sequence circulating tumor DNA, enabling non-invasive, real-time monitoring of cancer progression and supporting early detection. Notably, in March 2026, Illumina and Labcorp expanded their partnership to advance precision oncology by increasing access to NGS and developing new genomic profiling solutions. They will also co-commercialize FDA-approved tissue and liquid biopsy test kits to provide more timely, equitable cancer care and support targeted therapies. Beyond oncology, NGS is increasingly applied in newborn genetic screening, pharmacogenomics, infectious disease surveillance, and rare disease diagnosis across the U.S.

Regulatory Frameworks

- The U.S. Food and Drug Administration’s Guidance on NGS-Based In Vitro Diagnostics for Germline Diseases regulates the development and validation of NGS tests. It provides recommendations to ensure the reliability and clinical validity of NGS diagnostics.

- The U.S. HIPAA Privacy Rule regulates the protection of patient genetic data. It establishes requirements to ensure confidentiality and security for personal health information generated by next generation sequencing, safeguarding sensitive genomic data from unauthorized access or disclosure.

Competitive Landscape

The U.S. NGS market is moderately consolidated, with a mix of established life sciences giants and emerging innovators competing for market share. Leading players maintain dominance through extensive product portfolios spanning instruments, reagents, and bioinformatics software, while smaller and newer entrants compete by focusing on niche applications such as long-read sequencing, single-cell analysis, or portable benchtop platforms.

Strategic mergers, acquisitions, and partnerships remain central to growth, as companies seek to expand their technological capabilities, multiomics offerings, and clinical applications. Increasing collaboration between sequencing platform providers, software developers, and healthcare institutions is also reshaping the competitive environment, pushing companies to innovate with respect to speed, accuracy, and affordability to maintain their market position.

- In June 2026, Hartwig Medical Foundation and Ultima Genomics deepened their partnership by adopting Ultima’s UG200 sequencing system to accelerate whole-genome sequencing in oncology. The partnership aims to make WGS more accessible, precise, and routine for cancer diagnosis and monitoring, including MRD detection.

Key Companies In The U.S. Next Generation Sequencing Market

- Illumina, Inc.

- Agilent Technologies, Inc.

- DH Life Sciences, LLC.

- Bio-Rad Laboratories, Inc.

- BD (Becton, Dickinson and Company)

- Clear Labs, Inc.

- Ultima Genomics, Inc.

- Element Biosciences

- Twist Bioscience

- Oxford Nanopore Technologies plc.

- GENEWIZ

- Thermo Fisher Scientific, Inc.

- 10x Genomics

- QIAGEN

- Roche Diagnostics

Recent Developments

- In February 2026, Ultima Genomics introduced the UG200 Series and Solaris 2.0 workflows, providing next generation sequencing at scale with twice the output, half the runtime and better genomic coverage of the UG 100. The UG200 Series offers flexible, high throughput solutions, designed to make genomics research and clinical use more cost effective and time efficient.

- In March 2026, Minaris launched AgentSCREEN, a GMP-qualified next generation sequencing platform for adventitious virus detection in cell banks and cell-based samples. Offering a 28-day turnaround, U.S.-based support, and broad viral detection, AgentSCREEN simplifies viral safety testing and aligns with regulatory guidance for advanced biologics and cell/gene therapies.

- In October 2024, Illumina released its benchtop sequencer MiSeq i100 series which includes bench-top sequencers with easy to use software and room-temperature kit storage. The new systems allow for same-day sequencing, reduce environmental impact and costs, and are designed to make next generation sequencing accessible to more U.S. labs.

- In October 2024, Myriad Genetics and Ultima Genomics announced a collaboration to explore the UG 100 NGS platform to advance clinical tests in oncology and reproductive genomics. The partnership is designed to enhance test performance, reduce costs and enable high-fidelity sequencing for Myriad’s Precise MRD and FirstGene offerings.