Market Definition

The insurtech market refers to the ecosystem of technology-driven insurance solutions that enhance the distribution, underwriting, and servicing of insurance products. The U.S. insurtech market involves multiple distribution models, including direct-to-consumer digital platforms, comparison aggregators, digital brokers, managing general agents (MGAs), embedded insurance channels, and traditional agent- or broker-assisted networks. These models cater to the end users across small and medium-sized enterprises, large enterprises, the public sector, or individuals.

Insurtech Market Overview

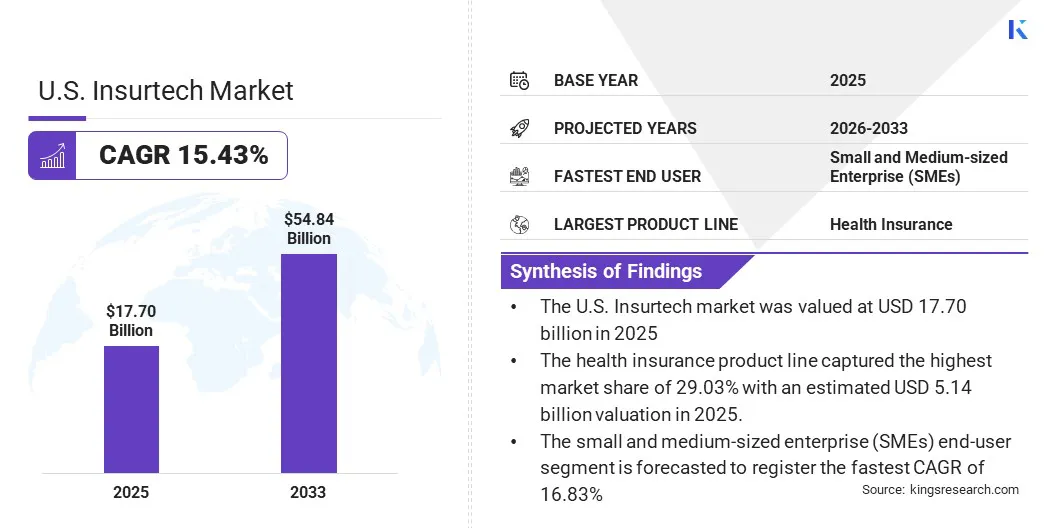

The U.S. insurtech market size was valued at USD 17.70 billion in 2025 and is projected to reach USD 54.84 billion by 2033, representing a CAGR of 15.43% over the forecast period. The market is driven by rising demand for faster, digital, and personalized insurance services. Additionally, the adoption of artificial intelligence in underwriting, claims automation, and customer-centric digital services is propelling growth in the U.S. insurtech market.

Key players in the market include Guidewire Software, Inc., Root Inc., Ethos Technologies Inc., Hippo Holdings Inc., Duck Creek Technologies, Acrisure, LLC, AgentSync Inc., Snapsheet, EvolutionIQ, Pie Group Holdings, Inc., and others. These companies are upgrading their technology platforms by integrating advanced technologies such as artificial intelligence and advanced analytics to offer personalized insurance products and services. The offerings include underwriting, claims automation, usage-based insurance, data-driven risk assessment, and real-time customer support to increase efficiency and consumer convenience. Additionally, rising consumer expectations, competition from tech-savvy entrants, and mobile adoption drive insurers to invest in digital-led solutions.

- In June 2025, Snapsheet enhanced its AI-driven insurance claims management platform with the integration of its conversational AI solutions, including LISA, ADDI, FloatSpace and FloatAgent. The integrated platform automates as much as 80% of First Notice of Loss (FNOL) submissions and simplifies claims intake, policyholder communication and documentation workflows. The development enables insurers to boost the efficiency of claims processing, reduce operational costs by approximately 40% and help adjusters save up to 40 hours per month through AI-powered workflow automation.

Key Market Highlights:

- The U.S. Insurtech market size was recorded at USD 17.70 billion in 2025.

- The market is projected to grow at a CAGR of 15.43% from 2026 to 2033.

- The health insurance product line captured the highest market share of 29.03% with an estimated USD 5.14 billion valuation in 2025.

- The embedded insurance distribution model registered the fastest growth rate of 15.86% over the forecast period.

- The small and medium-sized enterprise (SMEs) end-user segment is forecasted to register the fastest CAGR of 16.83%, reaching a valuation of USD 16.61 billion in 2033.

How is the adoption of artificial intelligence and machine learning across the U.S. insurtech sector driving market growth?

Artificial intelligence (AI) and machine learning utilize large amounts of data to outperform manual tasks, including statistical analysis, admin tasks, and processing claims in the insurance sector. LLMs accelerate claims management workflow by processing, extracting, and summarizing large unstructured text to help with claims triaging, litigation detection, claims evaluation, and subrogation and claims closure. Moreover, the deployment of machine learning enables efficient fraud detection during first notice of loss (FNOL), predicts claims complexities, supports cost predictions, and enhances the customer experience by predicting claims re-openings.

According to the Insurance AI Use Case Tracker by Evident, nearly 68% of publicly disclosed insurance AI deployments were generative or agentic, with agentic AI accounting for 21% of deployments, thereby indicating the implementation of AI in insurance as increasingly operational. Additionally, the inclusion of an AI chatbot to address customer grievances and claim settlement issues further fuels the adoption of AI in the U.S. insurtech market.

- In January 2026, Allianz partnered with Anthropic to expand AI use across operations, including employee productivity enhancement, automating claims and insurance workflows, and ensuring transparent AI decision-making.

- In November 2025, Chubb launched an AI-powered optimization engine within its Chubb Studio platform to enable digital partners to deliver personalized insurance offers at the point of sale. The solution utilizes AI-driven insights to recommend relevant insurance products, improve customer engagement, increase conversion rates, and provide real-time performance analytics, flexible integration options, and click-to-engage features for seamless customer interactions.

How is legacy insurance infrastructure restraining market growth in the U.S. Insurtech sector?

Legacy systems comprise outdated frameworks that are generally incompatible with modern technologies such as AI, blockchain, and cloud computing, which are crucial for scaling. The migration from conventional insurtech systems to advanced ones makes traditional firms vulnerable to agile Insurtech competition. The upgrade further acts as a massive drain on enterprise resources, as a significant portion of the IT budget in traditional insurance firms is spent on maintaining systems that are incompatible with modern technology.

To address the challenge, market players are transitioning their focus from maintaining legacy technology to building scalable, AI-enabled operations. Conventional insurers are identifying operational costs, profitability, expense ratios, and growth as their highest priorities. The players are further adopting cloud-native platforms, advanced data analytics, and AI-driven scalable operating models to accelerate innovation.

- In April 2026, Hippo Holdings released Clara from Claims, which is a 24/7 conversational AI agent that enables a fully digital, always-on FNOL experience. The agent captures and structures claim data in real time, flagging inconsistencies and routing claims intelligently to accelerate resolution.

- In March 2025, Frankenmuth Insurance selected Guidewire InsuranceSuite on Guidewire Cloud to modernize its core systems and streamline IT operations by migrating from its on-premises environment. The cloud migration enables the insurer to improve scalability and reduce system maintenance.

- In February 2025, Markel Group Inc. migrated Guidewire ClaimCenter from an on-premises environment to Guidewire Cloud across its U.S. specialty insurance business. The company further laid down plans to migrate Guidewire BillingCenter to the cloud and selected ClaimCenter for its International Wholesale operations.

How is the adoption of blockchain and smart contracts emerging as a notable trend in the U.S. Insurtech market?

Advancements in blockchain technologies and smart contracts offer transformative solutions to industry pain points comprising manual processes, excessive paperwork, fraudulent activities, and lack of transparency. Blockchain provides a decentralized, transparent, and auditable record of all transactions and modifications, which enables users to validate insurance policies, claims, and payments. Furthermore, the property of blockchain to reduce the risk of data manipulation, unauthorized changes and the elimination of intermediaries comprising brokers or third-party administrators, drive its adoption in the U.S. insurtech market.

Additionally, smart contracts (self-executing digital contracts) complement blockchain technology by enabling automated and tamper-proof agreements. This results in streamlined operations, reduced expenditure, and trust enhancement in insurance transactions. This also reduces operational costs, fraud risk, and settlement times while improving transparency, accuracy, and trust in insurance transactions.

- In February 2026, the Institutes RiskStream Collaborative launched RAPID X, which is the first live blockchain-based claims data exchange platform in the U.S. insurance industry. The platform accelerates the first notice of loss (FNOL) process by an average of seven days while ensuring secure, privacy-compliant data sharing.

- In September 2025, Reliance Global Group, Inc. announced a strategic expansion into cryptocurrency and blockchain-based insurance-linked assets. The company is exploring tokenization of insurance-linked assets to create a new investment class aimed at improving transparency, liquidity, and efficiency.

- In June 2025, SurancePlus introduced SurancePlus to its Midnight Blockchain network, which supports privacy-compliant transactions using zero-knowledge proof technology. It further offers privacy-focused, compliant digital asset transactions and aims to provide institutional investors with secure access to tokenized reinsurance products.

Insurtech Market Report Snapshot

|

Segmentation

|

Details

|

|

By Product Line

|

Life Insurance, Health Insurance, Property Insurance, Casualty Insurance, Specialty Insurance

|

|

By Distribution Model

|

Direct-to-Consumer Digital, Aggregators / Comparison Platforms, Digital Brokers, MGAs, Embedded Insurance, Bancassurance, Agent/Broker Assisted

|

|

By End User

|

Individual Consumers, SMEs, Large Enterprises, Government & Public Sector

|

|

By Country

|

U.S.

|

Market Segmentation

- By Product Line (Life Insurance, Health Insurance, Property Insurance, Casualty Insurance, Specialty Insurance). The health insurance product captures the highest market share, at 29.03% in 2025, with a valuation of USD 5.14 billion. The high share is attributed to rising healthcare costs and surging demand for comprehensive medical coverage through digital insurance platforms.

- By Distribution Model (Direct-to-Consumer Digital, Aggregators / Comparison Platforms, Digital Brokers, MGAs, Embedded Insurance, Bancassurance, Agent/Broker Assisted). The embedded insurance is estimated to register the fastest growth rate of 15.86% over the forecast period, reaching USD 4.52 billion in 2033. The high share is due to the expansion of insurance offerings into e-commerce, fintech, travel, mobility, and other digital ecosystems, enabling seamless point-of-sale policy purchases.

- By End User (Individual Consumers, SMEs, Large Enterprises, Government & Public Sector). The small and medium-sized enterprise (SMEs) end-user segment was valued at USD 4.80 billion in 2025 and is anticipated to register the fastest CAGR of 16.83% over the forecast period. The high growth rate is due to the adoption of affordable digital insurance solutions to protect against operational, cyber, liability, and business continuity risks.

The U.S. is designated as a premier hub for insurance and its vast software development ecosystem, which fosters the adoption of technology in the insurtech sector to develop customer-oriented offerings. Innovations in the market are occurring across the entire insurance value chain, ranging from distribution, marketing, product design, underwriting, to claims management including all lines of insurance-property and casualty, life and health. The distribution is capturing the highest focus as insurtech market players are acquiring new customers through novel distribution mediums where AI analyzes and provides custom insurance offerings on the basis of individual requirements. This transition is attributed to the generational shifts in how people communicate, access information, and make purchase decisions, while complementing rather than replacing traditional distribution channels.

Market players are further operationalizing artificial intelligence to transition beyond pilot projects towards embedding AI directly into core insurance business processes. Insurtech companies in the U.S. are enabling AI-enabled software development, real-time AI-enhanced operational support, and AI-powered business applications.

- In December 2025, Zywave introduced its Agentic AI strategy and a new suite of insurance-focused AI agents to improve productivity and drive organic growth for brokers and carriers. The agent’s key workflows comprise prospect identification, lead sourcing, data enrichment, and personalized outreach, thus reducing manual effort and boosting client acquisition.

Regulatory Frameworks

- The NAIC Insurance Data Security Model Law is a regulatory framework that establishes baseline cybersecurity standards for the U.S. insurance industry. The framework is implemented across 28 state jurisdictions in the U.S. and is designed to protect consumer nonpublic information (NPI) and mitigate data breach damages.

- The Gramm-Leach-Bliley Act (GLBA) requires all state insurance authorities to adopt standards relating to the privacy and disclosure of nonpublic personal financial information applicable to the insurance industry.

Competitive Landscape

Key players operating in the market are incorporating strategic mergers, acquisitions, and technical partnerships to capture a wider share. The players in the U.S. insurtech market are prioritizing the development of multi-agent systems and AI copilots that improve decision-making, operational efficiency, and scalability across business functions. According to Financial Technology Partners, Insurtech financing volume reached USD 7.2 billion across 304 transactions, with mergers and acquisitions recording their highest-ever deal count of 190 transactions with over USD 22 billion in total volume. 45% of the total insurtech funding was acquired by AI-native companies in 2025, where financing was received from companies including CyberCube, Nirvana, Quantexa, and Angle Health. Notable acquisition partners in the market were American Family Ventures with nine total investments, followed by MTech Capital and Greenlight Re, General Catalyst, and Clocktower Technology Ventures with eight investments.

- In December 2025, Majesco released its operational strategy focusing on strengthening Property and Casualty (P&C) insurance, and Life & Annuity, and Health (L&AH) markets through AI investments. The plans to build advanced AI-native SaaS platforms to enhance underwriting, claims, billing, and policy operations.

- In May 2025, Acrisure raised USD 2.1 billion in a funding round led by Bain Capital, valuing the company at USD 32 billion. The funding will be utilized to accelerate transformation into a technology-enabled financial services platform that delivers cybersecurity, payroll, payments, real estate, and wealth management services.

- In May 2025, Aviva plc partnered with CyberCube to integrate AI-driven cyber risk analytics to improve its cyber exposure management. The company plans to leverage large language models (LLMs) and Portfolio Threat Actor Intelligence of CyberCube to analyze ransomware behavior and target technologies.

Key Companies In The U.S. Insurtech Market :

- Acrisure, LLC

- AgentSync Inc.

- Bold Penguin Inc.

- Duck Creek Technologies

- Ethos Technologies Inc.

- EvolutionIQ

- Guidewire Software, Inc.

- Hippo Holdings Inc.

- Insurify, Inc.

- Kin Insurance, Inc.

- Lemonade

- Majesco

- Pie Group Holdings, Inc.

- Root Inc.

- Snapsheet

Recent Developments

- In June 2026, Southern Trust Insurance Company selected Duck Creek Embedded Payments and Duck Creek Policyholder Portal to modernize its insurance billing and digital payments experience. The process enables Southern Trust to offer flexible digital payment options, improve payment visibility and reconciliation, and provide policyholders with secure self-service access to billing and account information.

- In April 2026, Hashgraph partnered with The Institutes RiskStream Collaborative to develop a new property risk and resilience data solution for the insurance industry. The system built on Hedera and Hashgraph’s HashSphere uses a hybrid blockchain model that combines private and public ledgers.

- In December 2025, Bold Penguin Inc. announced a partnership with Adaptive Insurance to expand coverage options available through the Bold Penguin Placement Desk. The collaboration is focused on the GridProtect product of Adaptive, which provides payouts for losses caused by power outages.