Market Definition

The market comprises enterprise solutions and services that allow organizations to track, govern, optimize, and monetize software licenses across on-premise and cloud environments. The market is critical for controlling IT spend, ensuring vendor compliance, and reducing operational risk. Market growth is driven by cloud adoption, subscription-based licensing, and rising audit exposure across BFSI, healthcare, IT & telecommunication, retail & e-commerce sectors.

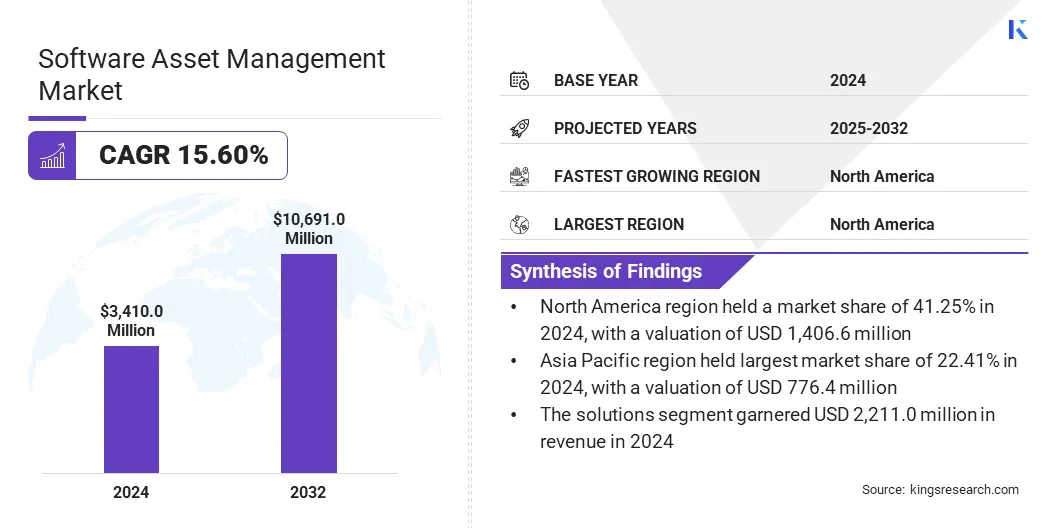

Software Asset Management Market Overview

The global software asset management market size was valued at USD 3,410 million in 2024 and is projected to grow from USD 3,874.5 million in 2025 to USD 10,691.02 million by 2032, exhibiting a CAGR of 15.6% over the forecast period. This growth is fueled by the increasing complexity of software licensing, accelerated cloud adoption, and rising regulatory scrutiny. Growing usage across BFSI, healthcare, and IT enterprises enables cost optimization, compliance, and scalable governance, creating strong near-term growth opportunities globally.

Major companies operating in the software asset management industry are Flexera, Ivanti, Certero, Eracent, Snow Software, BMC Software, Matrix42, USU Software AG, ServiceNow, Broadcom, and others.

The growing complexity of software portfolios, frequent vendor audits, and the shift toward subscription-based licensing are driving global adoption of software asset management. Both SMEs and large enterprises are implementing integrated solutions to enhance cost transparency and ensure compliance across on-premise and cloud environments.

Strong demand from BFSI, healthcare, IT & telecommunications, and retail & e-commerce is further accelerating market growth. Additionally, ongoing digital transformation and cloud migration initiatives create a timely opportunity for vendors to offer scalable, analytics-driven SAM platforms.

- In June 2024, IFS entered a definitive agreement to acquire Copperleaf Technologies, integrating advanced AI-powered decision analytics into its enterprise asset management portfolio. The acquisition strengthens clinical and operational efficiency for asset-intensive industries, including utilities and energy, by optimizing-term capital investment planning and asset lifecycle management.

Key Highlights:

- The software asset management industry size was recorded at USD 3410.0 million in 2024.

- The market is projected to grow at a CAGR of 15.6% from 2025 to 2032.

- North America held a share of 41.2% in 2024, valued at USD 1,406.6 million.

- The solution segment generated USD 2,2,11.04 million in revenue in 2024.

- The cloud segment generated a revenue of USD 1,982.9 million in 2024.

- The small & medium enterprises segment is anticipated to witness the fastest CAGR of 17.46% over the forecast period.

- The BFSI segment accounted for a share of 28.25% in 2024, valued at USD 963.33 million.

- Asia Pacific is anticipated to grow at a CAGR of 16.71% through the projection period.

Why Is the Growing Complexity of Hybrid IT and SaaS Sprawl Boosting Market Expansion?

The rising complexity of hybrid IT infrastructures is making software usage harder to track across on-premise systems, cloud platforms, and decentralized SaaS applications. As software spending grows, organizations are prioritizing cost optimization and compliance to avoid unplanned expenses and vendor audit penalties.

This is accelerating adoption of cloud-based software asset management solutions and managed services that provide centralized visibility, automated license tracking, and risk mitigation, thereby directly fueling growth in the software asset management market.

- In June 2024, Freshworks Inc. acquired Device42 to integrate advanced asset discovery into its ITSM platform. This expansion improves software asset management by providing a unified data source. It allows enterprises to reduce compliance risks, optimize IT infrastructure costs, and accelerate incident resolution through improved visibility.

How is the complexity of integrating SAM solutions hindering market expansion?

Key challenge limiting the growth of the software asset management market is the complexity of integrating SAM solutions across hybrid on premise and cloud environments. Budget constraints and limited technical expertise hinder adoption among small and medium-sized enterprises, while fragmented software inventories remain a critical barrier for large enterprises.

To address this challenge, vendors are enhancing cloud-native and hybrid-compatible SAM platforms with standardized connectors and automated discovery tools. In parallel, solution providers are expanding managed and advisory services to support SMEs with limited in-house expertise, while analytics-driven compliance engines simplify licensing intelligence and reduce audit risk across BFSI and healthcare.

How is the convergence of cloud-native intelligence and automated compliance reshaping global software asset management market?

The market is witnessing a strategic shift toward cloud-native solutions that integrate automated discovery with predictive analytics to optimize licensing expenditures. This trend is fueling the market by enabling organizations to gain real-time visibility into software usage while proactively controlling licensing costs.

Cloud-native platforms combined with automated discovery and predictive analytics help enterprises, particularly in BFSI and healthcare, minimize compliance gaps and audit exposure. At the same time, the growing adoption of managed services lowers operational complexity for SMEs, making advanced SAM capabilities more accessible across increasingly complex SaaS environments.

- In September 2024, ServiceNow enhanced its Software Asset Management capabilities with the Xanadu platform release, introducing improved SaaS usage tracking, cost optimization, and automation. These updates help organizations gain clearer visibility into software assets, reduce unnecessary spending, and make better-informed decisions across the software lifecycle.

Software Asset Management Market Report Snapshot

|

Segmentation

|

Details

|

|

By Component

|

Solution, Services

|

|

By Deployment

|

On-Premise, Cloud

|

|

By Organization Size

|

Small & Medium Enterprises, Large Enterprises

|

|

By Application

|

BFSI, Healthcare, IT & Telecommunication, Retail & E-commerce, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Component (Solution and Services): The solution segment earned USD 2,211.04 million in 2024, primarily driven by accelerated enterprise cloud migration and the integration of advanced analytics to optimize operational efficiencies across core business functions.

- By Deployment (On-Premise and Cloud): The on-premise segment held a share of 41.8% in 2024, fueled by strict data sovereignty regulations and the requirement for high-performance, low-latency processing within localized corporate infrastructures.

- By Organization Size (Small & Medium Enterprises andLarge Enterprises): The small & medium enterprises segment is projected to reach USD 3,822.49 million by 2032, largely due to increased adoption of cost-effective SaaS models and government-led digitalization initiatives aimed at enhancing global competitiveness.

- By Application (BFSI, Healthcare, IT & Telecommunication, Retail & E-commerce, and Others): The healthcare segment is projected to reach USD 1,296.80 million by 2032, owing to surging demand for remote patient monitoring and the mandated integration of electronic health records to enhance clinical decision-making

What is the market scenario in North America and the Asia Pacific region?

Based on region, the software asset management market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

The North America software asset management market accounted for a 41.2% share in 2024, valued at USD 1,406.6 million. The market is expected to expand at a CAGR of 14.8% from 2025 to 2032. Growth is driven by widespread SAM adoption across IT ecosystems and stringent software compliance requirements in the BFSI, IT & telecommunications, and healthcare sectors to manage licensing costs and mitigate audit risks.

- In July 2025, Flexera expanded its portfolio with the Flexera One SaaS Management solution, integrating SAM and SaaS discovery and optimization capabilities, including legacy Snow Software assets, to enhance organizational visibility and control over SaaS applications.

The Asia-Pacific software asset management industry is projected to grow at a CAGR of 16.7% during the forecast period. This expansion is driven by accelerating digital transformation across SMEs and large enterprises, particularly in retail & e-commerce and healthcare.

Increased adoption of cloud-based, solution-led offerings, valued for scalability and reduced upfront costs, along with ongoing IT modernization, rising software adoption, and heightened awareness of license governance, reinforces the region’s long-term growth potential for software asset management providers.

Regulatory Frameworks

- In the U.S., software asset management practices are shaped by intellectual property laws, contract compliance standards, and audit rights under federal and state regulations that govern software licensing and usage transparency.

- In the EU, software asset management is governed by GDPR, software copyright directives, and contractual compliance frameworks, requiring enterprises to maintain accurate software inventories and ensure lawful processing of usage data.

- In Asia Pacific, regulatory oversight is evolving, with countries strengthening software licensing enforcement, data localization rules, and cyber governance frameworks to support digital transformation while reducing software piracy and compliance risks.

- In Japan, regulatory guidance emphasizes strict adherence to software licensing agreements and data protection laws, prompting enterprises to deploy structured asset management systems to support audit readiness and operational accountability.

Competitive Landscape

The global software asset management industry is moderately fragmented, comprising established enterprise software vendors and specialized service providers. Key players like Broadcom and Flexera offer integrated, scalable solutions through extensive IT management portfolios, while niche vendors concentrate on license optimization, cloud governance, and managed services. This competitive landscape fosters continuous innovation, strategic partnerships, and ongoing enhancement of compliance-focused capabilities worldwide.

- In February 2024, Softchoice launched SAM+, a service suite optimized for subscription-based licensing. This solution addresses the shift toward recurring cost models. It allows small to large enterprises to improve visibility, reduce upfront investment, and maximize ROI across cloud and on premise deployments.

Key Companies in Software Asset Management Market:

- Flexera

- Ivanti

- Certero

- Eracent

- Snow Software

- BMC Software

- Matrix42

- USU Software AG

- ServiceNow

- Broadcom

- IFS

- Zluri

- Crayon

- DXC Technology Company

- Softchoice

Recent Developments (Product Launch)

- In July 2025, Flexera launched a unified SaaS management solution that integrates Snow’s capabilities to address shadow AI and rising cloud costs. This solution is designed to improve visibility into unsanctioned application usage. It enables enterprises to reduce security risks, eliminate overlapping tools, and optimize spending across complex, AI-driven digital ecosystems.