Market Definition

The sodium-ion battery market involves the production of sodium-ion-based battery systems that use sodium ions as the primary charge carriers. The market is gaining prominence due to the low cost of the technology and the fast-charging capabilities of the batteries. This, in turn, makes these batteries suitable across a diverse array of end-use domains, ranging from automotive and consumer electronics to large grid-scale energy storage systems.

The market includes multiple battery chemistries and configurations such as sodium-sulfur, sodium-nickel chloride (ZEBRA), and other emerging sodium-based technologies, available in various formats including cylindrical, prismatic, pouch, and other specialized designs. These batteries utilize different electrolyte systems, thus offering varied energy densities, cycle life, safety, cost efficiency, and thermal stability to support emerging applications across diverse end-use verticals.

Sodium-Ion Battery Market Overview

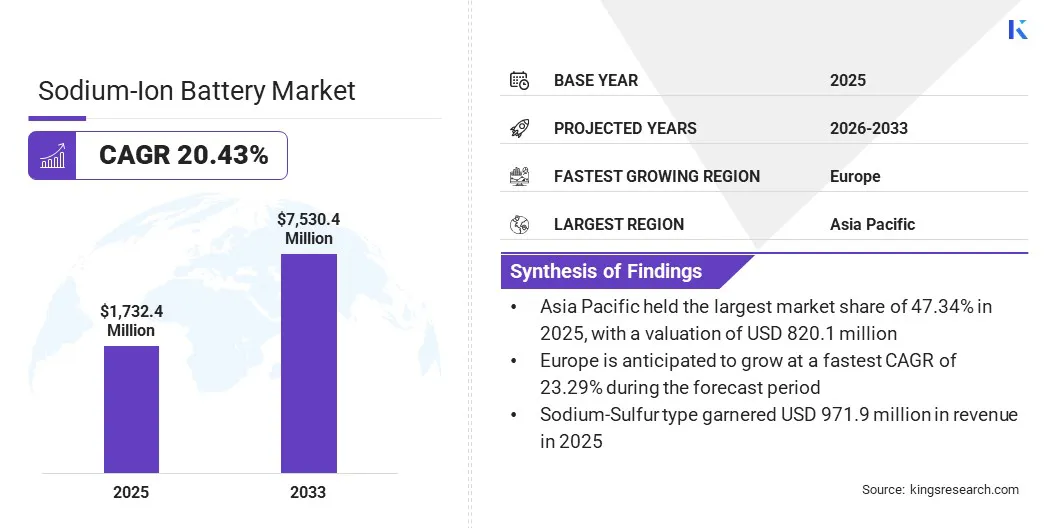

The global sodium-ion battery market size was valued at USD 1732.40 million in 2025 and is projected to reach USD 7530.44 million by 2033, representing a CAGR of 20.43% over the forecast period. This notable growth is driven by the rising demand for low-cost, environmentally friendly battery chemistries for deployment across large-scale grid energy storage systems and automotive end-use sectors. Additionally, the ability of sodium-ion batteries to reach 90% charge capacity in approximately 12 minutes, along with their stable performance at temperatures ranging from -40°C to 80°C, makes them a prime choice for addressing energy storage needs in colder climates.

Major companies operating in the global sodium-ion battery industry include CATL, Faradion, HiNa Battery Technology Co., Ltd., Natron Energy, TIAMAT SAS, BYD Co., Ltd., Indi Energy, VEKEN, Rechargion Energy Private Limited, AMTE Power, Pylon Technologies Co., Ltd., Samsung SDI, LG Chem, ProLogium Technology CO., Ltd., and TOSHIBA CORPORATION.

Businesses across diverse end-user industries such as automotive, stationary energy storage, and industrial power are adopting sodium-ion batteries (SIBs) to capitalize on their superior safety, low-temperature performance, and cost-effectiveness. The market is witnessing a strategic transition to the adoption of sodium-ion batteries due to their low cost and rapid charging capabilities, particularly for entry-level electric vehicles and large-scale renewable energy firming. Additionally, the high cost and volatile supply of critical battery minerals such as lithium further fuel the shift toward abundant metal sodium-based battery chemistries.

- In May 2024, the second-phase expansion of the Fulin Sodium-ion battery energy storage station was carried out in Nanning, Guangxi Zhuang Autonomous Region, China. The plant commenced operations with 10,000 kWh of newly generated sodium-ion batteries, supplying electricity to up to 1,500 households. It is further planned to reach 100 MWh, generating 73 million kWh of clean electricity annually and reducing 50,000 tons of CO2 emissions.

Key Market Highlights:

- The global sodium-ion battery market size was recorded at USD 1732.40 million in 2025.

- The market is projected to grow at a CAGR of 20.43% from 2026 to 2033.

- Europe emerged as the fastest-growing market with a CAGR of 23.29% in 2025 and valuation of USD 377.3 million.

- Sodium sulfur segment garnered USD 971.9 million in revenue in 2025.

- Aqueous segment is expected to reach USD 4179.2 million by 2033.

- Cylindrical segment captured the largest share of 37.24% in 2025, with the valuation of USD 645.1 million.

- Energy storage segment held the majority share and was valued at USD 906 million in 2025.

- Asia Pacific captured the largest share of 47.34% in 2025.

How Does Raw Material Abundance, Processing Cost, And Price Stability Of Sodium-Ion Batteries Drive Market Expansion?

Sodium-ion batteries utilize sodium carbonate as the primary raw material, which is over 1,000 times more abundant than lithium and up to 500 times less expensive to process. According to the U.S. Geological Survey (USGS), the global reserves of sodium are estimated at 47 billion tons, compared to 150 million tons for lithium as of 2025.

Moreover, the stability in sodium carbonate prices, which are estimated at around USD 300 per ton compared to USD 13,000 - USD 80,000 per ton for lithium, reduces the exposure of sodium-ion battery production to geopolitical supply shocks. This provides an overall lower cost on a kilogram basis to sodium-ion batteries compared to lithium-based chemistries, acting as a major driving factor.

- In January 2026, Altris, a Swedish clean technology and battery development company, transitioned to large-scale development and deployment of sodium-ion battery technology. The company secured a major USD 22.4 million strategic in-kind investment and manufacturing partnership with Draslovka for the production of its patented sodium-ion cathode active material (CAM).

How Does Lower Energy Density Of Sodium-Ion Batteries Negatively Impact The Market Growth?

The lower energy density of sodium-ion batteries compared to lithium-ion alternatives limits their performance and adoption. With around 175 Wh/kg, they offer shorter driving ranges (up to 350 km) versus 400–600 km for lithium-ion batteries, making them less suitable for long-range applications like electric vehicles. Additionally, dependence on minerals such as nickel and manganese, which face supply chain constraints, further restricts large-scale deployment.

To address this, industry players are advancing battery chemistries and material innovations to improve energy density and overall performance. Efforts focus on enhancing electrode materials, optimizing cell design, and improving thermal stability to boost efficiency and reliability. These developments are expected to narrow the performance gap with lithium-ion batteries while retaining the cost and resource advantages of sodium-ion technology.

- In April 2026, CATL entered mass production of sodium-ion cells that are 30% cheaper than LFP batteries, which offer up to 600 km of driving range and a stable energy density of 175 Wh/kg. The company has also entered into a strategic partnership with Changan Automobile for the distribution of sodium-ion batteries to support the launch of sodium-ion-powered vehicles.

Advancements in cathode materials, particularly the adoption of Prussian blue analogues (PBAs), are emerging as a notable market trend. PBAs offer three-dimensional ion diffusion channels that enable fast-charging capabilities, minimize structural strain during cycling, and their low-cost, iron-based chemistry leads to a significant reduction in reliance on cobalt- and nickel-based cathodes.

Moreover, PBAs such as iron hexacyanoferrate (FeHCF) and copper hexacyanoferrate (CuHCF) exhibit high specific capacity, good cycling stability, strong structural stability, high voltage, and relatively simple synthesis processes. This makes PBAs a commercially attractive cathode option for sodium-ion batteries, offering potentially 20-30% lower production costs and fast charging capabilities compared to lithium-ion batteries. This, in turn, creates potential growth opportunities for sodium-ion batteries.

- In May 2025, the Jawaharlal Nehru Centre for Advanced Scientific Research (JNCASR), India, developed a super-fast charging sodium-ion battery based on NASICON-type cathode and anode materials, capable of reaching 80% charge in 6 minutes and lasting over 3,000 cycles.

Sodium-Ion Battery Market Report Snapshot

|

Segmentation

|

Details

|

|

By Type

|

Sodium-Salt (ZEBRA), Sodium-Sulfur, Sodium-Nickel Chloride

|

|

By Format

|

Cylindrical, Prismatic, Pouch, Others

|

|

By Electrolyte

|

Aqueous, Non-Aqueous

|

|

By End Use

|

Automotive, Energy Storage, Consumer Electronics, Telecommunications, Industrial, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Type (Sodium-Salt (ZEBRA), Sodium-Sulfur, and Sodium-Nickel Chloride). The sodium-sulfur segment generated USD 971.9 million in 2025 and is anticipated to register the highest CAGR of 20.98% over the forecast period. This growth is mainly fueled by its high energy density and long life cycle compared to other types. This growth is further supported by its potential applicability in electric vehicles (EVs) and energy storage systems.

- By Format (Cylindrical, Prismatic, Pouch, and Others). The cylindrical segment accounted for the largest share of 37.24% in 2025 and is estimated to register a CAGR of 15.63% over the forecast period. The high share is attributed to optimal space utilization, resulting in lower cost and reduced environmental impact. The cylindrical form factor further guarantees even pressure distribution, thus ensuring safety, durability, and high energy density.

- By Electrolyte (Aqueous and Non-Aqueous). The aqueous segment garnered USD 1075.8 million in 2025, accounting for the majority share of 62.10%. Its non-flammability, lower cost, easier manufacturing, and suitability for large-scale stationary energy storage and grid applications contribute to segmental growth.

- By End Use (Automotive, Energy Storage, Consumer Electronics, Telecommunications, Industrial, and Others). The energy storage segment was valued at USD 906.0 million in 2025, with a significant share of 52.30%. The rising demand for renewable energy integration, grid stabilization, and battery materials that offer lower cost, enhanced safety, and increased performance in colder climates is boosting the demand for scalable, cost-effective sodium-ion battery storage solutions.

What Is The Market Scenario In Asia Pacific And European Region?

Based on region, the global sodium-ion battery market is segmented into North America, Europe, Asia Pacific, Middle East and Africa, and South America.

The Asia-Pacific sodium-ion battery market captured a majority share of 47.34% and was valued at USD 820.1 million in 2025. This expansion is primarily driven by accelerated renewable energy deployment and grid storage expansion due to rising electrification needs, along with the extensive adoption of electric vehicles across fast-growing economies such as China, South Korea, India, and Southeast Asia. Additionally, the booming industrial and commercial infrastructure, along with an extensive technological research landscape across China, Japan, South Korea, and Southeast Asian economies, supports regional market growth.

- In May 2026, Beijing HyperStrong Technology Co., Ltd. (HyperStrong) and SMA Solar Technology AG (SMA) signed an agreement to advance global utility-scale energy storage projects. The agreement involves combining HyperStrong’s expertise in energy storage system integration with SMA’s inverter technology and global service capabilities. The collaboration is aimed at accelerating the global energy transition and the adoption of sustainable energy infrastructure by delivering reliable, flexible, and grid-compliant energy storage solutions.

The Europe sodium-ion battery market is set to register the fastest CAGR of 23.29% over the forecast period. This rapid growth is primarily propelled by increasing awareness regarding the social and environmental impacts of extracting and refining critical battery minerals, including lithium, gallium, boron, and tungsten. The concentration of lithium, nickel, and cobalt reserves in a few countries, particularly China, which accounts for nearly 70% of the global lithium refining capacity, exposes Europe to geopolitical and trade disruptions and subjects it to intense competition.

Sodium-based batteries are gaining prominence in Europe owing to their ability to counter battery supply chain challenges and reduce Europe’s reliance on Chinese-sourced battery raw materials and technologies.

- In May 2024, Europe passed the Critical Raw Materials (CRM) Act to secure and diversify the supply of essential materials needed for green, digital, space, and defense technologies. The Act focuses on strengthening domestic critical minerals extraction, processing, and recycling capacities while reducing dependence on single-country suppliers such as China. The Act further promotes the adoption of sustainable supply chains and circular economy approaches to enhance the resilience of the EU against global supply disruptions.

Regulatory Frameworks

- In the U.S., the U.S. Department of Transportation proposed new regulations in February 2026 for shipping sodium-ion batteries as part of a broader effort to align U.S. hazardous materials transportation regulations with international standards. According to the Pipeline and Hazardous Materials Safety Administration (PHMSA) Hazardous Materials Table under §172.101, UN3292 classifies batteries containing sodium metal as dangerous when wet and they are regulated strictly under the Hazardous Materials Regulations (HMR).

- In Europe, Regulation (EU) 2023/1542 concerning batteries and waste batteries replaces the existing Batteries Directive (2006/66/EC). The updated regulation mandates that all batteries placed on the EU market must be durable, safe, sustainable, and efficient by introducing new mandatory design, content, and conformity assessment requirements as a key initiative of the European Green Deal.

- In China, the China Quality Certification Center (CQC) introduced an initiative governed by the certification rule CQC13-464292-2025, which aligns with the national standard GB/T 44265-2024. The regulation targets sodium-ion batteries used in electric energy storage systems and mandates China Compulsory Certification (CCC) or battery registration for import or sale in China.

Competitive Landscape

Key players in the sodium-ion battery market are conducting extensive research to improve electrode performance, refine electrolyte formulations, enhance battery energy density, and scale up pilot manufacturing to address the growing demand for scalable energy storage systems in renewable energy, grid integration, and electric mobility, thereby reducing dependence on critical raw materials.

- In May 2026, Gotion High-Tech launched its new sodium-ion battery brand, Gnascent. The company launched three dedicated cell variants designed for high-energy applications, cold-weather performance, and long-life energy storage systems, with gigawatt-hour-scale manufacturing facilities in Tangshan and Hefei.

Additionally, market players are prioritizing strategic technical collaboration with established players to drive the transition to sodium-ion battery cell technology and electrode design, while advancing commercialization opportunities in next-generation energy storage and high-performance systems.

- In August 2025, NEO Battery Materials entered into a joint development agreement with South Korea-based NainTech to co-develop sodium-ion battery technologies for energy storage systems. The partnership aims to enhance the applicability of sodium-ion batteries in AI data center applications, power grid storage, and high-performance drones.

Key Companies in The Sodium-Ion Battery Market

- CATL

- Faradion

- HiNa Battery Technology Co., Ltd.

- Natron Energy

- TIAMAT SAS

- BYD Co., Ltd.

- Indi Energy

- VEKEN

- Rechargion Energy Private Limited

- AMTE Power

- Pylon Technologies Co., Ltd.

- Samsung SDI

- LG Chem

- ProLogium Technology CO., Ltd.

- TOSHIBA CORPORATION

Recent Developments

- In February 2025, CATL and CHANGAN launched the first mass-produced passenger vehicle that is powered by sodium-ion batteries and is capable of navigating icy roads and steep, snow-covered slopes at temperatures reaching −30°C, with an estimated driving range of 400 km.

- In April 2025, CATL introduced the Freevoy Dual-Power Battery, Naxtra, which is the world's first mass-produced sodium-ion battery. The Naxtra battery line comprises a passenger EV battery and a 24V heavy-duty truck start-stop battery capable of retaining 90% of its capacity at −40°C, while offering approximately 500 km range and over 10,000 cycles.

- In February 2025, Trentar Energy Solutions entered into a partnership with KPIT Technologies to commercialize sodium-ion battery technology. The collaboration involves a technology transfer agreement and further includes Trentar investing in the manufacturing capacity of 3 GWh sodium-ion batteries.