Market Definition

The power transformer market comprises the manufacturing, assembly, and commercialization of high-voltage transformers used for transmission and substation applications. The market covers equipment used to step up or step down voltage across power grids, industrial facilities, renewable energy projects, and infrastructure development. The growing demand for reliable electricity transmission, grid modernization, renewable energy integration, AI adoption, and expansion of high-voltage transmission networks is driving the growth of the market.

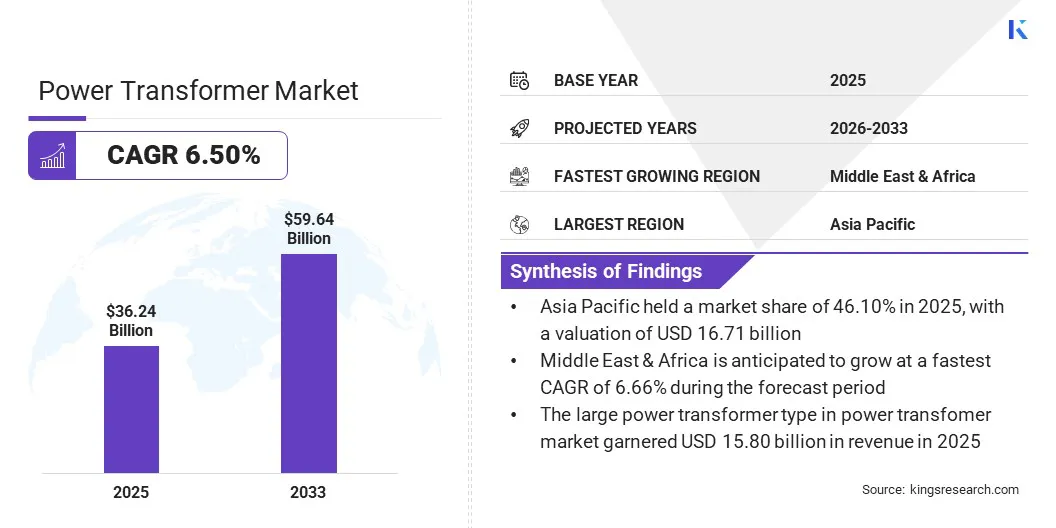

The global power transformer market was valued at USD 36.24 billion in 2025 and is projected to reach USD 59.64 billion by 2033, at a CAGR of 6.5% over the forecast period. Power transformers allow adjustment of voltage levels by stepping them up or down to suitable levels. This ensures long-distance transmission of power at high voltages and reduces voltage to safe levels for commercial and industrial use.

Major companies operating in the global power transformer industry are Hitachi Energy Ltd., Siemens AG, General Electric Company, Schneider Electric, Mitsubishi Electric Power Products, Inc., Toshiba International Corporation, HD Hyundai, TBEA Co., Ltd., WEG, Hyosung Heavy Industries, Fuji Electric Co., Ltd., LS Electric Co., Ltd., CG Power and Industrial Solutions Ltd., SBG SMIT, CHINT Group.

The rising demand for hyperscale data centers necessitates huge amounts of electricity. This mandates installing power transformers at multiple points in the distribution chain, thereby driving their market growth.

- In September 2025, Hitachi Energy announced a USD 1 billion investment for the expansion of critical U.S. power grid infrastructure, including transformers and high-voltage equipment. The investment includes approximately USD 457 million for a new large power transformer facility in South Boston, Virginia. The move is targeted at addressing surging electricity demand driven by AI data centers and broader grid modernization needs.

Key Market Highlights:

- The power transformer market size was recorded at USD 36.24 billion in 2025.

- The market is projected to grow at a CAGR of 6.5% from 2026 to 2033.

- Asia Pacific held a share of 46.10 % in 2025, valued at USD 16.71 billion.

- The large power transformer segment garnered USD 15.80 billion in revenue in 2025.

- The oil-cooled segment is expected to reach USD 52.10 billion by 2033.

- The three-phase segment captures the largest share of 83.30%, estimated at USD 30.19 billion in 2025.

- Middle East and Africa is anticipated to grow at a CAGR of 6.66% over the forecast period.

The rapid expansion of AI Compute infrastructure is transforming global energy demand. The expansion of hyperscale AI data centers to support large language models, autonomous systems, and high-performance computing (HPC) is leading to the surge in electricity consumption. This, in turn, requires the installation of power transformers which handle grid interconnection, voltage regulation and load balancing, thereby increasing their widespread applicability across data center power systems.

According to International Energy Agency (IEA), China and the U.S. are estimated as the most significant regions for data center electricity consumption, accounting for nearly 80% of global growth by 2030. The consumption is anticipated to increase by around 240 TWh (up 130%) in the U.S., compared to the 2024 level. In China, it increases by around 175 TWH (up 170%) for China and 45 TWh (up 70%) for Europe.

- In April 2026, Enphase Energy, Inc. announced the development of its IQ Solid-State Transformer (IQ SST) which is a next-generation distributed power platform designed specifically for AI data centers. The product achieves up to 98.5% efficiency and 99.999% availability through built-in redundancy. This replaces traditional centralized power conversion with a modular “supercluster” design, where each 1.25 MW rack integrates hundreds of semiconductor-based power modules working together to deliver highly efficient energy distribution.

Fluctuations in raw material availability and supply chain disruptions negatively impact the power transformer market by creating an inconsistent supply base. Rising geopolitical tensions, trade tariffs (One Big Beautiful Bill (OBBBA) in the U.S.), and material shortages affect export dynamics, leading to increased production costs for transformer manufacturers.

Additionally, the shortage grain-oriented electrical steel (GOES) which represents 20% of the transformer cost, followed by rising lead times is leading to a supply chain crisis in the U.S. power sector.

For instance, the production capability of GOES limited only to Cleveland Cliffs (U.S.) constrains supply flexibility and impacts transformer production timelines amid growing demand from grid modernization and electrification initiatives. This is expanding average lead times for power transformers and specialized units up to 60 months for North America and Europe and 12 months for Asia Pacific causing a significant backlog of power transformer orders. This further contributes to higher project expenses and hinders market development.

To address the challenge, stakeholders are transitioning towards amorphous core transformers which use non-crystalline metal alloys, resulting in up to 70–80% reduction in no-load losses, and lower carbon footprint.

- In February 2026, Proterial, Ltd. announced the establishment of a new Metglas amorphous metal material production facility in Andhra Pradesh (India), to cater rising demand for energy-efficient transformer components. The plant with an initial production capacity of 30,000 tons per year is scheduled to begin operations in October 2026.

- In August 2025, Klöckner & Co is expanded its electrical steel processing capacity in the U.S. to address rising demand of cold-rolled grain-oriented (CRGO) electrical steel for transformer production and modernization of the aging U.S. power grid. The company established a new production and service center that will increase processing of cold-rolled grain-oriented (CRGO) electrical steel, including slitting and transformer core manufacturing.

The adoption of digitalization and cybersecurity measures in power systems is emerging as a notable trend in the market. The demand for smart and digitally enabled power transformers featuring real-time monitoring, remote diagnostics, and secure communication within modern grid architectures is transforming the market.

Integration of power transformers into digital substations and connected control environments is viewed as data-rich components within broader cyber-physical systems. Cyberattacks on the grid impact power transformers causing incorrect readings, operational disruptions, equipment damage, or large-scale power outages. The malfunction results in forced constant turning on/off which creates an artificial demand for power. This causes the power transformers to trip, leading to blackouts.

To mitigate these operational disruptions, power transformer units are installed with sensors, condition monitoring systems, and communication interfaces. These interfaces enable predictive maintenance, improve operational efficiency and robust cybersecurity providing defense against unauthorized access, data manipulation, and communication-based attacks.

The energy infrastructure of Poland witnessed a failed cyberattack targeted in January 2026 which disrupted communication links between renewable energy installations and power distribution operators.

- In April 2026, Hitachi Energy invested USD 10 million to establish a Power Electronics Center of Competence in Cary, North Carolina (U.S.). The center is developed as a global hub for cybersecurity and advanced grid technologies and large power transformer development.

- In February 2023, Hitachi Energy launched its next-generation TXpert Hub to advance the digitalization of transformers, enable predictive maintenance and smart asset management. The solution collects, aggregates, and analyzes real-time data from digital sensors to improve monitoring, enhance performance, and strengthen cybersecurity.

|

Segmentation

|

Details

|

|

By Type

|

Small Power Transformers (10 MVA-30 MVA), Medium Power Transformers (30 MVA - 100 MVA), Large Power Transformers (Above 100 MVA)

|

|

By Cooling

|

Oil-Cooled, Air-Cooled

|

|

By Phase

|

Single-Phase, Three-Phase

|

|

By End Use

|

Utilities, Industrial, Data Centers

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Type (Small Power Transformers (10 MVA-30 MVA), Medium Power Transformers (30 MVA - 100 MVA), Large Power Transformers (Above 100 MVA)). The Large Power Transformers segment accounted for majority market share of 43.60% in 2025 with a valuation of USD 15.80 billion. The segment is expected to register a CAGR of 6.67% from 2026 to 2033. The expansion of data centers, industrial manufacturing sites, electric vehicles and renewable energy projects, combined with grid modernization, are driving demand for large power transformers

- By Cooling (Oil-Cooled, Air-Cooled). The oil-cooled segment was valued at USD 31.64 billion in 2025 and is anticipated to register a CAGR of 6.50% over the forecast period. The ability of oil-cooled power transformers to provide superior thermal management, exceptional dielectric strength, and long-term durability drives the market.

- By Phase (Single-Phase, Three-Phase). The three-phase segment accounted for the highest share of 83.30%, which was valued at USD 30.19 billion in 2025. The usage of three phase electricity for handling industrial loads and long-distance electricity transmission contributes towards the high share of three-phase transformers.

- By End Use (Utilities, Industrial, Data Centers). The utilities segment accounted for the highest share of 67.30%, which was valued at USD 24.39 billion in 2025. The rising electricity consumption due to developing industrial ecosystem, aging grid infrastructure, rapid transportation electrification, and a massive surge in large-load commercial operations, is driving the demand for power transformers.

What Is The Market Scenario In Asia Pacific And Middle East?

Based on region, the global market has been segmented into North America, Europe, Asia Pacific, Middle East and Africa, and South America.

Asia Pacific captures the highest market share of 46.10% in 2025. The high share is attributed to the rapid industrialization and an increased focus on clean energy initiatives. China and South East Asian countries act as major drivers for this growth due to their fast-growing industrial landscape and large populations, which creates high demand for electricity to support their vast grid infrastructures.

For instance, China laid provisions to strengthen its position as the global leader in renewable energy, accounting for 60% of the global capacity expansion by 2030, according to International Energy Agency (IEA). The country has doubled its utility-scale solar and wind power capacity as per government target of 2030 target of 1,200 gigawatts (GW), driving the demand for power transformers in the region.

Additionally, the rising demand from Europe and the U.S. for Chinese manufactured power transformers further drives the market expansion. The demand is attributable to the upgradation of aging power grids, increasing clean energy power generation, and expansion of computing infrastructure, including data centers.

- In March 2026, GE Vernova announced a USD 200 million investment for a large power transformer manufacturing facility in Hai Phong, Vietnam. The expansion is aimed at catering rising global electrification demand, strengthen supply chain resilience, and improve project delivery timelines for power transformers.

- In February 2026, Siemens AG approved an investment of USD 226.33 million for establishing a new 30,000 MVA power transformer factory. The plant is poised to be operational between 2030 and 2032 and will address the rising global and domestic demand for large power transformers.

The Middle East power transformer market is anticipated to grow at the fastest CAGR of 6.66% reaching USD 6.48 billion by 2033. The rise in renewable capacity additions (solar and wind) and smart city developments across the UAE and Saudi Arabia, with projects like Masdar City, NEOM, Red Sea project and, Sultan Haitham City, drive the demand for clean energy, and environmentally responsible urban planning. This fuels the demand for power transformers capable of handling varying load demands.

The surge in the data center industry, driven by digital transformation, widespread adoption of cloud services, and strategic investments in artificial intelligence (AI) further increases the demand for power transformers in the region.

- In April 2025, Saudi Power Transformers Company (SPTC), a subsidiary of Saudi-based Electrical Industries Company signed a getting a contract with Tecnicas Reunidas Saudia for Services and Contracting Company to supply transformers for a major project. The contract is valued at USD 34.3 million for supply of Extra High Voltage (EHV) and High Voltage (HV) transformers and reactors with a duration of 84 months.

Regulatory Frameworks

- In Europe, the Power transformers are regulated under the EU Ecodesign framework, primarily through Commission Regulation (EU) 548/2014 and its amendment (EU) 2019/1783, which establish minimum energy efficiency requirements for transformers used in 50 Hz transmission and distribution networks. The regulations are targeted at reducing lifecycle energy losses by mandating higher efficiency standards for units above 1 KVA and further estimated to deliver substantial system-wide benefits, including annual electricity savings of around 17 TWh by 2030.

- The Institute of Electrical and Electronics Engineers (IEEE) regulation applicable globally through the IEEE C57.12.10-2017 outlines requirements for liquid-immersed power transformers and autotransformers. It provides guidelines for performance, safety, interchangeability, and key electrical, mechanical, and dimensional specifications for both 50 Hz and 60 Hz systems. The standard is applicable to transformers rated 833 kVA and above for single-phase and 750 kVA and above for three-phase applications, typically used in substations for step-up or step-down functions.

Competitive Landscape

Key players operating in the power transformer market, such as Hitachi Energy, ABB, Siemens Energy, Schneider Electric, Fuji Electric and others, are strengthening innovation and efficiency through strategic collaborations and acquisitions. Market players are entering strategic collaborations and acquisitions to expand their portfolio, capture a wider market share and address the high lead timed for power transformers.

- In February 2026, Hammond Power Solutions Inc. (HPS), entered into a definitive agreement to acquire AEG Power Solutions for ~USD 261.97 Million. The acquisition is positioned as a strategic move for HPS to expand its product portfolio, combining transformer and power magnetics capabilities with power electronics expertise of AEG.

- In January 2026, RESA power acquired 3MD Power Services which is a Virginia-based company dealing in high-voltage transformer testing, repair, and maintenance. The acquisition is aimed at expanding power transformer services portfolio of RESA by adding and increasing the number of specialized rigs it uses to process transformer insulating fluids.

Key Companies In The Power Transformer Market:

- Hitachi Energy Ltd.

- Siemens AG

- General Electric Company

- Schneider Electric

- Mitsubishi Electric Power Products, Inc.

- Toshiba International Corporation

- HD Hyundai

- TBEA Co., Ltd.

- WEG

- Hyosung Heavy Industries

- Fuji Electric Co., Ltd.

- LS Electric Co., Ltd.

- CG Power and Industrial Solutions Ltd.

- SBG SMIT

- CHINT Group

Recent Developments

- In September 2025, Northern Transformer Corporation (NTC) invested USD 206.8 million in a new manufacturing facility Innisfil, Ontario (Canada). The plant will manufacture large power transformers of up to 750 MVA and 500 kV for high-voltage transmission and energy infrastructure projects. The expansion is supported by Invest Ontario and is poised to strengthen its energy supply chain and capacity to meet the growing demand for critical grid components.

- In May 2025, Prolec GE which is a joint venture between Xignux and GE Vernova, announced a USD 140 million investment for expanding its medium power transformer manufacturing capacity in Goldsboro, North Carolina. The project comprises a new 144,000-square-foot vertically integrated facility that will double production output by adding about 200 units annually.

- In February 2024, Siemens Energy announced the expansion of its presence in the U.S. by investing in a new large power transformer (LPT) manufacturing and service facility in Charlotte, North Carolina. The initiative is aimed at addressing the heavy reliance on imported transformers and strengthen the reliability and resilience of the U.S. power grid due to rising electricity demand.