Market Definition

The military drone market consists of products and services associated with unmanned aerial vehicles (UAVs) used in the military sector. The market comprises different types of drones such as fixed wing, rotary blade, and hybrid UAVs used for surveillance, reconnaissance, intelligence, target acquisition, and combat operations. It covers manufacturers, component suppliers, software developers, and service providers supporting defense organizations and government agencies.

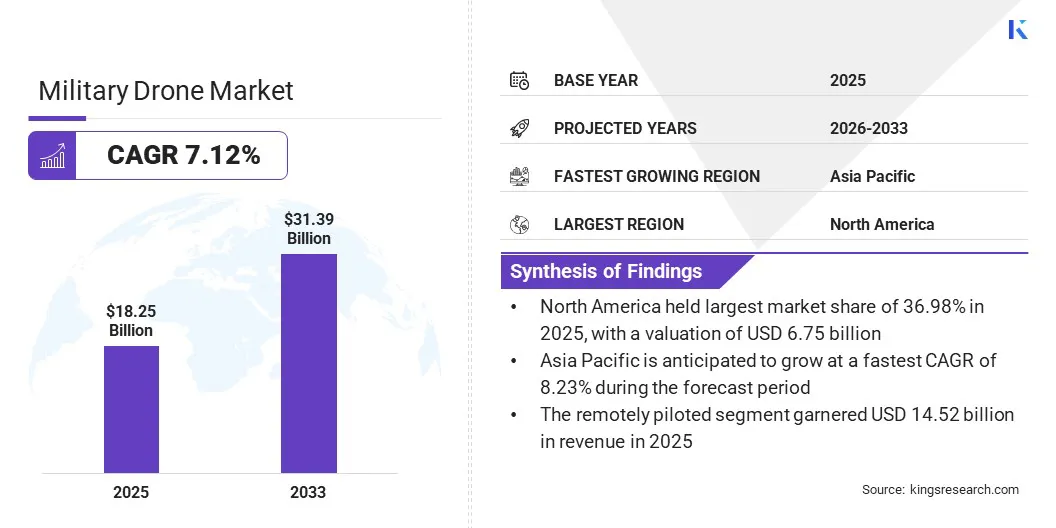

Military Drone Market Overview

The global military drone market size was valued at USD 18.25 billion in 2025 and is projected to grow from USD 19.40 billion in 2026 to USD 31.39 billion by 2033, exhibiting a CAGR of 7.12% during the forecast period. This growth reflects the increasing adoption of unmanned aerial vehicles for defense applications across various regions.

Major companies operating in the global military drone industry are General Atomics, Northrop Grumman, Boeing, AeroVironment, Inc., Anduril Industries, Lockheed Martin Corporation, Shield AI, Skydio, Inc., Kratos, Teledyne FLIR Defense Inc., Israel Aerospace Industries., BAYKAR TECH, Thales, Elbit Systems Ltd., and Airbus.

The market is expanding owing to the increasing demand for advanced surveillance, intelligence, and reconnaissance solutions and ongoing investments in military modernization. Moreover, technological improvements and the use of artificial intelligence are making military drones more versatile and effective, thus contributing to the positive growth of the market.

- In April 2026, Aero Velocity and AC Future Inc. entered into a strategic alliance to create a Mobile Drone Launch Vehicle (MDLV) platform tailored for the U.S. military. The system will enable the mobile and autonomous drone launch and recovery of drones, supporting missions in challenging environments and expanding deployable drone infrastructure for defense and public-sector applications.

Key Market Highlights

- The global military drone market size was USD 18.25 billion in 2025.

- The market is projected to grow at a CAGR of 7.12% from 2026 to 2033.

- North America held a share of 36.98% in 2025, valued at USD 6.75 billion.

- The fixed wing segment garnered USD 10.76 billion in revenue in 2025.

- The remotely piloted segment is expected to reach USD 24.50 billion by 2033.

- The beyond visual line of sight (BVLOS) segment is anticipated to witness the fastest CAGR of 8.05% over the forecast period.

- The intelligence, surveillance, reconnaissance, and targeting (ISRT) segment garnered USD 8.75 billion in revenue in 2025.

- The <150 Kg segment held a share of 47.54% in 2025.

- The short-endurance drones (Up to 6 hours) segment is expected to reach USD 7.70 billion in revenue in 2025.

- The army segment is likely to register USD 15.55 billion by 2033.

- Asia Pacific is anticipated to grow at a CAGR of 8.23% through the projection period.

How Is The Increasing Demand For Intelligence, Surveillance, And Reconnaissance (ISR) Capabilities Fueling Market Expansion?

The increasing need for improved intelligence, surveillance, and reconnaissance (ISR) capabilities is driving market growth. Accurate and timely intelligence is critical for decision-making, threat assessment, and situational awareness in military operations. The use of drone technology with sophisticated sensors, cameras, and data transmission systems can help armed forces perform persistent surveillance over large, inaccessible areas in demanding and hostile environments.

These drones are able to capture high-quality images, track enemy troop movements, and provide up-to-date situational updates without risking human lives. As threats become more sophisticated and militaries look for a tactical advantage, ISR-capable drones are becoming a key part of modern military strategy and investment.

- In April 2026, Arastelle Drone Solutions joined the Red Cat Futures Initiative to integrate modular tethered UAS technology with Red Cat’s drone platforms. The partnership provides extended mission endurance and flexibility for defense and public safety missions in challenging terrains, as it enables persistent ISR and tactical communications through these drones.

How Does Vulnerability To Cyberattacks And Electronic Warfare Hinder The Growth Of The Military Drone Market?

One of the major concerns is its susceptibility to cyber-attacks and electronic warfare. The dependence on sophisticated communication networks, GPS signals, and data links in drone operations increases their exposure to vulnerabilities like drone hacking, signal jamming, and interception by adversaries. Such weaknesses can result in the loss of control, data breaches, or the compromise of sensitive mission intelligence.

To overcome these challenges, companies are investing heavily in cybersecurity solutions, including encrypted communications, anti-jamming technologies, and real-time threat detection systems. By incorporating advanced protection measures and regular security updates, manufacturers aim to safeguard military drones and ensure mission continuity in contested environments.

The integration of artificial intelligence (AI) into military drones is an industry-transforming trend that is changing the defense landscape. AI allows drones to function with increased autonomy, enabling them to navigate complex environments, identify targets, and carry out missions with less human intervention. By utilizing machine learning algorithms and real-time data analysis, military UAVs can adjust to changing battlefield conditions, detect threats, and coordinate actions in drone swarms to enhance effectiveness.

This transition increases operational speed and accuracy while reducing the cognitive burden on operators. Defense firms are continuously developing AI systems to create more intelligent, reliable, and efficient autonomous drones capable of performing effectively across diverse mission scenarios.

- In February 2025, Ondas’ Airobotics unveiled a worldwide demonstration tour for its Iron Drone Raider system. The platform features AI capabilities to autonomously detect, track, and neutralize threats in real time and is designed for defense and security applications, particularly in response to the increasing demand for advanced automated counter-drone solutions.

Military Drone Market Report Snapshot

|

Segmentation

|

Details

|

|

By Type

|

Fixed Wing, Rotary Blade, and Hybrid

|

|

By Operation Mode

|

Remotely Piloted, Partially Autonomous, and Fully Autonomous

|

|

By Range

|

Visual Line of Sight (VLOS), Extended Visual Line of Sight (EVLOS), and Beyond Visual Line of Sight (BVLOS)

|

|

By Application

|

Intelligence, Surveillance, Reconnaissance, and Targeting (ISRT), Combat Operations, Battle Damage Management, Logistics & Transportation, and Others

|

|

By Weight

|

<150 Kg, 150 - 1000 Kg, and >1000 Kg

|

|

By Endurance

|

Short-Endurance Drones (Up to 6 hours), Medium Endurance Drones(6-24 hours), Long Endurance(Over 24 hours)

|

|

By End User

|

Air Force, Army, Navy, and Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Type (Fixed Wing, Rotary Blade, and Hybrid): The fixed wing segment earned USD 10.76 billion in 2025, owing to its superior endurance, higher payload capacity, and suitability for long-range surveillance and reconnaissance missions. Military units are the primary users of fixed-wing drones, as they can effectively cover large operational areas, which makes them the first choice for strategic defense applications.

- By Operation Mode (Remotely Piloted, Partially Autonomous, and Fully Autonomous): The remotely piloted segment held a share of 79.55% in 2025 because of its proven reliability, established operational protocols, and the ability to maintain human control in complex missions. This mode remains the standard for military situations requiring quick decisions and the ability to adapt to dynamic conditions for surveillance and combat.

- By Range (Visual Line of Sight (VLOS), Extended Visual Line of Sight (EVLOS), and Beyond Visual Line of Sight (BVLOS)): The Beyond Visual Line of Sight (BVLOS) segment is projected to reach USD 15.75 billion by 2033, owing to its ability to support long-distance operations, extended surveillance missions, and enhanced operational flexibility. BVLOS drones allow militaries to conduct missions in remote or hostile environments without risking personnel.

- By Application (Intelligence, Surveillance, Reconnaissance, and Targeting (ISRT), Combat Operations, Battle Damage Management, Logistics & Transportation, and Others): The combat operations segment is anticipated to grow at a CAGR of 8.12% through the projection period, driven by the increasing deployment of drones for precision strikes, real-time battlefield support, and tactical missions. UAVs enhance combat effectiveness by providing situational awareness and reducing risks to personnel during high-risk engagements.

- By Weight (<150 Kg, 150 - 1000 Kg, and >1000 Kg): The <150 Kg segment garnered USD 8.68 billion in 2025, mainly due to its versatility, ease of deployment, and suitability for tactical reconnaissance and rapid-response missions. Lightweight drones are favored for their mobility, lower operational costs, and ability to operate in environments where larger UAVs may be impractical.

- By Endurance (Short-Endurance Drones (Up to 6 hours), Medium Endurance Drones (6-24 hours), Long Endurance (Over 24 hours)): The short-endurance drones (Up to 6 hours) segment is projected to reach USD 12.96 billion by 2033, due to their widespread use in tactical operations, rapid deployment capabilities, and suitability for missions requiring agility and quick turnaround. These drones are ideal for short-range surveillance, battlefield support, and emergency response.

- By End User (Air Force, Army, Navy, and Others): The army segment held a share of 45.89% in 2025, fueled by the widespread use of drones for ground surveillance, reconnaissance, and tactical support. These drones are vital to the modern battlefield with the provision of real-time intelligence, target acquisition, and logistics support to ground forces.

What Is The Market Scenario In North America And Asia Pacific?

Based on region, the global military drone market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America military drone market share stood at 36.98% in 2025, with a valuation of USD 6.75 billion. This dominance is reinforced by significant investments in defense procurement programs, rapid adoption of cutting-edge UAV technologies, and strong government support for modernization initiatives. Robust collaboration between defense agencies and private sector innovators accelerates the development of advanced drones tailored to various military missions.

Furthermore, North America’s established infrastructure for research, testing, and deployment enables swift integration of new capabilities into the armed forces. The presence of skilled personnel and an ongoing focus on training and simulation further bolsters the region’s leadership in military drone deployment and operational effectiveness.

- In January 2026, the U.S. Department of Homeland Security established a new office to advance drone and counter-drone technology. A USD 115 million investment will provide systems for securing the America250 and FIFA 2026 events. The office will focus on rapid procurement and deployment to address drone threats.

The Asia-Pacific military drone market is set to grow at a CAGR of 8.23% over the forecast period, owing to increased demand for advanced defense technologies. Growing security concerns, territorial disputes, and the need for enhanced border surveillance are prompting countries to expand their UAV fleets. Several governments are working to develop in-country drone manufacturing capabilities and investing in local R&D to reduce dependence on foreign suppliers.

The regional market further benefits from a rapidly maturing technological landscape and the rise of local manufacturers offering low-cost solutions. Asia Pacific is an attractive market for the drone industry due to the increasing adoption of military capabilities, including the use of drones in reconnaissance, disaster management, and maritime security.

- In December 2025, JSW Defence started construction of a next-generation Unmanned Aerial Systems (UAS) facility in Hyderabad. It partnered with U.S.-based Shield AI. The company invested USD 90 million to manufacture V-BAT military drones to support the Indian Armed Forces and create a global production hub.

Regulatory Frameworks

- In the U.S., the International Traffic in Arms Regulations (ITAR) regulate the export and import of defense articles such as military drones and components. Its purpose is to prevent the unauthorized use of sensitive technologies, which has a direct impact on the military drone market.

- In the EU, the Common Position 2008/944/CFSP governs the export of military technology and equipment. It establishes standards for its member states to assess applications for export licenses and to ensure that exports do not contribute to armed conflict, human rights abuses, or regional instability.

Competitive Landscape

The military drone market is characterized by a dynamic mix of established defense firms and innovative technology companies. Industry leaders leverage advanced research and development to create sophisticated UAV platforms that address evolving military requirements. Meanwhile, specialized providers focus on emerging technologies such as artificial intelligence, autonomy, and miniaturization.

Collaborations, partnerships, and acquisitions are frequent as organizations aim to broaden their technological capabilities and market presence. This environment of intense competition fuels continuous advancements in drone performance, reliability, and adaptability, ensuring that military clients have access to cutting-edge solutions tailored to diverse operational scenarios.

- In October 2025, Red Cat Holdings partnered with AeroVironment to allow FANG FPV drones to be deployed from the P550 UAS platform. The partnership seeks to combine long- and short-range reconnaissance within a single mission, enhance operational flexibility, and demonstrate modular drone interoperability for U.S. defense applications.

Key Companies In The Military Drone Market

- General Atomics

- Northrop Grumman

- Boeing

- AeroVironment, Inc.

- Anduril Industries

- Lockheed Martin Corporation

- Shield AI

- Skydio, Inc.

- Kratos

- Teledyne FLIR Defense Inc.

- Israel Aerospace Industries.

- BAYKAR TECH

- Thales

- Elbit Systems Ltd.

- Airbus

Recent Developments

- In January 2026, the Swedish Government announced over USD 570 million in funding to boost drone and space capabilities for the Swedish Armed Forces. The plan allocates USD 430 million for advanced drone systems such as loitering munitions, reconnaissance drones, and unmanned marine vehicles, and USD 140 million for surveillance satellites.

- In September 2025, Honeywell demonstrated its Stationary and Mobile UAS Reveal and Intercept system to U.S. military operators, showcasing its capability to detect, track, and counter drone swarms. The mobile system protected critical infrastructure and assets, highlighting its advanced sensors, reliability, and rapid integration features.

- In September 2025, the U.S. Army awarded Draganfly Inc. a contract for Flex FPV drone systems. The high-performance drones are designed for rapid deployment, advanced operations, and the Army’s transition to decentralized, agile drone capabilities to enhance force readiness in overseas locations.

- In May 2025, Lyten launched a next-generation drone propulsion initiative using American-made lithium-sulfur batteries. The company has dedicated manufacturing plants in California to make ultra-lightweight, high-endurance batteries for U.S. defense drones, designed to reduce the need to import materials and increase the capabilities of payloads, flight times, and operational ranges.

- In January 2025, L3Harris Technologies introduced a robotic drone detection and defeat capability for the U.S. Army by integrating a counter-UAS system onto the T7 robot. This allows remote detection and neutralization of drones, as well as signal monitoring and decoding for electronic warfare applications.

- In July 2025, the Australian Government fast-tracked procurement of drone and counter-drone technologies for the Defence Force, awarding contracts worth USD 16.9 million to 11 vendors. A total of 120 advanced systems will be fielded, with long-term plans to inject more than USD 10 billion into drone capabilities over the next decade.

- In March 2025, Leonardo and Baykar signed a Memorandum of Understanding to create a joint venture in Italy focused on unmanned aerial systems. The partnership combines Baykar’s drone platforms with Leonardo’s mission systems and aims to target the European unmanned market, which is projected to reach USD 100 billion over ten years.