Market Definition

The fatty amines are nitrogen derivatives of fatty acids, olefins, or alcohols prepared from natural sources such as fats and oils, or from petrochemical raw materials. They are produced by hydrogenation of fatty nitriles, which are generated by the reaction between triglycerides, fatty acids, or fatty esters and ammonia, with the elimination of two molecules of water at high temperature in the presence of dehydrating catalyst.

Fatty amines are widely used in diverse end use industries owing to their applicability as adjuvants in agriculture, surfactants and corrosion inhibitors in manufacturing industries, and as fabric softeners due to their low toxicity and excellent surface activity.

Fatty Amines Market Overview

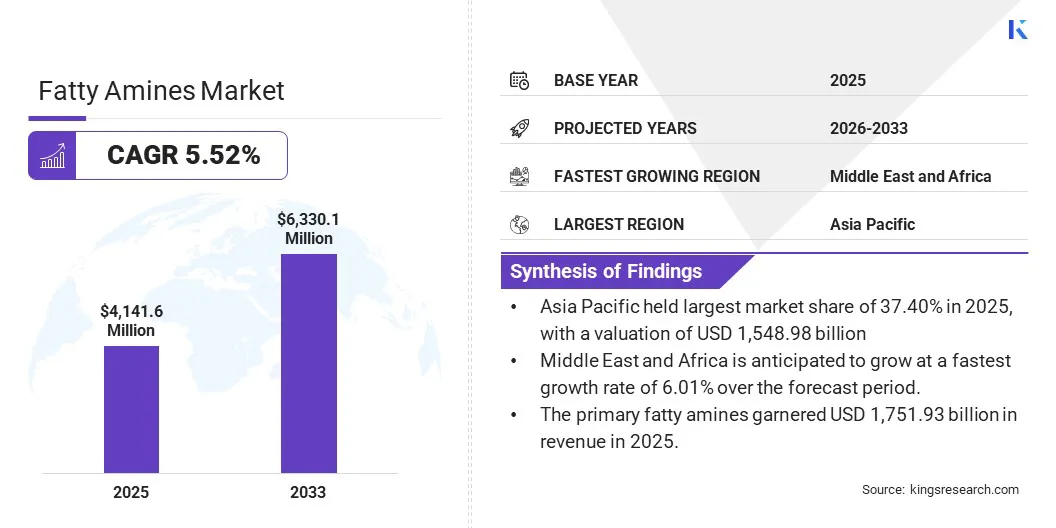

The fatty amines market size was valued at USD 4,141.67 million in 2025 and is projected to grow from USD 4,345.37 million in 2026 to USD 6,330.14 million by 2033, exhibiting a CAGR of 5.52 % over the forecast period. The market is experiencing rapid growth due to diverse applicability of fatty amines across key industries comprising agrochemicals, water treatment, personal care, and oilfields. Their application as potential corrosion inhibition, surfactants, and formulation enhancers to improve industrial performance fuels their adoption.

Major companies operating in the global market are Arkema, Akzo Nobel N.V., Albemarle Corporation, CLARIANT, Eastman Chemical Company, Evonik Industries AG, Global Amines Company Pte. Ltd., Huntsman, and Indo Amines Limited, Ascend Performance Materials, PT. Ecogreen Oleochemicals, Formosa Plastics Corporation, U.S.A., India Glycols Ltd., Kao Corporation, and KLK OLEO.

The applicability of fatty amines as biodegradable, low-toxic, and bio-based surfactants drives market growth. This enables market players to increase production and facility expansion.

- In June 2025, Evonik Industries AG expanded its production operations of specialty amines in Nanjing (China) with a strategic double-digit million-euro investment. The project is targeted at strengthening the production capacity of fatty amines in China and supporting the commercial-scale launch of new specialty amines by 2026.

Key Market Highlights:

- The fatty amines market size was recorded at USD 4,141.67 million in 2025.

- The market is projected to grow at a CAGR of 5.52% from 2026 to 2033.

- Asia Pacific held a share of 37.4% in 2025, valued at USD 1,548.98 million.

- The primary segment garnered USD 1,751.93 million in revenue in 2025.

- The agrochemicals segment is expected to reach USD 1,243.26 million by 2033.

- The Middle East and Africa region is anticipated to grow at a CAGR of 9.20% through the projection period.

How is the increasing agricultural production driving demand for fatty amines?

The application of fatty amines in the production of diverse agrochemical solutions acts as a major driver towards their growth. The potential of fatty amines in enhancing the effectiveness of herbicides, fungicides, and insecticides by enabling targeted delivery and improving plant absorption acts as a major catalyzing factor driving their growth.

Additionally, the cationic properties of fatty amines that enhance adhesion to plant surfaces in addition with improving efficiency and reducing environmental impact, further act as a major driving factor for market growth.

- In March 2025, the Food and Agriculture Organization reported the net agricultural output increment from USD 4.37 trillion in 2023 to USD 4.42 trillion in 2024. The high production rate necessitates the demand for effective agricultural formulations. Thus, highlighting the role of fatty amines in pesticide and herbicide production.

How do environmental regulations negatively impact the growth of the fatty amines market?

Rising concerns over toxicity, biodegradability, and potential bioaccumulation of fatty amines in soil layers and water bodies restrict their usage to specific applications. The imposition of stringent regulations results in increased compliance costs for fatty amine producers, which results in restricted potential and growth avenues for the market.

To address this challenge, market players are aligning strategies with evolving regulatory frameworks such as the REACH or RoHS directive. This drives the shift toward greener chemistry technologies and biodegradable amine-based production.

- In June 2024, Nouryon acquired ISCC PLUS accreditation for green ethylene oxide, ethanolamines, and ethylene amines at its Stenungsund facility in Sweden. The accreditation supports Nouryon's high-performance solutions that reduce product carbon footprints without compromising quality or performance.

How is the use of biodegradable raw materials becoming a major trend in the fatty amines market?

Major players operating in the fatty amines industry are adopting innovative strategies involving the use of biodegradable materials to improve the productivity and efficacy of fatty amines while simultaneously promoting sustainability. The rising shift toward sustainability is compelling manufacturers to incorporate biodegradable raw materials and environmentally friendly manufacturing practices to pose less strain on the environment.

The development of cobalt-based catalytic technologies is enabling the hydrogenative depolymerization of polyesters and biogenic waste to produce high-value amine compounds. The process is utilized for the one-pot production of primary fatty amines from used cooking oil which offers an efficient and sustainable alternative to conventional multi-step industrial synthesis processes.

- In March 2024, Olivia Oleo Pte LTD developed a process to generate fatty amines from distilled coconut fatty acid. The company innovated chemical processes that convert coconut-based fatty acids into fatty amines. This is poised to contribute significantly towards eco-friendly industrial practices, owing to the use of coconuts that are inherently biodegradable in nature.

Fatty Amines Market Report Snapshot

|

Segmentation

|

Details

|

|

By Type

|

Primary, Secondary, Tertiary

|

|

By Application

|

Agrochemicals, Oilfield Chemicals, Personal Care, Chemical Synthesis, Water Treatment, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Type (Primary, Secondary, and Tertiary). The tertiary segment is forecasted to grow at a CAGR of 6.88% over the forecast period. The growth is driven majorly by the use of tertiary fatty amines as corrosion inhibitors, demulsifiers, and lubricity enhancers in the petroleum industry, particularly for refining and fuel additive applications.

- By Application (Agrochemicals, Oilfield Chemicals, Personal Care, Chemical Synthesis, Water Treatment, and Others). The oilfield chemicals segment is projected to grow at a CAGR of 6.76% over the forecast period. The growth is driven by the rising demand for corrosion inhibitors, emulsion stabilizers, and drilling fluid additives across global manufacturing and industrial sectors.

What is the market scenario in North America and Asia Pacific region?

Based on region, the global fatty amines market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Asia Pacific accounts for the dominant market share, approximating 37.40% in 2025. The high share is attributable to the presence of a relatively larger industrial sector, rapid urbanization, and the surge in demand for agrochemicals, personal care, and water treatment facilities. The strong growth in agricultural activity across prominent Asian economies, including China, India, and Southeast Asia, further drives the demand for fatty amines, owing to their widespread consumption as emulsifiers and wetting agents in agrochemical formulations.

Additionally, increasing disposable income, leading to transforming lifestyles, fuels the demand for personal care and cosmetic products across Asian economies. This promotes the demand for fatty amines due to their applicability in personal care and cosmetic products such as conditioners, creams, and lotions for product formulation.

- In September 2022, Global Amines commenced the startup of its new fatty amines production plant in Surabaya, Indonesia. The new plant supplies fatty amines to customers in Southeast Asia and globally, extending the support provided by Global Amines’ existing production facilities in China, Europe, and the Americas.

North America held nearly 26.80% share in the global market. The growth in the region is due to established industrial manufacturing infrastructure, which necessitates chemical formulations including corrosion inhibitors, demulsifiers, friction modifiers, and anti-wear additives in order to safeguard aging assets and optimize high-tech machinery.

Additionally, the strong demand for water treatment solutions across the U.S. and Canada due to stringent environmental regulations regarding the use of specific chemicals in water treatment methodologies further drives their demand.

- In October 2023, the U.S. National Resources Defense Council (NRDC) highlighted the rising water crisis in the U.S., which is attributed to aging infrastructure, industrial pollution, and agricultural contamination. The situation underscores the necessity for effective water treatment technologies, thus driving the demand for fatty amines and allied chemical formulations in the region.

Regulatory Frameworks

- The U.S. Environmental Protection Agency (USEPA) mandates workplace protection measures, controls on industrial and consumer usage, limitations on water release, and recordkeeping for manufacturers and processors using fatty amines.

- In Europe, the REACH (Registration, Evaluation, Authorization and Restriction of Chemicals) Annex XVII sets specific limits for substances in textiles, leather, and polymers such as azo dyes, chromium VI, cadmium, PAHs, phthalates, and PFAS. The regulation requires testing or audits to ensure products meet the established maximum concentration limits.

- In Australia, the National Industrial Chemicals Notification and Assessment Scheme (NICNAS) conducts Tier II human health assessments of several structurally related fatty tertiary amines under the IMAP framework to track low acute toxicity and genotoxicity.

Competitive Landscape

Key players in fatty amines market are undertaking sustainable and renewable feedstock integration to cater to evolving environmental regulations and consumer demands. Companies are investing significantly in R&D to develop biomass-balanced amine chemistries, thereby reducing dependence on fossil-based raw materials and introducing bio-attributed intermediates and amine derivatives through certified supply chains and mass balance approaches.

This enables downstream industries such as personal care, surfactants, and paper chemicals to transition to lower-carbon raw materials without major process modifications, thus supporting broader decarbonization goals across the chemical industry.

- In September 2025, BASF delivered the first biomass-balanced 3-(dimethylamino)propylamine (DMAPA) in the Asia Pacific region to Galaxy Surfactants. The company used certified renewable feedstocks and renewable electricity in production with the target of reducing CO₂ emissions and aligning with the ESG and sustainability goals of Galaxy Surfactants.

- In February 2024, Kemira announced the launch of ISCC PLUS certified biomass-balanced wet strength resins and polyamines for the paper industry. The products contain 50% renewable carbon through the mass balance approach and are produced at the Estella plant. The initiative signals a growing shift toward renewable and sustainable amine-based chemicals, which are poised to influence future demand for bio-based amines and derivatives.

Key Companies In Fatty Amines Market :

- Arkema

- Akzo Nobel N.V.

- Albemarle Corporation

- CLARIANT

- Ascend Performance Materials

- Eastman Chemical Company

- Ecogreen Oleochemicals

- Evonik Industries AG

- Formosa Plastics Corporation, U.S.A.

- Global Amines Company Pte. Ltd.

- Huntsman

- India Glycols Ltd.

- Indo Amines Limited

- Kao Corporation

- KLK OLEO

Recent Developments

- In May 2025, the BASF Intermediates division converted its entire European amines portfolio to 100% renewable electricity. The transition applies to amines produced at the Ludwigshafen, Germany, and Antwerp, Belgium sites. The initiative is anticipated to reduce annual CO2 equivalent emissions by approximately 188,000 tons compared to 2020, representing an average product carbon footprint reduction of about 8%.

- In August 2025, Kao Corporation opened a new tertiary amine production plant in Pasadena, Texas, with an annual production capacity of 20,000 tons. The facility aims to strengthen supply stability for the U.S. market, which is expected to grow in the mid- to long term, while improving supply chain efficiency and reducing transportation-related CO₂ emissions.