Market Definition

The eVTOL aircraft market includes manufacturing and commercialization of electrically powered aircraft capable of vertical take-off, landing, and efficient low-altitude flight. The market analyzes emerging growth scenarios of eVTOLs in applications across urban air mobility (UAM), passenger transportation, cargo logistics, emergency medical services, and defense operations. It also includes the analysis of the charging infrastructure ecosystem, vertiports, air traffic management solutions, and commercial and regulatory developments.

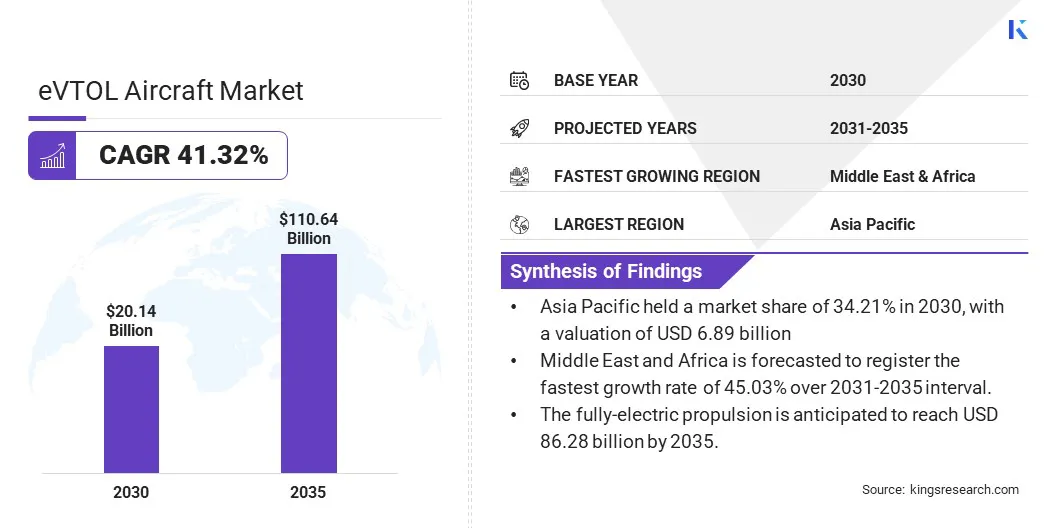

eVTOL Aircraft Market Overview

The global eVTOL aircraft market is forecasted to reach USD 20.14 billion in 2030 and a further USD 110.64 billion by 2035, registering a CAGR of 41.32% over the forecast period (2031 to 2035). The market is undergoing a transformative shift that is redefining urban mobility and public transportation. Market players are emphasizing the development and inclusion of faster, efficient, and sustainable aerial transportation alternatives into the mainstream mode of transportation. Major companies operating in the global eVTOL market, including Volocopter GmbH, Lilium, Joby Aero, Inc., Archer Aviation, Wisk Aero, Beta Technologies, and others, are entering strategic partnerships with technology providers and investment companies to expand market reach. Rising transportation congestion in metropolitan cities across the globe and increasing demand for faster and efficient transportation solutions are enabling transformation across industrial and aviation regulations across regions.

- In December 2025, Vertical Aerospace completed its third and final full-scale VX4 prototype, thus doubling its flight testing capacity to accelerate aircraft development and certification. The second VX4 prototype conducted multiple test flights after receiving a UK Civil Aviation Authority (CAA) permit to fly.

Key Market Highlights:

- The eVTOL aircraft market size is estimated at USD 20.14 billion in 2030.

- The market is projected to grow at a CAGR of 41.32% from 2031 to 2035.

- Asia Pacific is anticipated to hold a 34.21% share in 2030 with a valuation of USD 6.89 billion.

- The passenger eVTOL segment is forecasted to capture USD 15.75 billion in revenue in 2030.

- The fully electric propulsion is anticipated to reach USD 86.28 billion by 2035.

- The up to 200 km range is poised to capture the largest share of 81.31% and is estimated at USD 16.38 billion in 2030.

- The piloted mode of operation is forecasted to reach USD 94.12 billion in 2035.

- The 1,001–2,000 kg Maximum Take-Off Weight (MTOW) segment is poised to register the highest share of 57.45% in 2030.

- The air taxi / air metro / air shuttle application is estimated to capture USD 65.21 billion in 2035, registering a CAGR of 43.83%.

- The eVTOL aircraft market forecast for the Middle East and Africa is anticipated at a CAGR of 45.03%.

How is the rising urban congestion poised to fuel the growth of the eVTOL aircraft market across the globe?

eVTOL aircraft offer significant advantages compared to conventional transport, as these are purpose-built to carry passengers. They are operated within regulated airspace under conventional aviation safety standards. The lower noise levels, reduced operating costs, and zero direct in-flight emissions are anticipated to contribute towards their market adoption over the forecast interval. Unlike unmanned drones or cargo-focused platforms, eVTOL design, certification, and operational concepts are fundamentally centered on the safe, reliable transport of passengers, particularly in dense urban and suburban environments. Their high demand is further favorable due to their on-demand, point-to-point air mobility as urban air taxis, airport-city connections, and short-range regional mobility. This, in turn, empowers users to bypass ground traffic congestion and reduce travel times within metropolitan areas, thereby boosting adoption.

- In March 2026, Joby Aero, Inc. joined the White House-backed Electric Vertical Takeoff and Landing (eVTOL) Integration Pilot Program (eIPP). The program enables Joby to commence early air taxi operations in 2026 in Arizona, Florida, Idaho, New Jersey, New York, North Carolina, Oklahoma, Oregon, Texas and Utah.

How do battery limitations and charging considerations restrain the growth of the global eVTOL aircraft market?

eVTOLs require fast charging to maximize vehicle uptime and revenue generation. Hence, battery limitations to handle high power inputs without performance degradation restrain market growth. eVTOLs experience peak power output during takeoff and landing, which necessitates propulsion systems and batteries to handle the demand without overheating or suffering rapid wear. The short cruising times lead to frequent and intense power and thermal cycles, which require efficient power systems that deliver the peak power and dissipate heat effectively in parallel.

Challenges associated with lithium-ion batteries, including charging speed, thermal management, and the absence of charging stations in urban areas, further hinder adoption. This infrastructure challenge requires investment in grid upgrades and renewable energy integration to support sustainable and reliable charging. Additionally, high ambient temperatures across regions accelerate battery degradation and strain on propulsion systems during takeoff and landing. This results in engine operation at higher RPMs to generate the required lift, further stressing components, and potentially shortening their lifespan. To address the challenge, market players are exploring battery technologies offering higher energy densities and better thermal stability.

- In November 2024, EHang Holdings Limited, in collaboration with the Low-Altitude Economy Battery Research Institute of the Hefei International Advanced Technology Application Promotion Center and Shenzhen Inx Energy Technology Co., Ltd., launched a high-energy solid-state battery technology, EH216-S, which completed a continuous 48-minute and 10-second flight and improved flight endurance by 60%-90%.

How is the adoption of eVTOL aircraft in services, apart from air mobility, poised to create new growth avenues in the future?

The adoption of eVTOL aircraft in medical emergency services, disaster response, tourism and sightseeing or cargo, and logistics is anticipated to create novel growth avenues for market. eVTOL aircraft are positioned to enhance emergency medical services (EMS) and mission-critical applications by enabling the deployment of paramedic-pilots to incident locations, particularly in areas where ground response times are prolonged. Their application in emergency services to complement existing ambulance and air ambulance networks further creates new opportunities for the market. The integration of eVTOL technology is expected to improve response efficiency, particularly in congested urban areas, remote regions, and disaster-affected locations, thus supporting the broader adoption of advanced air mobility solutions within public safety operations.

Additionally, the high operating cost, noise restrictions, and environmental concerns of traditional helicopter tours create potential growth avenues for the market. The silent panoramic flights above coastal regions, mountain ranges, urban skylines, or cultural landmarks and reduced noise profile enable sightseeing flights in areas where alternative aerial applications witness community opposition.

- In March 2026, the U.S. Department of Transportation (USDOT) and the Federal Aviation Administration (FAA) selected eight pilot projects under the Advanced Air Mobility and eVTOL Integration Pilot Program (eIPP). The initiative is planned to accelerate the safe integration of next-generation aircraft into the U.S. national airspace. The initiative encompasses applications including urban air mobility, regional passenger transportation, cargo logistics, autonomous flight, offshore operations, and emergency medical services across 26 states.

- In June 2023, ADAC Luftrettung and Volocopter GmbH entered into a partnership to develop eVTOL aircraft for emergency medical services. The collaboration includes the purchase of two VoloCity aircraft for research operations in Germany, with plans to potentially acquire 150 additional eVTOLs for future rescue missions.

eVTOL Aircraft Market Report Snapshot

|

Segmentation

|

Details

|

|

By Platform Type

|

Passenger eVTOL, Cargo eVTOL, Dual-use / Special mission eVTOL

|

|

By Propulsion

|

Fully electric, Hybrid electric

|

|

By Range

|

Up to 200 km, Above 200 km

|

|

By Mode of Operation

|

Piloted, Autonomous

|

|

By Maximum Take-Off Weight (MTOW)

|

Below 250 kg, 250–1,000 kg, 1,001–2,000 kg, Above 2,000 kg,

|

|

By Application

|

Air taxi / air metro / air shuttle, Cargo transport / last-mile delivery, Medical / EMS, Defense / surveillance / special mission, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Platform Type (Passenger eVTOL, Cargo eVTOL, Dual-use / Special Mission eVTOL). The passenger eVTOL is forecasted to account for a majority market share of 78.21% in 2030 with a valuation of USD 15.75 billion. The growth is driven by the demand for urban air mobility, air taxi services, and investments in passenger-focused eVTOL commercialization.

- By Propulsion (Fully electric, Hybrid electric). The hybrid electric propulsion is forecasted to register the fastest CAGR of 51.78% over the forecast period. The growth rate is anticipated due to extended flight range, improved operational flexibility, and suitability for fast deployments.

- By Range (Up to 200 km, Above 200 km). The up to 200 km range is poised to capture the largest share of 81.31% and is estimated at USD 16.38 billion in 2030. The large share is anticipated to fulfill the demand for short-distance urban and suburban transportation applications.

- By Maximum Take-Off Weight (MTOW) (Below 250 kg, 250–1,000 kg, 1,001–2,000 kg, Above 2,000 kg). The 1,001–2,000 kg Maximum Take-Off Weight (MTOW) segment is forecasted to register the highest share of 57.45% in 2030. The share growth is attributed to eVTOLs’ ability to carry multiple passengers and balance payload capacity.

- By Application (Air taxi / Air metro / Air shuttle, Cargo transport / Last-Mile Delivery, Medical / EMS, Defense / Surveillance / Special Mission, Others). The air taxi / air metro / air shuttle application is estimated to reach USD 65.21 billion in 2035, registering a CAGR of 43.83%. The high growth rate is estimated due to the rising urban congestion and increasing demand for rapid point-to-point transportation.

What is the market scenario in Asia Pacific and the Middle East?

Based on region, the global eVTOL aircraft market has been segmented into North America, Europe, Asia Pacific, Middle East and Africa, and South America.

Asia Pacific is poised to capture the highest 34.21% market share in 2030. The high share is attributed to the demand for urban air mobility across densely populated megacities with limited ground transportation connectivity. The region is designated as a key hub for the development and commercialization of advanced air mobility (AAM) due to favorable government initiatives, expanding industry partnerships, and increasing investments in eVTOL technologies. Countries including Japan, South Korea, China, Singapore, India, Australia, and New Zealand are advancing air taxi services, regional mobility solutions, and supporting infrastructure such as vertiports and air traffic management systems.

- In January 2026, Vertical Aerospace showcased its next-generation Valo eVTOL aircraft at the Singapore Airshow. The eVTOL offers a redesigned platform with improved aerodynamics, an underfloor battery system, and enhanced propeller architecture with proposed commercial launch in 2028.

The Middle East eVTOL aircraft market is anticipated to grow at the fastest CAGR of 45.03% over the forecast period (2031-2035). The region is likely to gain pace as a strategic hub for advanced air mobility (AAM) due to strong government support, favorable regulatory policies, and significant investments in eVTOL infrastructure and commercialization. Countries such as the UAE and Saudi Arabia are signing strategic partnership deals with leading eVTOL manufacturers, including Archer, Joby, EHang, and Eve Air Mobility, to develop air taxi ecosystems, pilot training programs, maintenance facilities, and vertiport infrastructure. These initiatives are positioning the region as one of the earliest markets for large-scale commercial eVTOL deployment, with significant potential to accelerate urban air mobility adoption.

- In November 2025, Joby Aviation signed a memorandum of understanding with Red Sea Global and The Helicopter Company (THC) to conduct pre-commercial electric air taxi evaluation flights in Saudi Arabia during the first half of 2026.

Regulatory Frameworks

- In the U.S., the Federal Aviation Administration (FAA) frames positions eVTOL in the powered-lift category to operate safely in the National Airspace System (NAS). The advisory rule (AC 21.17-4) issues guide regarding testing, certification, and approval for usage in the national airspace.

- In Europe, the European Union Aviation Safety Agency (EASA) introduced “Innovative Air Mobility” that includes eVTOL and other vertical takeoff and landing aircraft. The rules provide detailed acceptable means of compliance and guidance covering manufacturers, operators, pilot licensing, and aircraft operations. The regulations further update existing EU aviation regulations to include new sections for VTOL operations, energy management, and infrastructure like vertiports.

Competitive Landscape

The eVTOL aircraft market is undergoing transformative evolution driven by development programs across the regions. The market is attracting significant funding, technology, and regulatory engagement to reach commercialization. The industry is expected to undergo consolidation over the next decade owing to high certification costs, strict regulatory requirements, and the demand for large-scale investment in eVTOL development, manufacturing, and infrastructure.

Market players with strong cash positions, strategic partnerships, and clear paths to certification are anticipated to register steady growth in the competitive market. Prime differentiators comprising aircraft design philosophy such as multicopter versus tilt-rotor versus lift-plus-cruise, target market segments from urban air taxi to regional transport to cargo. While go-to-market strategy including owned fleet versus manufacturing for others are positioned to create growth avenues for players.

- In July 2026, Joby Aviation and Toyota formed a joint venture named Joby Toyota Aero Manufacturing Preparation Co. to support the production of Joby’s S4 Series eVTOL aircraft. The JV positions Toyota to hold a 51% majority stake and Joby 49% and is targeted at combining manufacturing expertise of Toyota with electric aviation technology of Joby and accelerate commercial rollout of eVTOL air mobility services.

Key Companies in the Global eVTOL Aircraft Market:

- Airbus

- Archer Aviation

- AutoFlight

- Beta Technologies

- EHang Holdings Limited

- Eve Air Mobility

- Joby Aviation

- Lilium

- SkyDrive

- Supernal

- Textron eAviation

- Vertical Aerospace

- Volocopter GmbH

- Wisk Aero

- XPENG AEROHT

Recent Developments

- In June 2026, Vertical Aerospace signed a long-term supplier agreement with Astronics for power distribution systems for its Valo aircraft. The agreement reduces supply chain and production risks, complementing existing partnerships with major aerospace suppliers.

- In November 2025, Archer Aviation announced its first third-party powertrain deal with Anduril and EDGE Group of UAE to power its Omen autonomous air vehicle.