Market Definition

The edge AI in industrial automation market involves the deployment of artificial intelligence (AI) algorithms on edge devices such as sensors, cameras, and industrial controllers. The approach is aimed at reducing latency and enhancing data privacy to boost manufacturing operations. The technology is used across diverse industrial settings, particularly in remote environments, where edge AI monitors equipment, predicts failures, and triggers maintenance alerts without requiring constant data transfer.

Additionally, it improves the efficiency of industrial systems by filtering data at the source and delivering key insights, leading to a significant reduction in bandwidth usage and system load.

Edge AI in Industrial Automation Market Overview

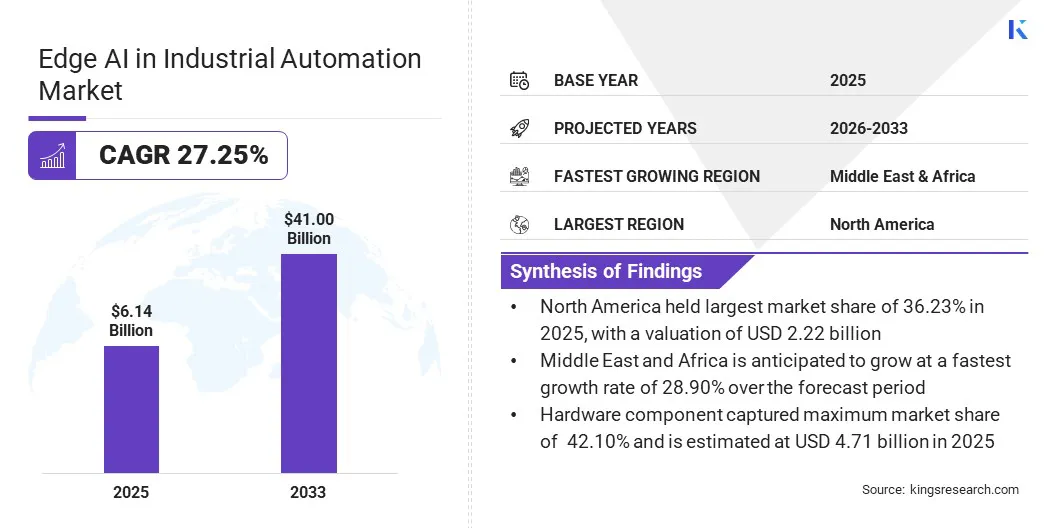

The global edge AI in industrial automation market size was valued at USD 6.14 billion in 2025 and is projected to grow from USD 7.59 billion in 2026 to USD 41.00 billion by 2033, exhibiting a CAGR of 27.25% during the forecast period (2026–2033). This growth is driven by the ability of edge AI systems to analyze data in real-time without needing cloud systems, which results in faster responses, better data privacy, and less use of bandwidth.

Major companies operating in the global edge AI in industrial automation industry are ABB, ARM Limited, CEVA Inc., Honeywell International Inc., Infineon Technologies AG, Mitsubishi Electric Corporation, Nutanix, NVIDIA Corporation, Rockwell Automation, Siemens, SINTRONES Technology Corp., STMicroelectronics, Synaptics Incorporated, TATA ELXSI, and Yokogawa Electric Corporation.

Companies are advancing edge AI in industrial automation by integrating compact AI models and high-performance controllers directly into operational systems. The move is aimed at enabling real-time decision-making, improved security, and enhanced efficiency at the device level.

- In November 2025, Rockwell Automation introduced edge-based generative AI by integrating NVIDIA Nemotron Nano into its FactoryTalk platform. The solution uses a compact AI model optimized for low power and edge deployment, enhancing responsiveness and data security while enabling real-time, on-device intelligence for industrial workflows.

- In October 2025, Rockwell Automation launched the ControlLogix 5590 controller, which is a high-performance industrial controller designed to enhance efficiency, safety, and scalability in edge AI-enabled manufacturing operations. The platform integrates advanced processing, built-in cybersecurity, and unified software tools to streamline workflows and support complex applications.

Key Market Highlights

- The global edge AI in industrial automation market was valued at USD 6.14 billion in 2025.

- The market is projected to grow at a CAGR of 27.25% from 2026 to 2033.

- North America held a share of 36.23% in 2025, valued at USD 2.22 billion.

- The hardware component segment garnered USD 4.71 billion in revenue in 2025.

- The large organization size segment is expected to reach USD 22.18 billion by 2033.

- The cloud-based segment is estimated to generate a revenue of USD 26.36 billion by 2033.

- The chemicals segment is anticipated to grow at a CAGR of 27.37% and is expected to reach USD 4.20 billion by 2033.

- Europe is anticipated to register a CAGR of 28.74% from 2026 to 2033.

How is the rising adoption of AI in manufacturing driving market growth?

The shift of artificial intelligence (AI) from centralized cloud infrastructures to the industrial edge in order to enable real-time decision-making in industrial systems is boosting the adoption of edge AI in industrial automation. The constraints of traditional computing architectures, which are designed for homogeneous workloads, are deemed inadequate for contemporary high-mix production settings, which require flexibility, scalability, and efficiency.

These factors are enabling industrial OEMs to adopt edge AI-integrated automation solutions, which provide inherent AI acceleration, superior performance per watt, scalability across devices, and seamless software transfer from edge to cloud.

Moreover, the attributes of edge AI, including low power consumption, real-time responsiveness, and secure, updatable systems, along with the resolution of critical challenges such as power inefficiency and inflexible hardware-software integration, serve as significant driving factors for the adoption of edge AI in industrial automation.

- In March 2026, Siemens announced advancements in industrial AI at the RXD Summit in Beijing (China). The company introduced 26 new technologies across industrial automation, edge computing, and infrastructure. It further expanded its partnership with Alibaba to deliver cloud-based engineering and simulation solutions across industrial sectors.

- In October 2025, Siemens collaborated with rhobot.ai to launch an advanced edge-native AI solution for manufacturing. The solution, available on the Siemens Xcelerator marketplace, enables real-time optimization and control of industrial processes by integrating directly with factory systems.

How do edge security, data privacy, and complexity impact AI adoption in industrial automation?

Edge AI privacy, security, and integration with legacy systems and data silos act as a crucial factor restraining edge AI adoption in industrial automation. Each edge device expands the attack surface, requiring rigorous hardening, segmentation, and monitoring, which delays deployment. Manufacturing firms cite privacy and compliance as key barriers due to the processing of sensitive operational data.

To address these challenges, market players are embedding security into devices through hardware-based protection, encryption, and secure boot, while simultaneously enabling firmware management, network segmentation, and auditable data flows. Additionally, companies are offering pre-integrated, compliant edge platforms with built-in monitoring and governance to reduce operational technology (OT) security reviews.

- In February 2026, EmbedUR Systems developed the ModelNova platform to provide ready-to-use AI models that simplify application development across industries such as healthcare, transport, and logistics. The company expanded partnerships with global chipmakers Infineon, ST Micron, Synaptics, Arm, Silicon Labs, NXP Semiconductors, and Ceva to strengthen its position in enabling AI to run directly on devices rather than relying on cloud-based systems.

- In December 2024, STMicroelectronics introduced the edge AI microcontroller series STM32N6. The chips are designed to run AI/ML tasks directly on factory machines without relying on large data centers. This enables data processing locally and reduces the need to transfer large amounts of information, improving speed and lowering energy consumption compared to traditional cloud-based AI systems.

How are innovations in industrial AI agents emerging as a key trend in the edge AI in industrial automation market?

Innovations in industrial AI agents are transforming the market. These autonomous systems act like intelligent supervisors on the factory floor and make real-time decisions without constant human input. The ability of these systems to coordinate machines, adjust production parameters, detect quality issues, and optimize workflows dynamically is anticipated to drive their adoption.

Additionally, AI-powered computer vision is transforming manufacturing facilities by enabling real-time, automated inspections that support zero-defect production. They facilitate defect detection, enhanced quality control, and downtime reduction. This, in turn, drives corrective actions that help manufacturers streamline operations and maintain consistent output in automated industrial facilities.

- In May 2025, Siemens introduced AI agents for industrial automation that autonomously execute complex workflows across its Industrial Copilot ecosystem. The agents optimize operations without constant human input and boost productivity by automating industrial processes efficiently.

- In April 2025, Matroid introduced AI-driven computer vision for manufacturing, which enables real-time inspection and zero-defect production. The technology uses deep learning and involves the integration of industrial systems to facilitate immediate corrective actions and continuous process optimization.

Edge AI in Industrial Automation Market Report Snapshot

|

Segmentation

|

Details

|

|

By Component

|

Hardware, Software, Services

|

|

By Organization Size

|

Large Enterprises, Small and Medium Enterprises (SMEs)

|

|

By Deployment Mode

|

Cloud-based, On-Premises

|

|

By End-User Industry

|

Automotive, Aerospace & Defense, Manufacturing, Food & Beverage, Pharmaceutical, Chemicals, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Component (Hardware, Software, and Services). The hardware segment captured the highest market share in 2025 and is estimated to register a growth rate of 26.11% over the forecast period. This growth is mainly attributed to the high dependency of industrial automation on on-site processing devices such as industrial PCs, sensors, GPUs, and edge gateways to drive onboard artificial intelligence systems

- By Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)). The small and medium enterprises (SMEs) are projected to reach USD 18.82 billion by 2033. The high share is due to rapid adoption of edge devices and scalable solutions in small and medium-scale industrial manufacturing sectors to automate production. The lower entry barriers for edge AI deployment enable SMEs to implement real-time automation without heavy cloud infrastructure investments.

- By Deployment Mode (Cloud-based and On-Premises). The cloud-based segment held a share of 52.07% in 2025. The deployment of cloud in edge AI for industrial automation is attributed to its applicability in streamlining supply chains, product lifecycles, and quality control, as well as its ability to enable real-time data access, cost savings, scalability, and smart Industry 4.0 manufacturing.

- By End-User Industry (Automotive, Aerospace & Defense, Manufacturing, Food & Beverage, Pharmaceutical, Chemicals, Others). The automotive segment accounted for a share of 35.20% in 2025 and is projected to reach USD 19.19 billion by 2033. The application of edge AI in shifting intelligence from centralized systems to the automotive production line, thus enabling instant analysis of sensor and production data, acts as a major factor boosting this growth.

What is the market scenario in the North America and Middle East and Africa regions?

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America dominates the market with a share of 36.23% in 2025, due to its advanced digital infrastructure, strong presence of AI and semiconductor manufacturing facilities, and an extensive industrial landscape, which facilitates the adoption of Industry 4.0 technologies. This growth is further supported by rising investments in real-time analytics, IoT, and 5G-enabled smart factories.

Additionally, U.S. manufacturers are deploying edge AI for predictive maintenance and autonomous production lines. Its applicability as on-device processing for faster decisions and improved security acts as a significant propeller towards boosting regional market growth and parallelly supporting edge AI deployments in North American industrial sectors.

- In June 2025, Amazon integrated robotic arms and autonomous mobile robots in its warehouse facilities to improve efficiency, safety, and operational speed. The company introduced AI models such as Proteus, Sequoia and Pegasus that continuously learn from real-world interactions to handle complex tasks and optimize processes.

- In March 2025, General Motors and NVIDIA expanded their collaboration to develop AI-powered solutions for next-generation vehicles, manufacturing, and robotics. The company introduced the use of advanced computing platforms and simulation tools to optimize factory operations and improve production efficiency.

The market in Middle East and Africa is anticipated to register the fastest growth, with a projected CAGR of 28.90% over the forecast period. Rapid industrial digitalization, smart city initiatives, investments in oil & gas automation, and government efforts to modernize infrastructure with AI are leading to the widespread adoption of edge AI in industrial automation. Additionally, the rising demand for real-time monitoring in remote, infrastructure-intensive environments like oil and gas for autonomous inspections and safety monitoring is fostering domestic market expansion.

- In June 2025, AIQ and SLB partnered to advance autonomous energy operations using SLB’s Agora edge AI and IoT solutions. The collaboration focuses on enabling AI-driven automation across energy production environments in Middle East, with further deployment of solutions like RoboWell to accelerate the adoption of AI in upstream and downstream operations.

Regulatory Frameworks

- In the U.S., the National Institute of Standards and Technology (NIST) developed the AI Risk Management Framework (AI RMF) to help enterprises manage risks associated with artificial intelligence. The framework improves the trustworthiness of AI systems throughout their design, development, and deployment.

- In Europe, the EU Artificial Intelligence Act classifies AI systems into risk categories, banning those with unacceptable risks, strictly regulating high-risk applications, and leaving low-risk systems largely unrestricted.

- In China, the Cyberspace Administration of China (CAC) regulates the provision of AI services in the country, thus promoting responsible AI development while also protecting national security, public interests, and user rights.

- In Japan, the framework built on the “Society 5.0” vision promotes a human-centered, data-driven society supported by AI and robotics. The 2025 AI Promotion Act focuses on supporting AI development, transparency, and risk mitigation rather than imposing heavy restrictions across diverse end-use sectors.

Competitive Landscape

The edge AI in industrial automation market is growing significantly due to the rise in investments by industrial enterprises in technologies that enable real-time data processing, predictive maintenance, efficient production methodologies, and autonomous decision-making at the edge. Market players are integrating sensor data, edge computing, and AI to optimize operations, improve system efficiency, and reduce latency across industrial environments.

Market players are introducing technologies that involve the fusion of computer vision, AI, and machine learning, and edge analytics to enhance process automation, quality inspection, and equipment monitoring. The solutions enable on-site intelligence, which facilitates faster response to anomalies, leading to enhanced asset performance and more efficient industrial workflows.

- In March 2025, Qualcomm acquired EdgeImpulse Inc. to expand its leadership in AI capabilities to power AI-enabled products and services across IoT. The acquisition enables Qualcomm to build, deploy, and manage AI models directly on edge devices, enhancing real-time data processing and decision-making, thus driving intelligent industrial and enterprise solutions.

- In December 2024, NVIDIA Corporation launched Jetson Orin Nano Super, a compact and affordable platform designed to run generative AI models on edge devices. The model delivers up to 1.7× improved AI inference performance, making it suitable for robotics and smart vision applications.

Key Companies in The Edge AI in Industrial Automation Market

- ABB

- ARM Limited

- CEVA Inc.

- Honeywell International Inc

- Infineon Technologies AG

- Mitsubishi Electric Corporation

- Nutanix

- NVIDIA Corporation

- Rockwell Automation

- Siemens

- SINTRONES Technology Corp.

- STMicroelectronics

- Synaptics Incorporated

- TATA ELXSI

- Yokogawa Electric Corporation

Recent Developments

- In March 2026, BMW in collaboration with Hexagon Robotics facilitated the deployment of adaptive robotics that can operate independently of centralized computing infrastructure.The company tested the technologies in its Leipzig plant, which represents a full production environment.

- In October 2025, Bosch Rexroth AG expanded its ctrlX AUTOMATION platform with enhanced AI capabilities, increased computing power, and new hardware and software features. The updates include AI-enabled controllers, advanced IPCs, expanded I/O modules, and a software-based Safety PLC that necessity for dedicated hardware.

- In May 2025, Schneider Electric launched its industrial automation innovations at Automate 2025. The products were focused on AI, advanced robotics, and software-defined automation. The company revealed a Generative AI-powered industrial copilot developed in collaboration with Microsoft to enhance productivity and simplify manufacturing operations.