Market Definition

The desktop virtualization market encompasses the technologies and services used to decouple the desktop environment and associated software from the physical client device used to access it. It covers different delivery platforms like hosted virtual desktop, hosted shared desktop, and desktop-as-a-service, along with emerging forms of virtual delivery. The market includes cloud-based and on-premises deployment models, helping both large organizations and small- to medium-sized enterprises.

Desktop Virtualization Market Overview

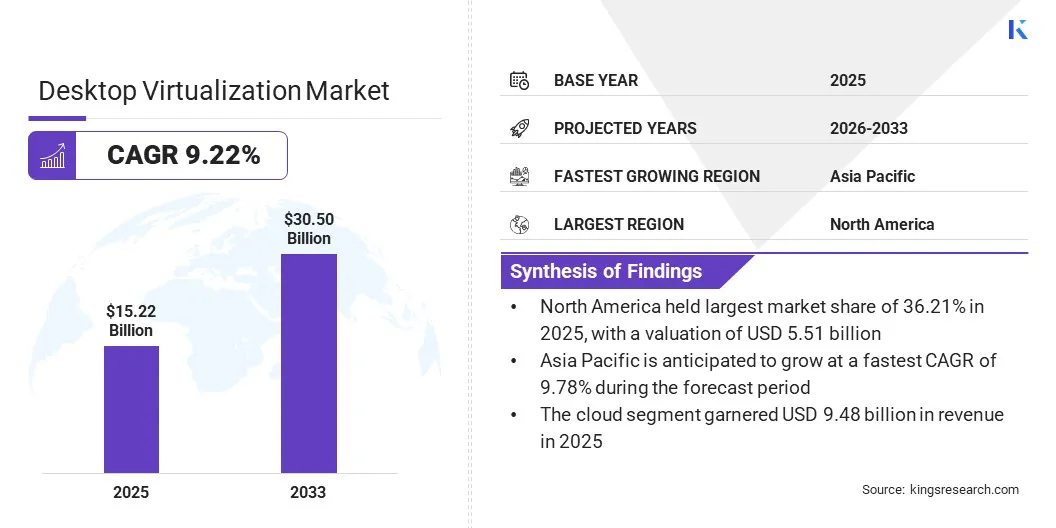

The global desktop virtualization market size was valued at USD 15.22 billion in 2025 and is projected to grow from USD 16.45 billion in 2026 to USD 30.50 billion by 2033, exhibiting a CAGR of 9.22% during the forecast period. This growth is primarily fueled by the rising demand for secure and flexible workspaces as organizations prioritize data protection for distributed workforces.

A significant trend driving this expansion is the strategic shift toward hybrid environments, where businesses combine on-premises infrastructure with cloud-native solutions like Desktop-as-a-Service (DaaS) to achieve optimal performance and cost efficiency.

Major companies operating in the global desktop virtualization industry are Microsoft, Cloud Software Group, Inc., Omnissa, LLC, Amazon Web Services, Inc., Nutanix, Google, Parallels International GmbH, Workspot, Nerdio, V2Cloud Solutions, Inc., Oracle, IBM, Hewlett Packard Enterprise Development LP, Cisco Systems, Inc., and Dizzion.

Organizations are also adopting desktop virtualization to address the emerging needs for high-performance and secure applications. These solutions provide resource-intensive software to remote users while maintaining data integrity. By moving application processing to secure environments, organizations can ensure that sensitive intellectual property is not exposed to vulnerabilities on endpoints.

This approach ensures uniform security policies and enhances productivity across various devices. It also enables a seamless user experience comparable to local hardware performance.

- In March 2024, Citrix, a business unit of Cloud Software Group, Inc., introduced an entirely new platform designed to consolidate application delivery and desktop virtualization infrastructure. The company intends to support enterprises in managing high-performance access to virtual applications and desktops in hybrid and multi-cloud environments more effectively by providing simplified subscription models.

Key Market Highlights

- The global desktop virtualization market size was USD 15.22 billion in 2025.

- The market is projected to grow at a CAGR of 9.22% from 2026 to 2033.

- North America held a share of 36.21% in 2025, valued at USD 5.51 billion.

- The hosted virtual desktop (HVD) segment garnered USD 7.02 billion in revenue in 2025.

- The cloud segment is expected to reach USD 19.76 billion by 2033.

- The large organization segment is expected to reach USD 16.34 billion by 2033.

- The IT & telecom segment is expected to reach USD 7.77 billion by 2033.

- Asia Pacific is anticipated to grow at a CAGR of 9.78% over the forecast period.

How is the rising demand for secure and flexible workspaces fueling market growth?

The desktop virtualization market has been growing at a rapid pace to meet the need for safe and versatile digital workspaces worldwide. Companies use these solutions to provide remote workers with consistent access to corporate applications on any device. This transition reduces the cost of hardware and enhances the operational flexibility within various business sectors.

In addition to remote work, desktop virtualization is applied to centralized data management and endpoint protection. Virtual technologies such as virtual desktop infrastructure (VDI) and desktop-as-a-service (DaaS) enhance efficiency by centralizing IT administration. These systems serve as the core of modern digital environments by allowing businesses to scale resources rapidly and maintain continuity during disruptions.

- In December 2025, Sopra Steria and Nerdio established a strategic partnership to enhance the delivery of desktop virtualization solutions on Microsoft Azure. This partnership combines the managed services of Sopra Steria with the automation technology of Nerdio to simplify the implementation and management of Azure Virtual Desktop and Windows 365. This initiative aims to simplify the management of a virtual work environment via automated scaling and standard configurations to provide safer digital environments.

How are high initial infrastructure costs and network dependencies negatively impacting the growth of the desktop virtualization market?

The major concern in the desktop virtualization market is associated with high initial capital investments and strong reliance on networks. Virtual desktop infrastructure places high financial pressure on small and medium enterprises since it needs powerful central servers and fast storage. These systems are also known to store, process, and manage huge volumes of information online, and this makes performance susceptible to latency and online connectivity problems. Lack of network stability may lead to a bad user experience and productivity loss within the organization.

To address these issues, providers are adopting cloud-based delivery models that minimize the expensive hardware on-premises. They are also introducing more sophisticated compression algorithms and local caching in order to reduce bandwidth usage. With edge computing and hybrid-cloud protocols, companies can achieve a predictable performance of applications even within low-bandwidth settings.

How is the shift toward hybrid environments positively influencing the desktop virtualization market?

One of the trends in the market is the growing use of virtual desktops in hybrid environments. These solutions are intended to be seamlessly integrated with the existing on-premise infrastructure and take advantage of public cloud capabilities. They contrast with traditional, independent, local configurations that do not enable the flexible distribution of resources across various platforms.

Hybrid models are increasingly being utilized in the business world as business needs become more diverse and data security demands grow more complicated. This shift makes hybrid virtualization a common solution for organizations around the world. Such systems enable companies to retain control over sensitive internal data while using the cloud to quickly scale and improve disaster recovery capabilities.

- In November 2025, Microsoft introduced a preview of Azure Virtual Desktop to hybrid environments, allowing Arc-Enabled Servers on premises to be used as session hosts. This release extends cloud-native desktop virtualization to existing infrastructures, such as VMware vSphere, Nutanix AHV, and physical servers, and supports unified management and compliance needs.

Desktop Virtualization Market Report Snapshot

|

Segmentation

|

Details

|

|

By Desktop Delivery Platform

|

Hosted Virtual Desktop (HVD), Hosted Shared Desktop (HSD), Desktop-as-a-Service (DaaS)/Other Forms

|

|

By Deployment

|

Cloud, On-Premises

|

|

By Organization Size

|

Large Organization, SMEs

|

|

By End User

|

IT & Telecom, Financial Service, Government & Public Sector, Healthcare, Retail & E-Commerce, Manufacturing, Education, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Desktop Delivery Platform (Hosted Virtual Desktop (HVD), Hosted Shared Desktop (HSD), and Desktop-as-a-Service (DaaS)/Other Forms): The hosted virtual desktop (HVD) segment earned USD 7.02 billion in 2025, largely attributed to its ability to provide users with a dedicated, high-performance computing environment that mimics a traditional physical PC. This model is specifically adopted by companies that need high levels of isolation for data and high customization for special workloads. The growing demand for steady desktop experiences, where data and user settings are saved across sessions, continues to drive the adoption of hosted virtual desktop solutions in security-conscious industries.

- By Deployment (Cloud and On-Premises): The cloud segment held a share of 62.31% in 2025, primarily due to its inherent scalability, lower upfront capital expenditure, and the ability to support distributed workforces with minimal infrastructure management. Cloud-based desktop virtualization allows IT teams to deliver resources instantly in response to rapid changes in demand, while benefiting from the strong security protocols of major public cloud providers. Additionally, the shift toward subscription models allows organizations to align their IT spend with actual usage, promoting greater financial agility during digital transformation initiatives.

- By Organization Size (Large Organization, SMEs): The large organization segment is projected to reach USD 16.34 billion by 2033, driven by the need to manage a huge number of distributed endpoints while maintaining strict corporate governance and compliance. Large enterprises typically have complex IT ecosystems and the financial capacity required to implement sophisticated virtualization platforms that integrate with existing identity management and security tools. Their focus on centralizing administrative tasks and reducing the total cost of ownership for multiple workstations makes desktop virtualization a priority for maintaining operational consistency globally.

- By End User (IT & Telecom, Financial Service, Government & Public Sector, Healthcare, Retail & E-Commerce, Manufacturing, Education, and Others): The IT & telecom segment is projected to reach USD 7.77 billion by 2033, owing to the continuous focus by major industry players on software development, remote technical support, and the requirement for secure sandbox environments. Companies in this sector use virtual desktops to help developers with secure access to proprietary code and sensitive systems without the risk of data leakage on local hardware. The rapid rollout of 5G technology and the increasing complexity of network management also necessitate flexible, virtualized workspaces that can be accessed reliably from any location.

What is the market scenario in Asia Pacific and North America?

Based on region, the desktop virtualization market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America accounted for a substantial share of 36.21% in 2025, valued at USD 5.51 billion. This dominance is reinforced by the strong presence of major IT and cloud service providers, which continuously support innovation in virtual workspace technologies. The focus on features such as AI-supported usage analytics and advanced automated lifecycle management allows companies in the region to improve and monitor the consumption of resources across all virtual desktops.

- In December 2025, Leostream Corporation released an updated version of its remote desktop access platform to improve and support the scalability of remote working systems. The launch is aimed at streamlining the desktop lifecycle with better API support and higher integrations with cloud providers.

The Asia-Pacific desktop virtualization market is expected to register the fastest CAGR of 9.78% over the forecast period. The growth is driven by large-scale digital transformation initiatives across emerging economies like China and India, where organizations are rapidly modernizing their legacy IT ecosystems.

The increase in mobile-first workforces and the expansion of the regional IT services sector require scalable, low-cost remote access solutions. Additionally, government-led smart city projects and increasing cloud infrastructure investments by local providers are aiding the adoption of virtualized desktops.

Regulatory Frameworks

- In the U.S., the security of virtual desktops in a healthcare environment is governed by the Health Insurance Portability and Accountability Act (HIPAA). It requires rigorous access controls and encryption of data to defend patient information in virtual environments.

- In Europe, the General Data Protection Regulation (GDPR) regulates the processing of personal data on virtualization platforms. It obligates providers to implement data protection measures and ensures that users retain control of their personal data.

- In China, the Personal Information Protection Law (PIPL) governs the storage and transfer of information processed using virtual applications. It imposes strict data localization policies that compel providers to keep sensitive data in the local domestic servers.

- In Japan, the Act on the Protection of Personal Information (APPI) governs the handling of user identity and cross-border data flows in desktop virtualization services. It also makes sure that the virtual service providers observe high levels of transparency and security for users in Japan.

- In India, the Digital Personal Data Protection (DPDP) Act governs the collection and processing of personal data in the virtual workspace. It requires virtualization companies to implement transparent consent processes and develop effective data breach reporting systems.

Competitive Landscape

The major players in the desktop virtualization market are forming alliances to offer customers greater choices. Key software vendors are working with cloud infrastructure pioneers to increase deployment options. These partnerships enable organizations to operate virtual applications on more than one private and public cloud. Meanwhile, platform developers are collaborating with hardware vendors to deliver compatibility with various devices. These alliances assist in easing the delivery of complicated workloads to distant users.

Advanced security features are also built into such collaborations as part of the virtualization layer. These strategic associations make virtual desktops more flexible and manageable. They facilitate the transition to hybrid-work systems and adaptable online workplaces. This kind of cooperation across the industry speeds up the implementation of newer, software-defined infrastructure.

- In May 2025, Omnissa and Nutanix, Inc. established a strategic partnership to support the Horizon platform on Nutanix AHV infrastructure. The partnership is meant to provide organizations with more flexibility in the deployment of virtual desktops and applications in hybrid and multi-cloud environments. This combination of technologies is expected to ease the IT tasks of companies and make the experience of managing distributed workforces more seamless.

Key Companies in The Desktop Virtualization Market

- Microsoft

- Cloud Software Group, Inc.

- Omnissa, LLC

- Amazon Web Services, Inc.

- Nutanix

- Google

- Parallels International GmbH

- Workspot

- Nerdio

- V2Cloud Solutions, Inc.

- Oracle

- IBM

- Hewlett Packard Enterprise Development LP

- Cisco Systems, Inc.

- Dizzion

Recent Developments

- In March 2026, ControlUp launched ControlUp DaaS IQ, a dedicated management solution designed to optimize operations and reduce costs in the Azure Virtual Desktop environment. The solution incorporates smart automation and dynamic resource scaling to eliminate inefficiencies in the cloud and provide IT teams with full visibility of infrastructure health and cost via a centralized control plane.

- In September 2025, Omnissa introduced platform innovations to Workspace ONE and Horizon, including strategic integrations with Nutanix and NVIDIA. These updates focus on autonomous workspaces, increased AI functionality, and integrated management to optimize IT processes and improve the digital employee experience.

- In April 2025, Nerdio launched Nerdio Manager for Enterprise 7.0, an automated management platform designed to streamline the deployment of desktop virtualization technologies. The solution focuses on improving the Windows 365 and Azure Virtual Desktop environments with specialized tools for smoother migration, AI-driven cost optimization, and deeper integration with Microsoft Intune for physical and cloud endpoints.