Market Definition

The ceramic tube market refers to the industrial ecosystem of high-performance cylindrical components. These tubes provide thermal insulation and chemical resistance. The market covers the production and exchange of materials such as alumina and silicon Carbide. Business-to-Business and Business-to-Consumer channels aid these transactions. Major industries, including aerospace, healthcare, and electronics, drive consistent demand.

Ceramic Tube Market Overview

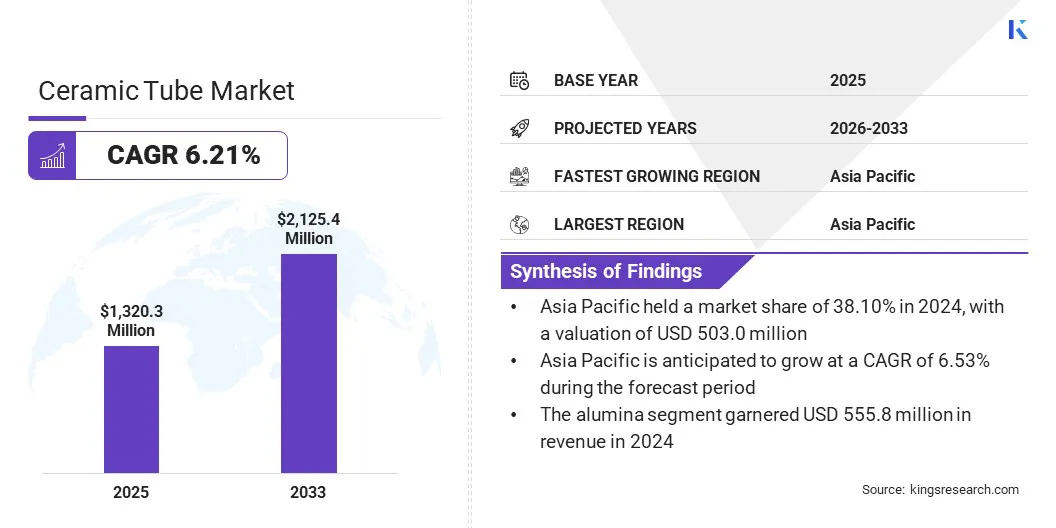

The global ceramic tube market size was valued at USD 1,320.3 million in 2024 and is projected to grow from USD 1,393.8 million in 2025 to USD 2,125.5 million by 2032, exhibiting a CAGR of 6.21% during the forecast period. This growth is fueled by the rising demand for materials that provide high thermal resistance and higher electrical insulation. The market is witnessing advancements in 3D printing technologies, allowing for complex internal geometries in the production of ceramic tubes.

Major companies operating in the global ceramic tube industry are KYOCERA Corporation, Engineering Ceramic Co., Ltd., LSP Industrial Ceramics, Inc., CoorsTek Inc., Kilncera, Corning Incorporated, CeramTec GmbH, Materion Corporation, Active Enterprises, STC Material Solutions, Morgan Technical Ceramics, Mingrui Ceramic, Srishti Ceramics, Carborundum Universal Limited (CUMI), and McDanel Advanced Material Technologies LLC.

Companies are combining precision machining procedures to meet the strict dimensional standards of the industry for ceramic tubes. This process includes diamond tooling and laser machining to achieve close tolerances in semiconductor and medical device manufacturing. These processes enhance the mechanical strength and reliability of the tubes and offer high-quality surfaces. The use of these finishing techniques, therefore, improves the performance of advanced ceramic solutions.

Key Market Highlights

- The global ceramic tube market size was USD 1,320.3 million in 2024.

- The market is projected to grow at a CAGR of 6.21% from 2025 to 2032.

- Asia Pacific held a share of 38.10% in 2024, valued at USD 503.0 million.

- The alumina segment garnered USD 555.8 million in revenue in 2024.

- The business-to-business (B2B) segment is expected to reach USD 1,774.6 million by 2032.

- The aerospace & defense segment is projected to generate a revenue of USD 585.8 million by 2032.

- Europe is anticipated to grow at a CAGR of 6.25% over the forecast period.

How is the rising demand for high thermal resistance and superior electrical insulation driving market expansion?

The ceramic tube market is growing rapidly due to the increasing adoption of materials that maintain structural integrity even under extreme heat and electrical stress. This demand is backed by a shift from conventional materials such as metallic components towards more advanced ceramics, which can withstand temperatures beyond the limits of industrial alloys. The operational lifespan of thermal processing equipment and furnace systems is being extended to minimize downtime and energy loss in high-temperature environments.

Such high-performance materials also provide important dielectric strength and aid in avoiding dielectric interference in sensitive semiconductor equipment. This focus on thermal and electrical stability is an important component of heat management and electronic packaging. These properties allow for a more reliable and low-cost option for operating high-stress, complex circuit industrial systems across the energy and aerospace sectors.

- In 2025, the Journal of Microelectronics and Electronic Packaging published a study on the thermal performance of lead frame packages and ceramics. In the study, aluminum nitride and aluminum oxide were mentioned to be excellent thermal and electrical insulation materials in high-power electronics applications.

How do high production costs negatively impact the ceramic tube market?

One of the major issues in the market is the high cost of production due to expensive raw materials and specialized manufacturing procedures. Advanced ceramics require high-temperature firing and precision machining using diamond tools. These requirements significantly increase energy consumption and instrumentation costs when compared to standard metal parts. These factors create financial constraints for companies seeking cost-effective alternatives to traditional materials.

To solve this issue, manufacturers are adopting technologies such as automated sintering and energy-efficient kilns to reduce the fixed costs. They are also enhancing and streamlining their supply chain operations to receive raw materials in bulk at a low cost. This strategy reduces the production costs of the ceramic tube while ensuring high-quality performance for buyers worldwide.

How are advancements in 3D printing technologies emerging as a key trend in ceramic tube market?

The use of 3D printing for the production of ceramic tubes is increasing. 3D printing enables the creation of ceramic tubes with complex internal geometries and shapes that are highly specific. These systems are different from traditional machining, which often results in higher material waste.

This manufacturing shift addresses the growing need for specialized industrial components across diverse sectors. By adopting additive techniques, the aerospace & defense and healthcare industries have established more efficient, customizable production standards. These advancements allow for precise engineering while significantly reducing the overhead associated with conventional fabrication methods.

Ceramic Tube Market Report Snapshot

|

Segmentation

|

Details

|

|

By Material

|

Alumina, Silicon Carbide, Boron Nitride, Zirconia, Others

|

|

By Distribution Channel

|

Business-to-Business (B2B), Business-to-Consumer (B2C)

|

|

By End-User Vertical

|

Aerospace & Defense, Electronics & Semiconductors, Healthcare, Commercial, Industrial, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Material (Alumina, Silicon Carbide, Boron Nitride, Zirconia, and Others): The alumina segment earned USD 555.8 million in 2024, due to its strong thermal conductivity and higher electrical insulation properties. This material remains a key choice for high-temperature furnace components and heavy-duty industrial machinery. The wide availability of alumina also ensures cost-effectiveness for mass production requirements in sectors such as electronics and automotive.

- By Distribution Channel (Business-to-Business (B2B) and Business-to-Consumer (B2C)): The business-to-business (B2B) segment held a share of 83.20% in 2024, due to the high-volume procurement needs of large-scale manufacturing plants. Industrial buyers typically need customized specifications and bulk shipments that necessitate direct long-term contracts with specialized producers. These arrangements support quality assurance protocols and technical support, which are important for complex projects.

- By End-User Vertical (Aerospace & Defense, Electronics & Semiconductors, Healthcare, Commercial, Industrial, and Others): The aerospace & defense segment is projected to reach USD 585.8 million by 2032, fueled by the increased demand for heat-resistant and lightweight materials in aircraft engines. Ceramic tubes are used to safeguard valuable equipment like communication equipment and sensors that are used in high atmospheric pressure. The development of high-performance insulators is propelled by the need to advance missile defense technologies and satellite components.

What is the market scenario in Asia Pacific and Europe?

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

The Asia-Pacific ceramic tube market accounted for a substantial share of 38.10% in 2024, valued at USD 503.0 million. The reason behind this dominance is the strong manufacturing base and the high rate of special ceramic production plant development in the region. China, Japan, and India are also key centers of large-scale production of ceramics with favorable industrial policies and low-cost production.

The developed electronics and semiconductor fabrication infrastructure in South Korea and Taiwan is also a contributing factor to the demand for high-performance ceramic components. This pooling of production power enables local manufacturers to produce in large quantities while catering to the needs of both the local and international markets.

- In August 2024, Kyocera Corporation started building a new factory in Nagasaki, Japan. The project aims to expand the capacity of the fine ceramic parts and semiconductor packaging solutions. The new plant serves the increasing demand for high-technology electronics, artificial intelligence, and automotive applications.

The market in Europe is expected to register the fastest CAGR of 6.25% over the forecast period. This rapid growth is fueled by the expansion of global companies into the region to meet the rising demand for high-quality ceramic materials. Leading manufacturers are establishing new research and production centers in Germany and France to support the automotive and aerospace sectors. Such investments are focused on the creation of precision-engineered tubes that are in accordance with the stringent European safety and environmental standards.

- In August 2025, Precision Ceramics and MillenniTEK announced a strategic alliance in order to increase the supply of high-quality Boron Carbide in Europe. The cooperation is aimed at the provision of highly machined, high-quality neutron absorbers and shielding elements for high-demand sectors such as the nuclear industry, including natural and 10B-enriched boron carbide.

Regulatory Frameworks

- In the U.S., the main regulatory authority for advanced ceramics is the American Society of Testing and Materials (ASTM), which has the Committee C28 that establishes standard test methodologies for determining the flexural strength and thermal characteristics of ceramic tubes. The ASTM C1161 standard regulates the testing of the mechanical reliability of structural ceramics used in industrial applications.

- In Europe, the Chemical Composition of Ceramic Components the Restriction of Hazardous Substances (RoHS) Directive 2011/65/EU regulates the chemical content of ceramic parts, particularly the amount of heavy metals such as lead and cadmium in electronic ceramic tubes. Directive (EU) 2025/2363 provides updated exemptions for lead in high-voltage ceramic insulators where alternative technical solutions are not yet available.

- In China, the national standard of GB 4806.4-2016 specifies strict requirements for the release of lead and cadmium in ceramic products that are in contact with food or heat. The electrical systems, in which industrial ceramic tubes are employed, are controlled under the China Compulsory Certificate (CCC) system to make sure that the high-voltage transmission of power is safe.

- In Japan, the technical requirements for fine ceramics are defined by the Japanese Industrial Standards (JIS), JIS R 1601 provides test procedures used to determine the mechanical strength of monolithic ceramics. Guidelines are also issued by the Ministry of Economy, Trade and Industry (METI) to make sure that advanced ceramic materials meet high safety standards for use in aerospace and automotive industries.

- In India, IS 15155, which applies to ceramic pouring tubes used in steel casting, ensures thermal shock resistance and structural integrity and is maintained by the Bureau of Indian Standards (BIS). Waste management regulations regarding the disposal of hazardous byproducts of ceramic manufacturing are also implemented by the Ministry of Environment, Forest and Climate Change.

Competitive Landscape

The major participants in the ceramic tube industry are aggressively forming strategic alliances with research centers to advance material science capabilities. Major producers are negotiating Memorandums of Understanding (MOUs) to conduct collective research and development on silicon carbide and other high-performance materials. The goal of these activities is to improve the thermal conductivity and mechanical strength required for high-stress applications.

At the same time, manufacturers are collaborating with academic laboratories to explore the properties of advanced ceramic compositions. This form of cooperation enables companies to share technical risks and enhance the development of specialized products within the aerospace and semiconductor industries. These endeavors also focus on improving thermal conductivity and mechanical strength of high-stress applications.

- In April 2024, Penn State University and Morgan Advanced Materials entered into a memorandum of understanding to launch a strategic research and development initiative. This collaboration is expected to advance silicon carbide technologies and refine carbon-based materials for use in high-efficiency semiconductor production. The partnership supports the creation of the next generation of power electronics while strengthening the supply chain for electric vehicles and renewable energy systems.

Key Companies in The Ceramic Tube Market

- KYOCERA Corporation

- Engineering Ceramic Co., Ltd.

- LSP Industrial Ceramics, Inc.

- CoorsTek Inc.

- Kilncera

- Corning Incorporated

- CeramTec GmbH

- Active Enterprises

- Materion Corporation

- STC Material Solutions

- Morgan Technical Ceramics

- Mingrui Ceramic

- Srishti Ceramics

- Carborundum Universal Limited (CUMI)

- McDanel Advanced Material Technologies LLC

Recent Development

- In January 2025, scientists at Amrita Vishwa Vidyapeetham received a grant from the Department of Science and Technology to create improved ceramic-layered steel tubes. The project focuses on a specialized thermite-based centrifuge process to create high-density ceramic coatings for use in high-temperature and corrosive industrial environments. The project will enhance longevity and increase the service life of key infrastructure in power generation and chemical processing industries.