Market Definition

The automotive remanufacturing market refers to the industrial ecosystem dedicated to the systematic restoration, quality validation, and lifecycle management of vehicle components to their original performance criteria. This market covers the circular processing of critical systems for 2, 3, and 4-wheelers across ICE, BEV, and hybrid propulsion technologies, combining complex supply chains that serve both original equipment manufacturers and the aftermarket.

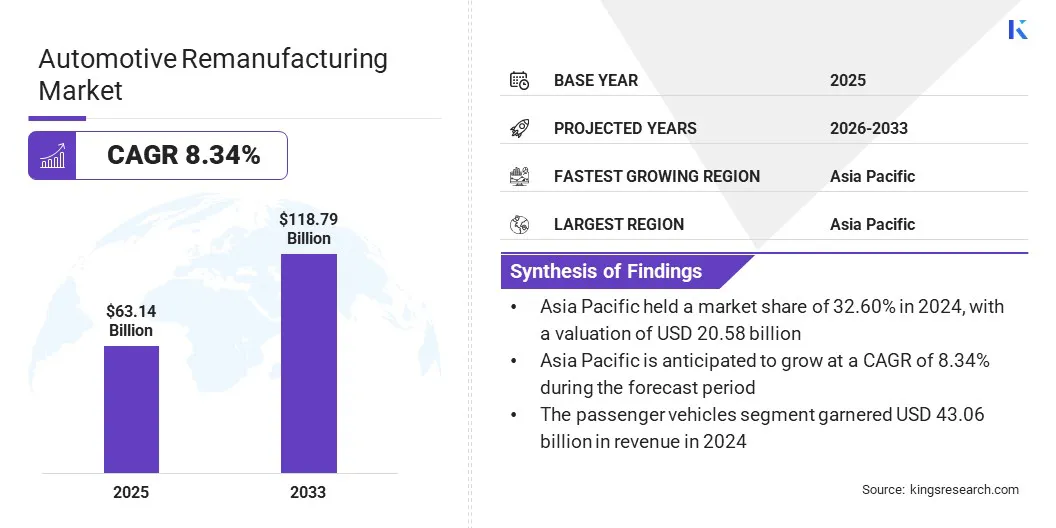

Automotive Remanufacturing Market Overview

The global automotive remanufacturing market size was valued at USD 63.14 billion in 2024 and is projected to grow from USD 67.81 billion in 2025 to USD 118.79 billion by 2032, exhibiting a CAGR of 8.34% during the forecast period. This expansion is primarily driven by the industry-wide shift toward a circular economy model that promotes a reduction in resource depletion and environmental waste.

Major companies operating in the global automotive remanufacturing industry are LKQ Corporation, Robert Bosch GmbH, VALEO, Caterpillar, ZF Friedrichshafen AG, BorgWarner Inc., DENSO, CARDONE Industries, Cummins Inc, Eaton, Schaeffler Technologies AG & Co. KG, Standard Motor Products, Inc., MPA, JASPER Engines & Transmissions, and ATCDT Corp.

Companies are also proactively increasing their engineering expertise to recreate sophisticated power electronics like inverters to their original performance standards. These companies are investing in specialized testing environments and high-end diagnostic software to handle high-end semiconductor recalibration and module restoration.

In contrast to traditional mechanical component restorers, automotive remanufacturing companies are placing a significant emphasis on clean-room production and automated testing to ensure the reliability of electrified powertrains. This interest is expanding as the global fleet is becoming increasingly hybrid and electrically propelled, and remanufactured inverters have become a very common form of sustainable vehicle maintenance.

- In October 2025, Valeo and The Remakers, a division of The Future is NEUTRAL, launched a remanufactured inverter for the Renault ZOE, offering a 30% price cut and a 45% reduction in natural resource consumption. The project is a high-quality, sustainable alternative to new components, based on a rigorous remanufacturing procedure, which can speed up the integration of circular economy solutions in the automotive sector.

Key Market Highlights

- The global automotive remanufacturing market size was USD 63.14 billion in 2024.

- The market is projected to grow at a CAGR of 8.34% from 2025 to 2032.

- Asia-Pacific held a share of 32.60% in 2024, valued at USD 20.58 billion.

- The engine segment garnered USD 14.59 billion in revenue in 2024.

- The 4-wheelers segment is expected to reach USD 84.05 billion by 2032.

- The internal combustion engine (ICE) segment is anticipated to hit USD 42.24 billion by 2032.

- The passenger vehicles segment is likely to generate a revenue of USD 82.59 billion by 2032.

- The original equipment manufacturer (OEM) segment is estimated to reach USD 76.72 billion by 2032.

- Europe is anticipated to grow at a CAGR of 8.60% over the forecast period.

How is the increasing focus on the circular economy driving market expansion?

The market is growing rapidly due to the rising adoption of circular economy models to minimize resource depletion and waste. This solution involves shifting away from conventional linear forms of production in favor of closed systems that emphasize the recovery, restoration, and reuse of valuable vehicle components. The lifecycle of components such as engines and transmissions should be extended as much as possible to minimize energy usage and carbon emissions in comparison to new units.

Such green practices assist manufacturers in addressing stringent environmental policies while also stabilizing the supply chain of essential raw materials. This model is a critical component of resource optimization that allows a more sustainable and low-cost method of maintaining a vehicle and fleet management.

- In February 2026, Toyota Motor Europe announced plans to establish a new Circular Factory in Walbrzych, Poland, with significant investment in infrastructure. The project is dedicated to the processing of end-of-life vehicles to recover raw materials, remake essential parts, and speed up the company’s transition to a carbon-neutral business model.

How are the increasing complexities of advanced vehicle electronics impeding the development of the automotive remanufacturing market?

The biggest challenge in the market is the increasing complexity of modern vehicle electronics and software integration. Because the majority of modern components are equipped with proprietary sensors and control units, accessing encrypted diagnostic data and specialist firmware needed in the restoration process is difficult.

Such integrated systems need highly technical expertise as well as costly machines to re-calibrate and that can act as a hindrance to the traditional remanufacturing plants. This lack of homogeneous access to internal electronic structure makes it complicated to test the levels of performance and safety.

To address these hurdles, manufacturers are investing in advanced diagnostic software and automated testing benches that have the capability to operate with modern vehicle architecture. They are also forging stronger relationships with original equipment manufacturers so that they can access valuable technical specifications and proprietary recovery software.

Standardized certification programs and specialized training for technicians can be used to ensure that such complex electronic assemblies are restored to their original performance levels without causing data loss.

How is the shift toward AI, digital technologies, and automation reshaping the automotive remanufacturing market?

One of the key market trends is the growing popularity of artificial intelligence (AI), digital technologies, and automation used to restore processes. These advanced tools are designed to streamline tasks such as core identification, precision disassembly, and high-fidelity quality inspection. They differ from traditional manual methods, which do not enable rapid, data-driven diagnostic accuracy at a large industrial scale.

Automation and digital twin technology are being increasingly used as components become more complex and electronically integrated, making them widely implemented solutions for modern vehicle systems.

- In September 2025, REMADE and its members confirmed a joint R&D venture to create digital technologies, AI, and robotics to support the development of remanufacturing in the fields of heavy-duty equipment, automotive, and aerospace. The initiative aims to enhance material recovery through the application of automated design, inspection, and restoration tools.

Automotive Remanufacturing Market Report Snapshot

|

Segmentation

|

Details

|

|

By Component

|

Engine, Transmission, Brake System, Electrical & Electronic Components, Chassis & Suspension, Others

|

|

By Vehicle Configuration

|

4-Wheelers, 2-Wheelers, 3-Wheelers

|

|

By Propulsion

|

Internal Combustion Engine (ICE), Battery Electric Vehicles (BEVs), Hybrid Vehicles

|

|

By Vehicle Type

|

Passenger Vehicles, Commercial Vehicles

|

|

By End User

|

Original Equipment Manufacturer (OEM), Aftermarket

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Component (Engine, Transmission, Brake System, Electrical & Electronic Components, Chassis & Suspension, and Others): The engine segment earned USD 14.59 billion in 2024 because of the high prices of new power units. It is growing in popularity due to the rising demand for factory-certified powertrain restoration. These processes provide performance parity with original equipment, and lead times are significantly reduced for aging vehicle fleets.

- By Vehicle Configuration (4-Wheelers, 2-Wheelers, and 3-Wheelers): The 4-Wheelers segment held a share of 72.50% in 2024, mainly due to the significant volume of passenger cars and light commercial vehicles. These units need complicated component renewals to prolong their operational lifespan. Another factor supporting segmental growth is the necessity to meet strict safety standards and adhere to stricter emission regulations.

- By Propulsion (Internal Combustion Engine (ICE), Battery Electric Vehicles (BEVs), and Hybrid Vehicles): The internal combustion engine (ICE) segment is projected to reach USD 42.24 billion by 2032, fueled by the large number of active vehicles globally that rely on traditional powertrains. Another factor that has helped the segment is the continued availability of high-value cores for engine and fuel system restoration. This is especially applicable in developing economies, where ICE vehicles remain the primary mode of transportation.

- By Vehicle Type (Passenger Vehicles and Commercial Vehicles): The passenger vehicles segment is projected to reach USD 82.59 billion by 2032, owing to rising consumer awareness regarding the economic benefits of remanufactured parts. High-quality components have become more accessible through authorized dealership networks. Furthermore, independent service providers and specialized digital aftermarket platforms have significantly expanded the reach of these restored products.

- By End User (Original Equipment Manufacturer (OEM) and Aftermarket): The original equipment manufacturer (OEM) segment is projected to reach USD 76.72 billion by 2032, propelled by intensified investments by major automakers in closed-loop production systems. Many companies are now formally integrating remanufacturing into official warranty and service programs. These initiatives allow companies to meet global circular economy targets while enhancing long-term customer loyalty.

What is the market scenario in Asia Pacific and Europe?

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

The Asia-Pacific automotive remanufacturing market accounted for a substantial share of 32.60% in 2024, valued at USD 20.58 billion. This dominance is due to the region's strong manufacturing base for the automotive industry, which provides a consistent supply of vehicle components for remanufacturing.

Countries such as China, India, and Japan have a massive active vehicle fleet that creates high demand for cost-effective replacement parts. Furthermore, the region benefits from expanding industrial infrastructure and rising consumer interest in affordable vehicle maintenance, which supports the large-scale expansion of the remanufacturing sector.

The market in Europe is expected to register the fastest CAGR of 8.60% over the forecast period. The reason behind this growth is the high level of government concern regarding sustainability and strict adherence to circular economy policies. Major stakeholders in the region are now paying more attention to reworking automotive parts to comply with the environmental requirements and minimize waste generation during the industrial process.

- In May 2024, Renault Group and The Future Is NEUTRAL entered into an agreement to establish a new company called THE REMAKERS by merging the remanufacturing expertise of the Flins Re-factory. The joint venture aims at expanding the refurbishment of automotive parts across nine product lines to supply a sustainable and economical alternative to new parts across the European market.

Regulatory Frameworks

- In the U.S., the Federal Trade Commission uses the Green Guides to enforce environmental claims, where remanufactured parts are clearly disclosed to consumers. Also, the Federal Vehicle Repair Cost Savings Act requires federal agencies to prioritize the use of remanufactured components in their vehicle fleets to lower costs and environmental impact.

- In Europe, the End-of-Life Vehicles Directive sets specific targets for the reuse and recovery of vehicle parts, with the objective of achieving 95 percent recovery. This is backed by the Circular Economy Action Plan, which proposes ecodesign requirements to ensure that automotive systems are efficiently disassembled and restored.

- In China, the Circular Economy Promotion Law and the Administrative Measures on Auto Parts Remanufacturing allow certified enterprises to restore critical components like engines and transmissions. Recent State Council revisions permit authorized remanufacturers to purchase high-value cores from scrapped vehicles to improve industrial scale and efficiency.

- In India, the Ministry of Road Transport And Highways manages end-of-life vehicle regulations, which provide a framework through which registered scrap recycling centers can redirect recovered components to the remanufacturing system. This is in line with the National Auto Policy, which aims to standardize quality certifications for all restored automotive parts.

- In Japan, the End-of-Lifecycle Vehicle Recycling Law has established an Extended Producer Responsibility scheme, where manufacturers are responsible for the collection and recovery of vehicle parts. The Ministry Of Economy, Trade And Industry is supported by strict benchmark standards that ensure remanufactured goods comply with original safety certifications.

Competitive Landscape

Major players operating in the automotive remanufacturing industry are forming strategic partnerships and implementing business models based on the circular economy to gain a competitive edge. Large manufacturers are also collaborating with technology experts to incorporate sophisticated diagnostics and automated recovery systems, ensuring that restored parts meet original performance levels.

Moreover, the commercialization of closed-loop supply chains and cross-sector partnerships is being undertaken by industry players to stabilize core material sourcing and mitigate environmental impact. These collaborations and the transition to circularity help stabilize the availability of key components for ICE, BEV, and hybrid propulsion systems and accelerate the shift toward a more sustainable and resource-efficient global automotive aftermarket.

- In April 2025, Stellantis N.V. and Valeo announced an expansion of their strategic alliance to launch the first remanufactured LED headlamps and infotainment display screens in the European market. The partnership aims at industrializing the circular economy operations to reclaim high-value raw materials and reuse intricate electronic components while maintaining their original equipment performance benchmarks.

Key Companies in The Automotive Remanufacturing Market

- LKQ Corporation

- Robert Bosch GmbH

- VALEO

- Caterpillar

- ZF Friedrichshafen AG

- BorgWarner Inc.

- DENSO

- CARDONE Industries

- Cummins Inc

- Eaton

- Schaeffler Technologies AG & Co. KG

- Standard Motor Products, Inc.

- MPA

- JASPER Engines & Transmissions

- ATCDT Corp.

Recent Developments

- In April 2025, Daimler Buses announced the expansion of its e-mobility portfolio through a new project aimed at increasing the service life of electric bus batteries. The project will involve offering remanufacturing services and next-generation battery replacements, aimed at improving the long-term sustainability and financial viability of electrified public transit fleets.