Market Definition

The market encompasses cloud-based storage and computing solutions that allow individuals to store, access, and manage digital content securely across multiple devices. These services operate through remote servers using virtualization, encryption, and automated synchronization to ensure data integrity and accessibility.

Personal clouds are available in public, private, or hybrid models, offering features such as real-time file sharing, media streaming, and backup restoration. They are widely used for storing documents, photos, videos, and other personal files while enabling seamless collaboration and remote access. This market caters to users seeking enhanced data control, security, and cross-platform connectivity.

Personal Cloud Market Overview

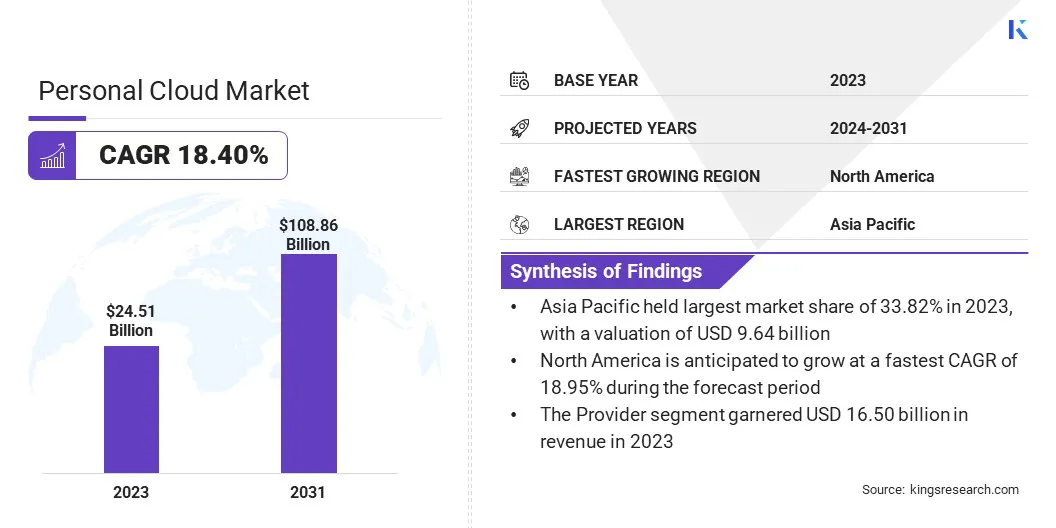

The global personal cloud market size was valued at USD 28.51 billion in 2023 and is projected to grow from USD 33.37 billion in 2024 to USD 108.86 billion by 2031, exhibiting a CAGR of 18.40% during the forecast period.

The surge in digital content creation is driving market growth, as individuals increasingly require seamless storage and access solutions for photos, videos, and documents. The transition to remote work environments has further accelerated demand, enabling employees to collaborate efficiently across locations.

Additionally, the proliferation of smart devices and rising concerns over data security are prompting users to adopt encrypted and synchronized cloud solutions, ensuring data protection and accessibility.

Major companies operating in the personal cloud industry are Apple Inc., Google LLC, Microsoft, Dropbox, Inc., Amazon.com, Inc., pCloud AG, Sync.com Inc., IDrive Inc., SpiderOak Inc., Tresorit, Nextcloud GmbH., QNAP Systems, Inc., Seagate Technology LLC, Internxt, Zoolz, and others.

The surge in digital content creation is propelling the growth of the market. Individuals generate vast amounts of data through mobile devices, social media, and digital transactions. Traditional storage devices lack flexibility and remote accessibility, allowing users to adopt personal cloud services.

Cloud platforms provide seamless storage expansion, reducing reliance on physical hardware. Moreover, the transition to remote work environments is fueling market expansion. Employees and freelancers require secure, on-demand access to documents, presentations, and project files.

Cloud-based storage enables efficient collaboration through real-time editing, file sharing, and version control. Businesses promote personal cloud solutions to enhance worflow flexibility and reduce dependence on physical storage devices.

- In January 2025, IDrive Backup upgraded its Cloud Drive service, enabling users to create and preview Microsoft Word, PowerPoint, Excel, and PDF files directly. The introduction of IDrive for Office improves productivity and efficiency for individuals and businesses by streamlining cloud-based file access and editing.

Key Highlights:

- The personal cloud industry size was recorded at USD 28.51 billion in 2023.

- The market is projected to grow at a CAGR of 18.40% from 2024 to 2031.

- Asia Pacific held a share of 33.82% in 2023, valued at USD 9.64 billion.

- The server device cloud segment garnered USD 9.81 billion in revenue in 2023.

- The provider segment is expected to reach USD 62.92 billion by 2031.

- The consumer segment is likely to grow at a robust CAGR of 18.43% through the projection period.

- North America is anticipated to grow at a CAGR of 18.95% over the forecast period.

Market Driver

Proliferation of Smart Devices

The expansion of smartphones, tablets, and IoT-enabled devices is boosting the expansion of the personal cloud market. Consumers demand real-time access to files, photos, and applications across devices.

Preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker in April 2024 indicates that global smartphone shipments reached 289.4 million units in the first quarter of 2024, reflecting a 7.8% year-over-year increase.

The growing ecosystem of interconnected gadgets, including smart home systems and wearable technology, highlights the need for centralized cloud storage. Cloud services provide synchronization across multiple platforms, ensuring seamless data retrieval.

Users benefit from automatic backups, secure access, and remote file management. The global rise in connected devices is boosting cloud adoption, as users seek integrated solutions for storage, security, and cross-platform accessibility.

Market Challenge

Data Localization and Compliance Issues

A major challenge hampering the progress of the personal cloud market is compliance with data localization and regulatory requirements. Governments in regions such as the EU, China, and India mandate local data storage, restricting cross-border transfers. These regulations create operational complexities and increase infrastructure costs for cloud service providers.

To address this challenge, companies are establishing regional data centers to comply with local laws while ensuring seamless service delivery. Additionally, they are adopting hybrid cloud models that balance local data storage with global accessibility, along with AI-driven compliance management tools to streamline regulatory adherence.

Market Trend

Rising Concerns Over Data Security

Security challenges are influencing the market. Users demand solutions that protect sensitive data from cyber threats, unauthorized access, and data breaches. Cloud providers implement end-to-end encryption, multi-factor authentication, and advanced security frameworks to enhance privacy.

Consumers prefer cloud services that comply with regulatory standards, ensuring data integrity and confidentiality. Cloud storage mitigates risks associated with device theft or data loss. With increasing awareness of cybersecurity threats, individuals and businesses adopt personal cloud solutions with robust encryption and access controls to safeguard digital assets.

- In October 2024, Apple launched Private Cloud Compute(PCC) for researchers, offering up to USD 1 million for identifying vulnerabilities in its secure cloud platform supporting Apple Intelligence features. PCC operates on Apple’s proprietary silicon servers with a custom-designed operating system.

Personal Cloud Market Report Snapshot

|

Segmentation

|

Details

|

|

By Type

|

Server Device Cloud, NAS Device Cloud, Home-Made Cloud, Online Cloud

|

|

By Hosting

|

Provider, User/Self

|

|

By End User

|

Consumer, Enterprises

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Type (Server Device Cloud, NAS Device Cloud, Home-Made Cloud, and Online Cloud): The server device cloud segment earned USD 9.81 billion in 2023 due to its superior storage capacity, enhanced data security, and seamless multi-device synchronization, making it the preferred choice for users seeking reliable and scalable cloud solutions.

- By Hosting (Provider and User/Self): The provider segment held a share of 57.87% in 2023, mainly propelled by its robust infrastructure, advanced security features, and seamless multiple-device integration, ensuring reliable data storage, accessibility, and efficient management.

- By End User (Consumer and Enterprises): The consumer segment is poised to grow at a CAGR of 18.43% through the forecast period, largely attributed to the rising adoption of cloud storage for digital content, remote access, and data backup, supported by increasing smartphone penetration and growing concerns over data security.

Personal Cloud Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

The Asia Pacific personal cloud market share stood at around 33.82% in 2023, valued at USD 9.64 billion. High-speed internet connectivity and the widespread adoption of smartphones are fostering this expansion. Countries such as China, India, and Indonesia are witnessing significant improvements in broadband infrastructure and 5G rollout, making cloud storage more accessible.

The surging adoption of affordable mobile data plans and increasing smartphone ownership is highlighting the need for cloud-based storage solutions, enabling seamlessly data access across devices. As internet penetration expands, cloud service providers benefit from a larger user base.

- According to the GSMA’s Mobile Economy Asia Pacific 2024 report, the mobile industry’s economic contribution in Asia-Pacific is projected to surpass USD 1 trillion by 2030. The region's rapid 5G adoption is expected to boost a 15% sector expansion from 2023 to 2030, exceeding the global average of 12%. Additionally, mobile internet users in the region are forecasted to increase from 1.4 billion (51% penetration) to 1.8 billion (61% penetration) by 2030.

Additionally, domestic cloud service providers in China, India, Japan, and South Korea are expanding, offering localized solutions tailored to regional preferences.

Companies such as Tencent Cloud, Alibaba Cloud, and Reliance Jio Cloud present competitive alternatives to global providers, leveraging data localization policies and regional insights to foster adoption. Their growth bolsters market growth and improves cloud accessibility for individuals and small businesses.

North America market is set to grow at a robust CAGR of 18.95% over the forecast period. North America boasts a highly advanced cloud infrastructures globally, supporting the widespread adoption of personal cloud services. High-speed internet, extensive fiber-optic networks, and the rapid expansion of 5G enable seamless cloud access.

The presence of major cloud service providers, such as Google, Apple, Microsoft, and Amazon, fosters continuous innovation. Well-established data centers and edge computing facilities enhance storage, reduce latency, and improve performance, ensuring widespread adoption across consumers and businesses.

- In June 2024, Apple introduced Apple Intelligence, a personalized AI system operating within a private cloud across its devices. This AI suite delivers tailored services while prioritizing data security. Apple emphasizes that any personal data processed in the cloud is used solely for the requested AI task and is neither retained nor accessible for debugging or quality control.

Furthermore, North America's tech-savvy consumer base recognizes the benefits of cloud storage, including data security, backup, and multi-device accessibility.

High digital literacy boosts the adoption of cloud storage solutions for personal and professional use, supported by educational initiatives and corporate training. Demand for advanced features such as automated backups, AI-powered file organization, and seamless collaboration tools further contributes to regional market expansion.

Regulatory Frameworks

- In Europe, the General Data Protection Regulation (GDPR) governs data protection, enforcing strict guidelines on personal data processing, storage, and transfer. It requires data to be stored within the EU or in countries with equivalent protections, impacting cross-border data management in personal cloud services.

- China's Cybersecurity Law mandates doemstic storage of personal data and business data collected within the country. Companies must undergo security assessments before transferring data abroad, significantly affecting personal cloud service operations.

- South Korea's Personal Information Protection Act (PIPA) is among the world's strictest data laws, imposing rigorous data processing regulations. It further mandates the localization of geospatial and map data, affecting personal cloud services handling such information.

Competitive Landscape

The personal cloud industry is characterized by several market players adopting strategies such as collaborations and integrations to enhance cloud backup solutions, ensuring seamless data protection and management.

By expanding their service offerings and integrating with widely used platforms, companies are strengthening their market presence and addressing growing consumer demand for secure cloud storage. These strategic initiatives contribute to market growth as businesses innovate to deliver more efficient, reliable, and user-friendly solutions.

- In March 2024, IDrive Inc. launched cloud-to-cloud backup for Google personal accounts, allowing users to protect critical data stored across Google services. This integration enables seamless backup of Google Drive files, Gmail messages, photos, and other important data directly through the IDrive interface, enhancing security and accessibility.

List of Key Companies in Personal Cloud Market:

- Apple Inc.

- Google LLC

- Microsoft

- Dropbox, Inc.

- com, Inc.

- pCloud AG

- com Inc.

- IDrive Inc.

- SpiderOak Inc.

- Tresorit

- Nextcloud GmbH.

- QNAP Systems, Inc

- Seagate Technology LLC

- Internxt

- Zoolz

Recent Developments (Expansion/Product Launch)

- In March 2025, IDrive expanded its IDrive e2 S3 Compatible Object Storage platform with new features for improved data management, monitoring, and security. Key additions include Cloud Object Replication, Bucket Event Notifications, and Bucket Logging, offering greater flexibility, control, and protection for object storage operations.

- In February 2025, Nextcloud launched Hub 10, its cloud-based SaaS platform with major security upgrades. The update features end-to-end encryption for web access to encrypted files, enhancing data protection across web, desktop, and mobile devices.

- In June 2024, Apple introduced a series of updates across its platforms designed to enhance user empowerment and data control. Private Cloud Compute extends the advanced security protections of the iPhone to the cloud, enabling users to benefit from intelligent, context-aware features without compromising privacy. Additionally, Apple strengthened its privacy standards with new tools, including locked and hidden apps, providing users with greater control over sensitive information on their devices.