Hybrid Cloud Market Size

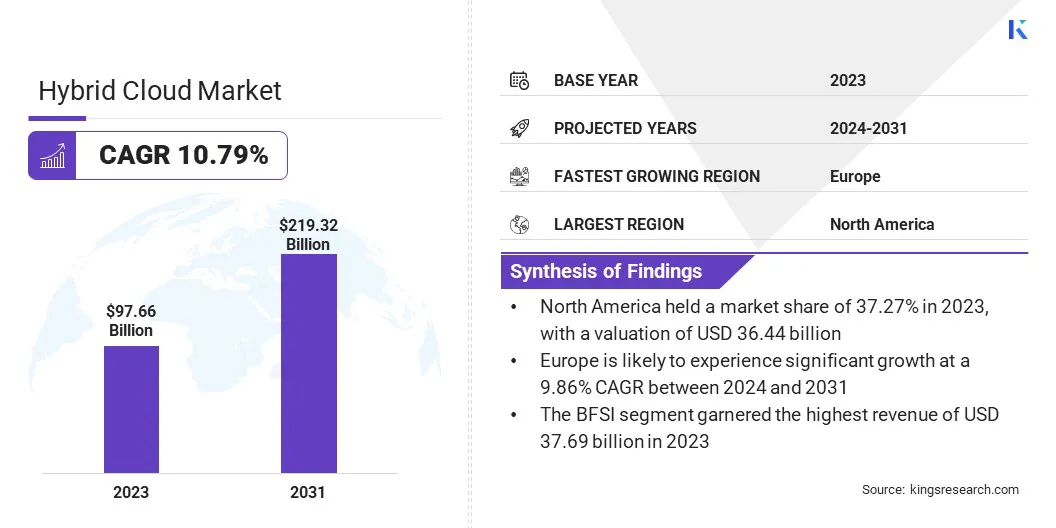

The global Hybrid Cloud Market size was valued at USD 97.76 billion in 2023 and is projected to reach USD 219.32 billion by 2031, growing at a CAGR of 10.79% from 2024 to 2031. In the scope of work, the report includes solutions offered by companies such as IBM Corporation, Microsoft, Oracle, HITACHI, Amazon Web Services, Inc., Google LLC, Broadcom, RACKSPACE US, INC., NetApp, Fujitsu, Atos SE and Others.

Businesses worldwide are increasingly adopting diverse cloud environments, marking a notable trend in the evolution of the hybrid cloud market. This trend is driven by the recognition that a one-size-fits-all approach to cloud infrastructure is often inadequate to meet the complex needs of modern organizations. Instead, enterprises are turning to multi-cloud strategies, leveraging a combination of public, private, and edge cloud services to optimize performance, enhance resilience, and mitigate risks.

The major factor supporting this trend is the growing recognition that different workloads and applications might benefit from specific cloud environments tailored to their requirements. For instance, sensitive data can be stored in a secure private cloud, while compute-intensive tasks can be offloaded to a scalable public cloud.

Additionally, the emergence of specialized cloud providers offering niche services encourages organizations to diversify their cloud portfolios, enabling them to leverage best-of-breed solutions for various use cases.

A hybrid cloud is a computing environment that combines on-premises infrastructure with public and/or private cloud resources, allowing organizations to seamlessly orchestrate workloads across multiple platforms. In a hybrid cloud deployment, solutions encompass a mix of cloud services, including Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS), tailored to meet specific business requirements.

This flexible approach enables enterprises to leverage the scalability, cost-efficiency, and innovation of public cloud offerings while retaining control over sensitive data and critical workloads in private cloud or on-premises environments. Hybrid cloud solutions cater to a wide range of industries, including healthcare, finance, retail, and manufacturing, offering tailored services to address sector-specific challenges and compliance requirements.

Analyst’s Review

The hybrid cloud market is experiencing robust growth, driven by rising demand for flexible, scalable, and secure IT infrastructure solutions. With businesses increasingly implementing digital transformation initiatives, hybrid cloud adoption has become a strategic imperative to modernize operations, enhance agility, and support innovation.

The market with forecasts indicating sustained expansion in the coming years, as organizations across diverse industries continue to leverage hybrid cloud environments to optimize workload management, improve resource utilization, and drive business value.

Emerging trends such as multi-cloud adoption, edge computing integration, and containerization are expected to propel market growth, offering new opportunities for providers to innovate and differentiate their offerings in a dynamic and competitive landscape.

Hybrid Cloud Market Growth Factors

The growing demand for hybrid cloud solutions is driving market expansion. This demand is propelled by the increasing momentum of digital transformation initiatives among businesses across industries.

As organizations strive to innovate, enhance agility, and stay competitive in rapidly evolving markets, they recognize the need for flexible, scalable, and resilient IT infrastructure solutions. Moreover, the increasing complexity of modern workloads, coupled with evolving regulatory compliance requirements, drives the adoption of hybrid cloud solutions.

Enterprises are leveraging hybrid cloud architectures to optimize resource utilization, streamline operations, and enable seamless integration across diverse on-premises and cloud environments, thereby accelerating digital transformation.

- For instance, in March 2024, Fujitsu Limited and Amazon Web Services announced an extended partnership to expedite the modernization of legacy applications on AWS Cloud through the introduction of a joint initiative named Modernization Acceleration.

One notable restraint impeding market expansion is the dependency on legacy infrastructure, which often poses compatibility issues and integration complexities. Many enterprises have invested heavily in on-premises hardware and software systems over the years, creating a heterogeneous IT landscape with disparate technologies, protocols, and architectures.

Migrating legacy applications and workloads to hybrid cloud environments requires careful planning, extensive testing, and sometimes significant reengineering efforts to ensure compatibility, performance, and data integrity.

Moreover, organizational inertia, resistance to change, and the shortage of skilled personnel exacerbate the challenges associated with transitioning to hybrid cloud models. Overcoming these barriers necessitates a strategic approach, comprehensive governance frameworks, and investments in training and upskilling initiatives to empower teams with the expertise needed to navigate the complexities of hybrid cloud adoption successfully.

Hybrid Cloud Market Trends

The growing utilization of container technologies is a notable trend shaping hybrid cloud deployments. Containers offer a lightweight, portable, and scalable solution for packaging and deploying applications across hybrid cloud environments, enabling organizations to achieve greater agility, efficiency, and consistency in their software delivery pipelines.

By abstracting applications from underlying infrastructure dependencies, containers facilitate seamless migration and portability across diverse cloud platforms, on-premises data centers, and edge locations.

For instance, Kubernetes, an open-source container orchestration platform, has emerged as the de facto standard for managing containerized workloads in hybrid cloud environments, providing automated scaling, load balancing, and service discovery capabilities.

As businesses increasingly adopt microservices architectures and DevOps practices, containers play a pivotal role in accelerating application development, deployment, and lifecycle management, thereby fostering innovation and competitiveness in the hybrid cloud market.

Segmentation Analysis

The global hybrid cloud market is segmented based on component, service model, service type, organization size, vertical, and geography.

By Component

Based on component, the market is segmented into solutions and services. The solutions segment dominated the market with a share of 58.65% in 2023 on account of a wide range of offerings such as hybrid cloud management platforms, cloud integration services, security solutions, and data management tools, catering to the diverse needs of businesses transitioning to hybrid cloud environments.

These solutions play a crucial role in addressing challenges related to workload management, data integration, security, and compliance, thereby enabling organizations to fully leverage the potential of hybrid cloud architectures.

Additionally, as businesses increasingly recognize the strategic importance of hybrid cloud adoption for digital transformation initiatives, there is a growing demand for comprehensive solutions that simplify hybrid cloud deployment, orchestration, and management while ensuring seamless integration with existing IT infrastructure.

The dominance of the solutions segment underscores the pivotal role played by technology providers in delivering innovative and value-added solutions, resulting in an increase in hybrid cloud adoption and driving business outcomes.

By Service Model

Based on service model, the market is categorized into infrastructure as a service (IaaS), platform as a service (PaaS), and software as a service (SaaS). The Platform as a Service (PaaS) segment is anticipated to witness the highest CAGR of 12.40% over the forecast period.

PaaS offerings provide developers with a comprehensive platform for building, deploying, and managing applications without the complexity of underlying infrastructure management, thereby fostering the growth of the segment. As businesses increasingly prioritize application modernization and digital innovation, there is a growing demand for PaaS solutions that streamline development workflows, accelerate time-to-market, and enhance developer productivity.

Additionally, PaaS offerings enable organizations to leverage cloud-native technologies such as containerization, serverless computing, and microservices architectures, which are essential for building scalable and resilient applications in hybrid cloud environments.

Furthermore, the shift toward DevOps practices and agile methodologies accelerates the adoption of PaaS solutions, facilitating collaboration between development and operations teams and promoting continuous integration and delivery (CI/CD) pipelines. The PaaS segment is poised to witness significant growth as businesses seek to leverage cloud-native development platforms for driving innovation and gaining a competitive advantage in the hybrid cloud environment.

By Vertical

Based on vertical, the market is classified into BFSI, IT & telecommunications, healthcare, government & public sector, and others. The BFSI segment garnered the highest revenue of USD 37.69 billion in 2023.

The BFSI sector is undergoing a profound digital transformation, driven by changing customer expectations, regulatory requirements, and competitive pressures. As financial institutions strive to deliver personalized and seamless customer experiences, they are increasingly turning to hybrid cloud solutions to modernize legacy infrastructure, enhance agility, and accelerate innovation.

Additionally, the BFSI sector faces unique challenges related to data security, compliance, and scalability, making hybrid cloud architectures an attractive option for balancing the need for regulatory compliance with the flexibility to scale resources dynamically.

Furthermore, the growth of the BFSI sector is fueled by investments in advanced analytics, artificial intelligence, and machine learning capabilities enabled by hybrid cloud platforms. This empowers financial institutions to gain deeper insights, mitigate risks, and drive business growth. The dominance of the BFSI sector in hybrid cloud adoption underscores the strategic importance of technology modernization in driving competitiveness and resilience in the rapidly evolving financial services landscape.

Hybrid Cloud Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

The North America Hybrid Cloud Market share stood around 37.27% in 2023 in the global market, with a valuation of USD 36.44 billion.

The region is home to a large number of leading technology companies and cloud service providers, thereby driving innovation and adoption of hybrid cloud solutions in the region. Additionally, businesses in North America, particularly in sectors such as technology, finance, healthcare, and manufacturing, have adopted hybrid cloud strategies at an early stage to enhance agility, scalability, and competitiveness.

Moreover, favorable regulatory environments, robust digital infrastructure, and a mature ecosystem of technology partners contribute to North America's leading position in the hybrid cloud market. Furthermore, strategic investments in cloud infrastructure, data centers, and emerging technologies fuel the growth of the market in the region.

Europe is likely to experience significant growth at a 9.86% CAGR between 2024 and 2031. Enterprises are increasingly recognizing the strategic importance of hybrid cloud adoption in driving digital transformation initiatives, enhancing operational efficiency, and maintaining competitiveness in the global market. As a result, there is a growing demand for hybrid cloud solutions across various industries, including banking, healthcare, retail, and manufacturing, thereby fueling market growth in the region.

Furthermore, strategic partnerships between European cloud service providers, technology vendors, and industry stakeholders contribute to ecosystem development and innovation in hybrid cloud solutions.

Moreover, the growing emphasis on sustainability and environmental responsibility drives investments in green data centers and renewable energy sources, positioning Europe as a key region in environmentally conscious hybrid cloud deployments. Europe's favorable market dynamics and conducive regulatory environment are expected to propel the growth of the hybrid cloud market in the region in the coming years.

- For instance, in November 2023, Atos introduced Atos Cloud Services for VMware Cloud on AWS, a seamlessly integrated service within VMware Cloud Service that enables customers to swiftly migrate applications to the cloud and seamlessly extend their on-premise VMware environments to VMware Cloud on AWS.

Competitive Landscape

The hybrid cloud market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Expansion & investments are the major strategic initiatives adopted by companies in this sector. Industry players are investing extensively in R&D activities, building new manufacturing facilities, and supply chain optimization.

List of Key Companies in the Hybrid Cloud Market

- IBM Corporation

- Microsoft

- Oracle

- HITACHI

- Amazon Web Services, Inc.

- Google LLC

- Broadcom

- RACKSPACE US, INC.

- NetApp

- Fujitsu

- Atos SE

Key Industry Developments

- March 2024 (Partnership): Hitachi finalized a strategic alliance with Amazon Web Services Japan G.K. to enhance hybrid cloud solutions. Hitachi and AWS are aiming to bolster the advancement of hybrid cloud solutions co-created to facilitate customer system modernization and cloud migration initiatives.

- May 2023 (Launch): IBM introduced IBM Hybrid Cloud Mesh, a Software-as-a-Service (SaaS) solution engineered to empower enterprises to effectively manage their hybrid multi-cloud infrastructure.

- February 2023 (Launch): Microsoft unveiled Azure Operator Nexus, its cutting-edge hybrid cloud platform tailored for communication service providers. This innovative solution aims to enhance and monetize partners' infrastructure, while simultaneously reducing their total cost of ownership.

The global Hybrid Cloud Market is segmented as:

By Component

By Service Model

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

- Software as a Service (SaaS)

By Service Type

- Cloud Management and Orchestration

- Disaster Recovery

- Hybrid Hosting

By Organization Size

- Small and Medium Enterprises

- Large Enterprises

By Vertical

- BFSI

- IT & Telecommunications

- Healthcare

- Government & Public Sector

- Others

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America