Market Definition

The market refers to the industry focused on technologies that capture carbon dioxide (CO₂) directly from the atmosphere. It includes companies developing and deploying scalable solutions for CO₂ removal for mitigating climate change.

The market also covers sectors such as CO₂ storage and utilization. This report outlines the major factors driving the market, along with the competitive landscape shaping the industry over the forecast period.

Direct Air Capture Market Overview

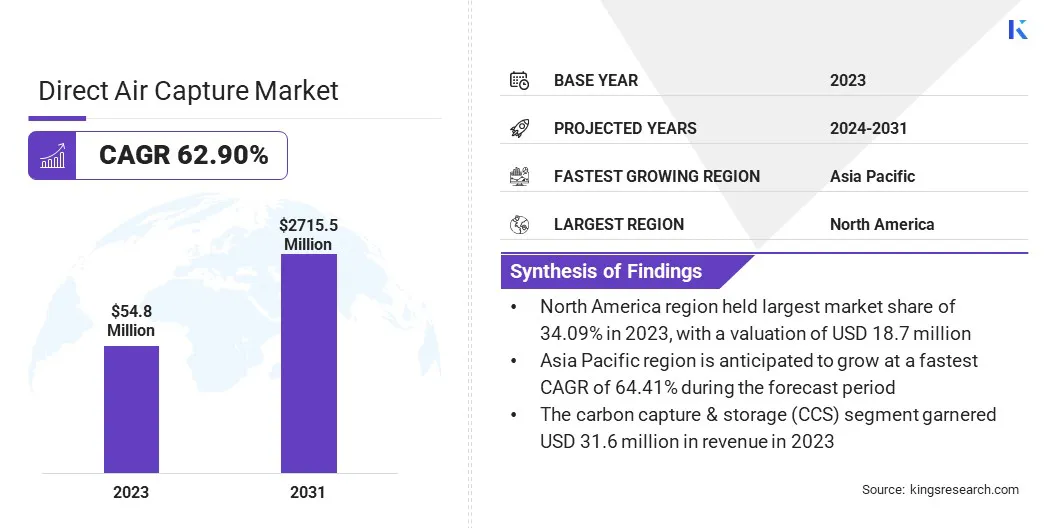

The global direct air capture market size was valued at USD 54.8 million in 2023 and is projected to grow from USD 89.2 million in 2024 to USD 2715.5 million by 2031, exhibiting a CAGR of 62.90% during the forecast period.

Major companies operating in the direct air capture industry are Climeworks, Heirloom Carbon Technologies, Zero Carbon Systems, Carbon Engineering ULC., Skytree., Soletair Power, Avnos, Inc., Noya PBC, RepAir, Svante Technologies Inc., AspiraDAC Pty Ltd, Carbon Clean, Mission Zero Technologies, Twelve Benefit Corporation, and Mosaic Materials Inc.

Rising global carbon emissions are intensifying the demand for scalable carbon removal technologies. Direct Air Capture (DAC) systems are gaining traction as viable solutions for reducing atmospheric CO₂, particularly in hard-to-decarbonize sectors such as heavy industry, aviation, and maritime transport. This is driving increased investment and deployment of DAC technologies to support long-term climate goals and regulatory compliance.

- In November 2024, the Global Carbon Budget report highlighted that global carbon emissions from fossil fuels have reached a record high. According to new research by the Global Carbon Project science team, fossil CO₂ emissions are projected to reach 4 billion tonnes a 0.8% increase from 2023. Including emissions resulting from land-use activities such as deforestation and land degradation, total CO₂ emissions are estimated at 41.6 billion tonnes, up from 40.6 billion tonnes in 2023.

Key Highlights:

- The direct air capture market size was recorded at USD 54.8 million in 2023.

- The market is projected to grow at a CAGR of 62.90% from 2024 to 2031.

- North America held a market share of 34.09% in 2023, with a valuation of USD 18.7 million.

- The solid-dac segment garnered USD 21.1 million in revenue in 2023.

- The carbon capture & storage (CCS) segment is expected to reach USD 1546.0 million by 2031.

- Asia Pacific is anticipated to grow at a CAGR of 64.41% during the forecast period.

Market Driver

Climate Change Mitigation Goals

Increasing government initiatives to meet net-zero emissions targets are driving the market. DAC technology is increasingly recognized as a scalable and efficient solution for removing excess CO₂ from the atmosphere, helping to support long-term mitigation strategies and advance global decarbonization objectives.

Market Challenge

Concerns pertaining to high costs associated with technologies

The global direct air capture market faces significant challenges due to the high capital and operational costs associated with technology deployment and scalability. Current systems are energy-intensive and require advanced infrastructure, making large-scale implementation costly and challenging.

To address these challenges, key players are focusing on enhancing energy efficiency, developing cost-effective materials, and optimizing capture processes. Moreover, market players are leveraging government incentives, including tax credits and subsidies, to further improve project economics.

Market Trend

Technological Advancements

The global market is experiencing significant technological progress as companies focus on increasing operational efficiency, minimizing energy requirements, and lowering overall costs. Key advancements include the development of innovative sorbent materials and improved capture processes that enhance the scalability and effectiveness of DAC systems.

These innovations are enabling systems to extract more carbon dioxide from the atmosphere using less energy, making deployment at larger scales more feasible. As a result, DAC technologies are transitioning from pilot stages to commercially viable solutions.

Their improved performance and cost-efficiency position them as critical tools in global carbon removal strategies, supporting climate goals and net-zero targets.

- In November 2023, Southern California Gas Company (SoCalGas) announced the launch of Hybrid Direct Air Capture (HDAC), an innovative carbon removal technology, in Bakersfield, U.S.

Direct Air Capture Market Report Snapshot

|

Segmentation

|

Details

|

|

By Technology

|

Solid-DAC, Non-Solid-DAC, Electrochemical-DAC

|

|

By Application

|

Carbon Capture & Storage (CCS), Carbon Capture Utilization & Storage (CCUS)

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation:

- By Technology (Solid-DAC, Non-Solid-DAC, Electrochemical-DAC): The solid-dac segment earned USD 21.1 million in 2023 due to its superior efficiency, lower energy requirements, and scalability, making it more cost-effective and commercially viable compared to other DAC technologies.

- By Application (Carbon Capture & Storage (CCS), Carbon Capture Utilization & Storage (CCUS)): The carbon capture & storage (CCS) segment held 57.70% of the market in 2023, due to its established infrastructure, proven effectiveness in large-scale carbon sequestration, and critical role in achieving long-term carbon reduction goals.

Direct Air Capture Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

The North America direct air capture market share stood around 34.09% in 2023 in the global market, with a valuation of USD 18.7 million. The dominance is attributed to significant investments in clean technology. The region benefits from robust financial support, including venture capital and government incentives.

This strong funding ecosystem drives innovation, enables scalable DAC solutions, and establishes North America as a leader in advancing carbon removal technologies.

- In April 2025, Rhodium Group reported that since the U.S. implemented the Inflation Reduction Act (IRA), clean energy manufacturing has become the fastest-growing sector for investment, rising from USD 2.5 billion in Q3 2022 to USD 14.0 billion in Q1 2025. This surge is primarily driven by the electric vehicle supply chain, highlighting the increasing global competition to localize clean technology supply chains and strengthen domestic manufacturing.

Asia Pacific is poised for significant growth at a robust CAGR of 64.41% over the forecast period. The growth is fueled by rapid industrialization, rising environmental awareness, and strong government support for carbon reduction technologies.

Increased clean energy investments by private enterprises and governments are accelerating the development of direct air capture (DAC) solutions. Additionally, robust policy support and sustainability-driven regulations are further driving the adoption of DAC technologies in this region.

Regulatory Frameworks

- In the Asia-Pacific region, Japan proposed common CCS rules through the Asia Zero Emission Community (AZEC) with ASEAN and Australia. These rules emphasize safety standards for storage facilities, carbon volume measurement methods, and monitoring procedures for potential leaks.

Competitive Landscape

The direct air capture market is shaped by strategic acquisitions among key players. Leading companies are strengthening their market positions by acquiring innovative DAC technology firms, boosting their carbon capture and storage capabilities. These strategic moves accelerate technological advancements, expand market reach, and position companies for sustained growth in the rapidly evolving DAC market.

- In August 2023, Occidental entered into a definitive agreement to acquire Carbon Engineering, a Direct Air Capture (DAC) technology innovator, for approximately USD 1.1 billion. This acquisition follows a collaboration between the two companies since 2019 and supports Occidental’s net-zero strategy. It enables its 1PointFive subsidiary to accelerate the deployment of large-scale cost-effective DAC solutions. Carbon Engineering’s proven standardized DAC technology will enhance Occidental’s efforts in advancing global carbon removal initiatives.

List of Key Companies in Direct Air Capture Market:

- Climeworks

- Heirloom Carbon Technologies

- Zero Carbon Systems

- Carbon Engineering ULC.

- Skytree.

- Soletair Power

- Avnos, Inc.

- Noya PBC

- RepAir

- Svante Technologies Inc.

- AspiraDAC Pty Ltd

- Carbon Clean

- Mission Zero Technologies

- Twelve Benefit Corporation

- Mosaic Materials Inc.

Recent Developments (Partnerships)

- In October 2024, Johnson Matthey and Noya formed a partnership to manufacture Noya’s proprietary sorbent, the core component of its advanced direct air capture technology. Noya’s system delivers high-quality carbon removal credits while also providing clean water and grid services, supporting organizations in meeting sustainability goals related to carbon emissions and water usage.

ambitious