Digital Diabetes Management Market Size

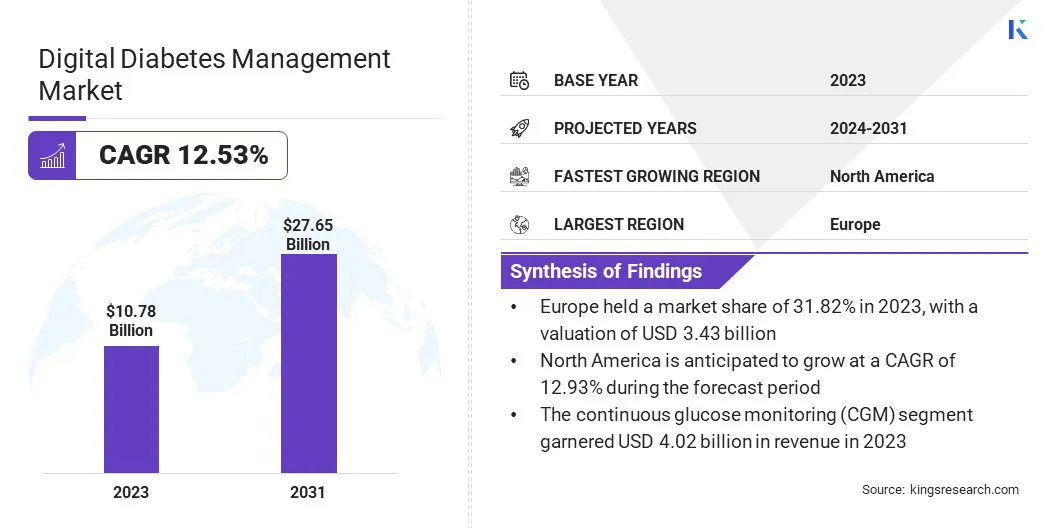

The global Digital Diabetes Management Market size was valued at USD 10.78 billion in 2023 and is projected to reach USD 27.65 billion by 2031, growing at a CAGR of 12.53% from 2024 to 2031. Technological advancements in wearable devices and AI analytics are revolutionizing the landscape of diabetes management. In the scope of work, the report includes solutions offered by companies such as Medtronic plc, Dexcom, Inc., Abbott Laboratories, Roche Diabetes Care, Inc., Insulet Corporation, Tandem Diabetes Care, Inc., Ascensia Diabetes Care Holdings AG, Livongo Health, Inc. (now part of Teladoc Health), Senseonics Holdings, Inc., WellDoc, Inc. and Others.

Wearable devices such as continuous glucose monitors (CGMs) and insulin pumps are becoming increasingly sophisticated, offering real-time monitoring of glucose levels and automated insulin delivery. These devices provide valuable data insights to patients and healthcare providers, enabling personalized treatment plans and timely interventions. AI analytics is further enhancing the capabilities of these devices by analyzing large datasets to identify patterns, predict blood sugar fluctuations, and recommend optimal treatment strategies. Machine learning algorithms have the ability to learn from user behavior and physiological responses, improving the accuracy of glucose predictions and insulin dosage recommendations over time.

Moreover, the integration of wearable devices with AI analytics improves diabetes management outcomes and helps patients better monitor their health. As these technologies continue to evolve, greater precision in devices is enhancing convenience in managing diabetes and improving the quality of life.

Digital diabetes management encompasses the use of technology, such as mobile apps, wearable devices, telemedicine platforms, and data analytics, to monitor, track, and manage diabetes-related parameters. Its application areas include glucose monitoring, medication adherence tracking, diet and exercise management, remote consultations, and data-driven treatment decision support. Regulatory bodies play a crucial role in ensuring the safety, efficacy, and privacy of digital diabetes management solutions. Regulations impact aspects such as data security, interoperability with existing healthcare systems, and approval processes for new technologies, thereby propelling the adoption and growth of the digital diabetes management market globally.

Analyst’s Review

Key players in the global digital diabetes management market are developing user-friendly and interoperable solutions, utilizing AI and data analytics for personalized care, forging partnerships with healthcare providers and technology firms, and complying with regulatory standards. These strategies are enhancing patient engagement, improving treatment outcomes, and streamlining healthcare delivery. In the foreseeable future, these strategies are anticipated to continue shaping the industry landscape by driving innovation, expanding market reach, and addressing evolving healthcare needs.

Digital Diabetes Management Market Growth Factors

The rising prevalence of diabetes worldwide is a significant factor driving the demand for digital diabetes management solutions. According to the World Health Organization (WHO), diabetes rates are steadily increasing due to factors such as sedentary lifestyles, unhealthy diets, obesity, and aging populations. This has led to a growing burden on healthcare systems and increased focus on preventive and proactive healthcare measures.

Digital diabetes management solutions offer scalable and cost-effective tools to monitor and manage diabetes, empower patients with self-care capabilities, and enable healthcare providers to deliver timely interventions and personalized care plans. With the rising prevalence of diabetes, the adoption of digital solutions is anticipated to play a crucial role in mitigating the impact of diabetes-related complications and improving population health outcomes.

However, data privacy and security concerns are hampering the market expansion. The sensitive nature of health data, including glucose levels, medication history, and lifestyle habits, raises concerns about unauthorized access, data breaches, and misuse of personal information. Patients and healthcare providers prioritize the protection of sensitive health data, necessitating robust security measures and compliance with data protection regulations such as GDPR and HIPAA.

To address these challenges, stakeholders in the digital diabetes management market are implementing encryption protocols, secure data storage solutions, access control mechanisms, and regular security audits. Transparent privacy policies, informed consent practices, and user education about data security best practices are playing a crucial role in enhancing trust and confidence in digital health technologies. Collaborating with cybersecurity experts, utilizing blockchain technology for data integrity, and adhering to industry standards for data protection are other strategies that help firms overcome data privacy and security concerns.

Digital Diabetes Management Market Trends

The rise of personalized and preventive healthcare solutions is reshaping the global digital diabetes management market. Personalized approaches utilize data analytics, AI algorithms, and genetic insights to tailor treatment plans according to individual patient needs. This shift improves treatment efficacy, reduces adverse events, and enhances patient engagement and adherence.

Additionally, the integration of digital diabetes management platforms with electronic health records (EHRs) facilitates seamless data exchange, care coordination among healthcare providers, and holistic patient monitoring. Real-time access to patient data, combined with predictive analytics, enables proactive interventions, early disease detection, and population health management initiatives. These trends are driving market growth by improving healthcare outcomes, reducing healthcare costs, and enhancing patient satisfaction.

Segmentation Analysis

The global digital diabetes management market is segmented based on product, end user, and geography.

By Product

Based on product, the market is segmented into continuous glucose monitoring, smart glucometer, smart insulin patch pump, and apps & services. The continuous glucose monitoring (CGM) segment garnered the highest revenue of USD 4.02 billion in 2023. This dominance is attributed to the essential role of CGM in real-time glucose monitoring and diabetes management. CGM devices offer continuous and accurate glucose level readings, enabling patients and healthcare providers to make informed treatment decisions. The growing demand for CGM systems stems from the rising prevalence of diabetes and increasing awareness about continuous glucose monitoring benefits.

Furthermore, reimbursement policies, regulatory approvals, and investments in CGM research and development are contributing to the growth of the segment.

By End User

Based on end user, the market is classified into self/home healthcare, hospitals & clinics, and others. The hospitals & clinics segment held the largest market share of 55.33% in 2023. Hospitals and clinics serve as primary points of care for diabetes diagnosis, treatment, and management, leading to significant adoption of digital diabetes management solutions within these healthcare settings.

Moreover, hospitals and clinics often have established partnerships with digital health solution providers, medical device companies, and pharmaceutical firms, driving technology adoption and innovation within these settings. Growing emphasis on data-driven decision-making, quality patient care, and improved clinical outcomes further incentivizes hospitals and clinics to invest in digital diabetes management tools and platforms. The segment is foreseen to dominate over the review period driven by ongoing advancements and collaborations.

Digital Diabetes Management Market Regional Analysis

Based on region, the global digital diabetes management market is categorized into North America, Europe, Asia-Pacific, MEA, and Latin America.

The Europe Digital Diabetes Management Market share stood around 31.82% in 2023 in the global market, with a valuation of USD 3.43 billion. The region has a well-established healthcare infrastructure, coupled with the widespread adoption of advanced technologies, which creates a conducive environment for digital health solutions. Additionally, the rising prevalence of diabetes in European countries is boosting the demand for innovative diabetes management technologies.

Moreover, supportive regulatory frameworks, robust data privacy regulations, and reimbursement policies for digital health services are encouraging investment and innovation in the sector. Furthermore, strategic collaborations between healthcare providers, technology developers, and research institutions are facilitating the development and adoption of cutting-edge digital diabetes management solutions tailored to patients' healthcare needs. These factors are collectively supporting Europe's prominence in the global digital diabetes management market.

The North America digital diabetes management industry is poised to grow significantly at a CAGR of 12.93% through the forecast period. The region has a high prevalence of diabetes and obesity, which is driving the demand for advanced diabetes management solutions. Additionally, the region boasts advanced healthcare infrastructure, robust technological capabilities, and a favorable regulatory environment, which promotes digital health innovation. Increasing investments in telemedicine, remote patient monitoring, and AI-driven healthcare solutions are further fueling market growth.

Moreover, evolving payment models emphasizing value-based care and population health management incentivize healthcare providers to adopt digital diabetes management technologies. Strategic partnerships between healthcare organizations, technology firms, and pharmaceutical companies are also accelerating product development and market penetration. With continuous advancements in AI analytics, wearable devices, and telehealth platforms, the regional market is poised to witness significant growth and innovation in the forthcoming years.

Competitive Landscape

The global digital diabetes management market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions. Companies are undertaking effective strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, to gain a competitive edge in the market.

List of Key Companies in Digital Diabetes Management Market

- Medtronic plc

- Dexcom, Inc.

- Abbott Laboratories

- Roche Diabetes Care, Inc.

- Insulet Corporation

- Tandem Diabetes Care, Inc.

- Ascensia Diabetes Care Holdings AG

- Livongo Health, Inc. (now part of Teladoc Health)

- Senseonics Holdings, Inc.

- WellDoc, Inc.

Key Industry Development

- August 2023 (Partnership): Kakao Healthcare, a South Korean digital health platform, partnered with Novo Nordisk to enhance digital diabetes management services. The collaboration integrated Kakao's AI capabilities with Novo Nordisk's expertise in diabetes care, providing personalized support for patients. This initiative was aimed to improve diabetes management outcomes through innovative digital solutions, leveraging data analytics and patient engagement tools for more effective healthcare delivery in South Korea and other regions worldwide.

The Global Digital Diabetes Management Market is Segmented as:

By Product

- Continuous Glucose Monitoring

- Smart Glucometer

- Smart Insulin Patch Pump

- Apps & Services

By End User

- Self/Home Healthcare

- Hospitals & Clinics

- Others

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America