Market Definition

The market is the global landscape of devices, systems, and related technologies used for monitoring carbon dioxide levels in exhaled breath across various healthcare settings.

It includes manufacturers, suppliers, and service providers involved in the development, distribution, and maintenance of capnography systems used in hospitals, ambulatory centers, emergency care, and home healthcare environments. The report identifies the principal factors contributing to market expansion, along with an analysis of the competitive landscape influencing its growth trajectory.

Capnography Equipment Market Overview

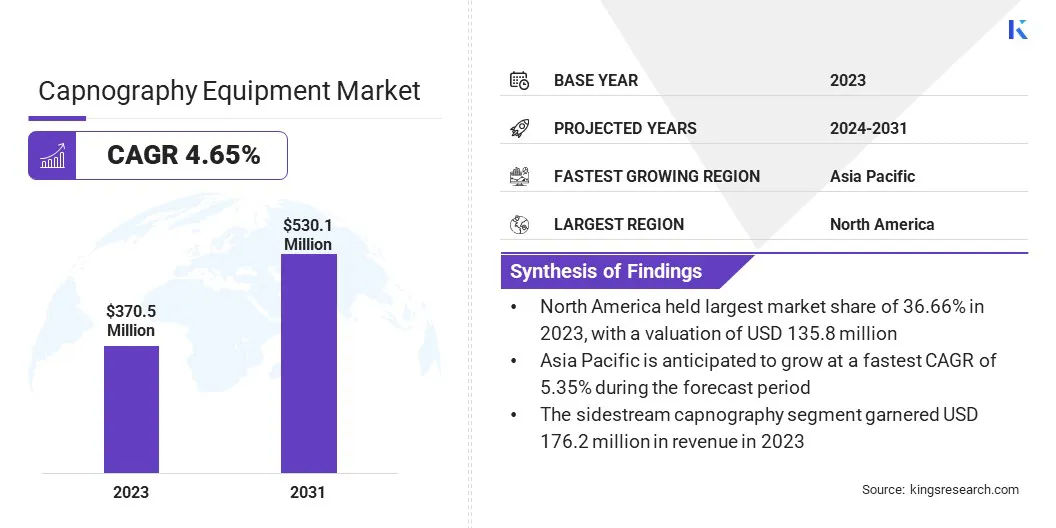

The global capnography equipment market size was valued at USD 370.5 million in 2023 and is projected to grow from USD 385.6 million in 2024 to USD 530.1 million by 2031, exhibiting a CAGR of 4.65% during the forecast period.

The market is growing steadily due to the rising use of breathing monitors in hospitals, especially during surgeries and in emergency care. More people are undergoing medical procedures that require anesthesia, which increases the need for capnography. Newer, portable, and easier-to-use devices are also helping more clinics and ambulances use this technology.

Major companies operating in the capnography equipment industry are Medtronic, Koninklijke Philips N.V., Masimo, Nihon Kohden Corporation, Drägerwerk AG & Co. KGaA, BD, Nonin, ICU Medical, Inc., Hill-Rom Holdings, Inc., Infinium Medical, ZOLL Medical Corporation, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Hamilton Medical, SCHILLER AG, and Zoe Medical, Incorporated.

Healthcare providers are becoming aware of how capnography helps catch breathing problems early. Further, growth in healthcare spending and better medical facilities in developing countries are also helping the market expand.

Key Highlights

- The capnography equipment industry size was valued at USD 370.5 million in 2023.

- The market is projected to grow at a CAGR of 4.65% from 2024 to 2031.

- North America held a market share of 36.66% in 2023, with a valuation of USD 135.8 million.

- The sidestream capnography segment garnered USD 176.2 million in revenue in 2023.

- The respiratory monitoring segment is expected to reach USD 209.5 million by 2031.

- The hospitals segment is expected to reach USD 241.5 million by 2031.

- The market in Asia Pacific is anticipated to grow at a CAGR of 5.35% during the forecast period.

Market Driver

"Rising Prevalence of Respiratory Diseases"

The capnography equipment market is significantly driven by the increasing prevalence of chronic respiratory diseases, such as chronic obstructive pulmonary disease (COPD) and asthma. COPD is a significant cause of disability.

The WHO is actively working to extend the diagnosis and treatment of COPD, particularly in low- and middle-income countries, through initiatives like the Global Action Plan for the Prevention and Control of Noncommunicable Diseases.

As these conditions become common worldwide, there is a growing need for effective monitoring solutions to track respiratory function and CO₂ levels. Capnography equipment assesses respiratory performance and detects potential complications in patients with chronic conditions.

- In November 2024, the World Health Organization (WHO) reported that Chronic Obstructive Pulmonary Disease (COPD) is the fourth leading cause of death in the world. In 2021, it was responsible for 3.5 million deaths.

Market Challenge

"Limited Awareness and Training in Non-Critical Care Settings"

A significant challenge in the capnography equipment market is the limited awareness and training regarding the use of capnography in non-critical care settings.

While capnography is widely used in critical care, its application in general wards, outpatient care, and home healthcare remains underutilized. Many healthcare providers lack the necessary training to interpret capnography data effectively. This hampers the early detection of respiratory issues.

To address this challenge, healthcare systems can invest in comprehensive training programs for clinicians and raise awareness about the benefits of capnography in routine monitoring. This could help expand its usage and improve patient outcomes outside of high-acuity environments.

Market Trend

"Advancements in Multi-Parameter Monitoring Systems"

A significant trend in the capnography equipment market is the integration of CO₂ measurements into multi-parameter patient monitoring systems. This allows healthcare providers to monitor various critical parameters, such as respiratory function, brain activity, and oxygen levels, in a single device.

By combining these technologies, clinicians can obtain a more comprehensive and real-time view of patient health, improve decision-making, and streamline clinical workflows. This trend is especially prominent in settings where quick, informed decisions are crucial for patient outcomes, driving the demand for advanced monitoring solutions.

- In June 2023, Philips and Masimo partnered to enhance Philips' high acuity patient monitors. The collaboration focused on integrating SedLine Brain Function Monitoring, Regional Oximetry, and CO₂ measurements into Philips’ IntelliVue MX750 and MX850 monitors to enable clinicians to make quick and informed decisions with a more holistic view of the patient.

Capnography Equipment Market Report Snapshot

|

Segmentation

|

Details

|

|

By Technology Type

|

Mainstream Capnography, Sidestream Capnography, Microstream Capnography

|

|

By Application

|

Cardiac Care, Trauma and Emergency Care, Respiratory Monitoring, Others

|

|

By End User

|

Hospitals, Ambulatory Surgery Centers, Home Care Settings, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Technology Type (Mainstream Capnography, Sidestream Capnography, and Microstream Capnography): The sidestream capnography segment earned USD 176.2 million in 2023 due to its ease of integration with existing monitoring systems and suitability for use in patients without a breathing tube.

- By Application (Cardiac Care, Trauma and Emergency Care, Respiratory Monitoring, and Others): The respiratory monitoring segment held 38.91% of the market in 2023, owing to increasing cases of chronic respiratory diseases and the growing need for continuous CO₂ monitoring.

- By End User (Hospitals, Ambulatory Surgery Centers, Home Care Settings, and Others): The hospitals segment is projected to reach USD 241.5 million by 2031, owing to high patient volumes, greater availability of advanced medical equipment, and widespread use of capnography during surgeries and critical care.

Capnography Equipment Market Regional Analysis

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America capnography equipment market share stood at around 36.66% in 2023 in the global market, with a valuation of USD 135.8 million. The strong market presence of this region is primarily due to high volume of surgical procedures and widespread use of capnography in emergency medical services (EMS).

In the U.S., the integration of capnography into routine monitoring across operating rooms and intensive care units has significantly contributed to regional demand. Additionally, EMS providers in the U.S. and Canada rely on portable capnography devices for pre-hospital care, further fueling market growth in this region.

The Asia Pacific is expected to register the fastest growth in the capnography equipment industry, at a projected CAGR of 5.35% over the forecast period. This growth is largely attributed to increasing incidence of respiratory and cardiac conditions, particularly in densely populated countries like China and India.

Rapid urbanization and increasing air pollution levels in major cities have further surged these cases, boosting the need for continuous CO₂ monitoring. Additionally, growing private healthcare facilities and infrastructure imporvements are promoting the adoption of capnography equipment in surgical and emergency care settings.

Regulatory Frameworks

- In the U.S., capnography equipment is regulated by the U.S. Food and Drug Administration (FDA). The FDA ensures the safety, effectiveness, and quality of these medical devices before they can be marketed.

- In the European Union, capnography equipment falls under the Medical Device Regulation requiring a CE mark for market access. EMA is responsible for the scientific evaluation and supervision of medical devices, including capnographs that are marketed in the EU.

- In Japan, capnography equipment is regulated under the Pharmaceuticals and Medical Devices Act (PMD Act), with the Pharmaceuticals and Medical Devices Agency (PMDA) overseeing approvals. The Ministry of Health, Labour and Welfare handles broader administrative actions like product approvals and whether a product is considered a medical device.

Competitive Landscape

The capnography equipment industry is characterized by several established as well as emerging players actively developing strategies to strengthen their market position. Key participants are focusing on innovation, particularly device portability, connectivity, and integration with multi-parameter monitoring systems.

Many companies are expanding their product lines by introducing compact, user-friendly capnography devices for non-hospital settings such as ambulatory care and emergency response.

Strategic partnerships and collaborations with healthcare providers, research institutions, and distributors are commonly used to increase geographic reach and penetration. Mergers and acquisitions help consolidating market share and accelerating access to new technologies and customer bases.

List of Key Companies in Capnography Equipment Market:

- Medtronic

- Koninklijke Philips N.V.

- Masimo

- Nihon Kohden Corporation

- Drägerwerk AG & Co. KGaA

- BD

- Nonin

- ICU Medical, Inc.

- Hill-Rom Holdings, Inc.

- Infinium Medical

- ZOLL Medical Corporation

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Hamilton Medical

- SCHILLER AG

- Zoe Medical, Incorporated