Market Definition

The market encompasses cloud-based computing solutions optimized for processing, rendering, and delivering high-quality visual content. It involves AI-driven video encoding, real-time graphics rendering, and media streaming through cloud infrastructure.

Key applications include cloud gaming, virtual desktop infrastructure (VDI), video analytics, and augmented reality (AR) processing. The market relies on GPU-accelerated cloud instances, containerized workloads, and edge computing integration to enhance latency-sensitive visual applications.

Enterprises leverage visual cloud solutions for AI-driven content moderation, automated video editing, and immersive media experiences. Additionally, sectors such as healthcare, retail, and manufacturing utilize these technologies for remote diagnostics, digital signage, and real-time simulation.

Visual Cloud Market Overview

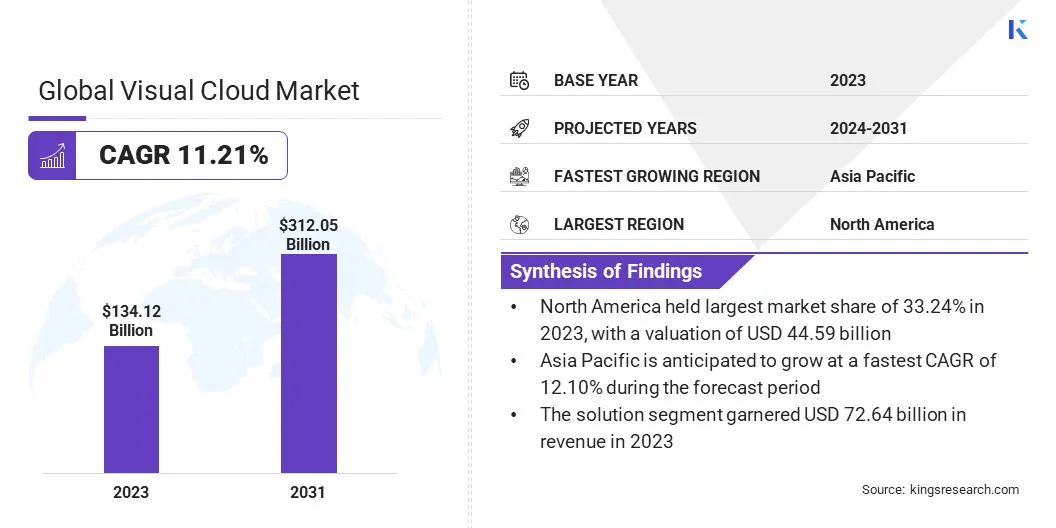

The global visual cloud market size was valued at USD 134.12 billion in 2023 and is projected to grow from USD 148.33 billion in 2024 to USD 312.05 billion by 2031, exhibiting a CAGR of 11.21% during the forecast period.

Market growth is driven by the increasing adoption of AI-powered video analytics for real-time surveillance, security, and content optimization. Enterprises are leveraging cloud-based GPU infrastructure to support high-performance workloads, including 3D rendering, virtual desktop infrastructure (VDI), and immersive media applications.

Additionally, rising investments in edge computing enhance low-latency processing, enabling seamless streaming and real-time data insights across industries.

Major companies operating in the visual cloud industry are Amazon.com, Inc., Microsoft, Google, IBM, Oracle, Zoom Communications, Inc., Alibaba Cloud, Avaya, Cisco Systems Inc., Adobe, NVIDIA Corporation, Salesforce, Broadcom, ServiceNow, Advanced Micro Devices, Inc., and others.

The deployment of 5G networks is accelerating the adoption of visual cloud applications by enabling high-speed, low-latency connectivity for video streaming, cloud gaming, and AI-driven analytics. Ultra-fast data transmission is enhancing the performance of cloud-based AR/VR experiences, remote video surveillance, and interactive digital signage.

Telecom providers are integrating 5G with cloud-based video services to support real-time broadcasting, autonomous vehicle monitoring, and smart city applications. Businesses are leveraging 5G-powered cloud infrastructure for AI-driven visual content generation, immersive customer experiences, and high-definition video conferencing. The expansion of 5G connectivity is fueling market growth by enabling seamless real-time processing.

- In June 2023, Samsung Electronics and NAVER Cloud expanded their collaboration to deploy Korea’s first private 5G network in the construction sector for Hoban Construction. This initiative aims to enhance worksite safety and efficiency by integrating advanced 5G applications.

Key Highlights:

- The visual cloud industry size was recorded at USD 134.12 billion in 2023.

- The market is projected to grow at a CAGR of 11.21% from 2024 to 2031.

- North America held a share of 33.24% in 2023, valued at USD 44.59 billion.

- The solution segment garnered USD 72.64 billion in revenue in 2023.

- The large enterprises segment is expected to reach USD 180.24 billion by 2031.

- The government segment is set to grow at a robust CAGR of 11.50% through the forecast period.

- Asia Pacific is anticipated to grow at a CAGR of 12.10% through the projection period.

Market Driver

Rising Demand for Cloud-Based Security and Surveillance

Increasing concerns over cloud security, as highlighted in the Cloud Security Alliance’s 2024 study, are reinforcing the demand for cloud-based security and surveillance solutions, propelling the expansion of the visual cloud market. Cloud security is a top concern for 65% of security and IT management professionals, with 72% expecting its importance to increase.

Attacks on cloud management infrastructure have surged, reported by 72% of respondents. Additionally, 44% experienced a cloud data breach, with 31% citing misconfiguration or human error as the cause.

The increasing prevalence of cyber threats targeting cloud infrastructure is prompting organizations to adopt AI-powered security analytics and cloud-integrated surveillance systems to enhance threat detection and real-time monitoring. Cloud platforms provide scalable video storage, secure remote access, and AI-driven facial recognition, strengthening access control and anomaly detection.

Governments and enterprises are investing in cloud-integrated security solutions for smart city surveillance, retail loss prevention, and transportation monitoring. AI-powered video analytics support behavior detection, anomaly recognition, and automated alert systems, reducing response times and enhancing situational awareness.

Rising cloud security risks are compelling industries to invest in intelligent surveillance and fraud detection solutions, highlighting the need for visual cloud for security applications.

Market Challenge

Data Security and Privacy Concerns

Data security and privacy concerns present a major challenge to the growth of the visual cloud market. As enterprises adopt cloud-based visual processing, sensitive data, such as real-time video surveillance, AI-powered analytics, and user-generated content, becomes vulnerable to cyber threats and regulatory risks. Unauthorized access, data breaches, and compliance with region-specific data protection laws further hinder market expansion.

To mitigate these risks, companies are enhancing encryption techniques, deploying AI-driven threat detection, and adopting zero-trust security frameworks. Strategic partnerships with cybersecurity firms and compliance-focused cloud architectures help organizations strengthen data protection while ensuring adherence to global regulatory standards.

Market Trend

Growing Investments in Cloud Infrastructure and Data Centers

Leading cloud service providers are expanding data center infrastructure to support the increasing demand for high-performance visual computing. Investments in high-capacity GPUs, AI-driven cloud instances, and high-speed networking solutions are strengthening cloud-based visual applications.

Enterprises are shifting workloads to hyperscale cloud environments for AI-powered video processing, rendering, and analytics, stimulating the growth of the market.

Cloud providers are integrating containerized workloads, serverless computing, and scalable storage solutions to enhance visual cloud efficiency. Increased adoption of multi-cloud strategies is driving investment in cloud-based visual applications across industries.

- In February 2025, Alibaba Cloud introduced its first data center in Mexico to expand its global digital infrastructure and cloud computing services. This facility is designed to provide local businesses with access to cloud computing resources. It aims to support companies seeking to modernize their IT infrastructure and transition to cloud-based solutions.

Visual Cloud Market Report Snapshot

|

Segmentation

|

Details

|

|

By Offering

|

Solution, Services

|

|

By Organization Size

|

Small & Medium Enterprises, Large Enterprises

|

|

By Industry Vertical

|

IT & Telecommunications, Media & Entertainment, Retail, Government, Healthcare, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Offering (Solution and Services): The solution segment earned USD 72.64 billion in 2023 due to the increasing adoption of AI-driven video analytics, cloud-based rendering, and immersive content processing, enabling enterprises to enhance security, optimize workflows, and deliver high-performance visual computing across industries.

- By Organization Size (Small & Medium Enterprises and Large Enterprises): The large enterprises segment held a share of 57.86% in 2023, fueled by the increasing adoption of AI-powered video analytics, cloud-based GPU infrastructure, and scalable data processing solutions to support high-performance workloads, enterprise security, and real-time collaboration across multiple locations.

- By Industry Vertical (IT & Telecommunications, Media & Entertainment, Retail, Government, Healthcare, and Others): The government segment is set to grow at a CAGR of 11.50% through the forecast period, largely attributed to the increasing adoption of AI-powered surveillance, smart city initiatives, and cloud-based data analytics for public safety, traffic management, and national security, propelling demand for scalable, real-time processing solutions.

Visual Cloud Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

The North America visual cloud market share stood at around 33.24% in 2023, valued at USD 44.59 billion. Governments across North America are investing in cloud-integrated surveillance and AI-powered traffic monitoring to enhance urban security and infrastructure management.

Cities such as New York, Toronto, and San Francisco are deploying cloud-based video analytics for smart traffic control, emergency response optimization, and automated public safety monitoring. Cloud-enabled surveillance networks are improving real-time data sharing among law enforcement agencies, leading to increased demand for high-performance visual cloud solutions in urban security applications.

Additionally, prominent cloud service providers, including Microsoft Azure, Google Cloud, and AWS, are expanding their data center capabilities to support visual cloud workloads.

The development of GPU-accelerated cloud platforms is fueling demand for AI-driven video processing, immersive AR/VR applications, and cloud-based game streaming. With ongoing investments in high-performance computing and AI-optimized cloud services, North America remains a key hub for visual cloud innovation and enterprise adoption.

- In January 2025, Microsoft announced an USD 80 billion investment in AI-enabled data centers for its current fiscal year, focusing on training large language models and deploying AI and cloud-based applications. Rising AI workloads previously have strained cloud capacity, accelerating data center expansion. Additionally, in September 2024, Microsoft partnered with BlackRock, MGX, and Global Infrastructure Partners to raise USD 100 billion for data center and power infrastructure development.

Asia Pacific visual cloud industry is estimated to grow at a robust CAGR of 12.10% over the forecast period. Countries such as China, Singapore, and India are deploying AI-powered visual cloud solutions for traffic monitoring, urban security, and real-time emergency response.

China's extensive network of cloud-integrated surveillance cameras, backed by state-sponsored AI research, is boosting large-scale adoption. Singapore's Smart Nation initiative leverages cloud-based video analytics for urban management, while India's Smart Cities Mission is expanding AI-powered security solutions across metropolitan areas.

The Asia-Pacific region is witnessing a surge in cloud gaming and esports, supported by high consumer demand and increasing investments in 5G infrastructure. Leading cloud providers such as Tencent Cloud and Alibaba Cloud are enhancing GPU-accelerated visual cloud platforms to support real-time game streaming and AI-enhanced gaming experiences.

Japan and South Korea are leading markets for cloud gaming, with companies such as Sony and Nvidia expanding their cloud-based gaming services. The rise of mobile gaming in Southeast Asia is further fueling demand for visual cloud technology, enhancing game streaming quality and reducing latency.

- In February 2025, The Game Company (TGC), a pioneer in AI-driven cloud gaming, announced its partnership with Tencent Cloud, a global leader in cloud technology and gaming innovation. This collaboration leverages Tencent Cloud’s advanced infrastructure to enhance gaming performance, accessibility, and engagement, particularly in the Asia-Pacific region.

Regulatory Frameworks

- The CLOUD Act mandates U.S.-based cloud providers to comply with government data requests regardless of storage location, impacting global data sovereignty. State regulations, including the California Consumer Privacy Act (CCPA), impose stringent data protection requirements, influencing cloud security frameworks. Compliance with sector-specific laws such as HIPAA and FISMA remains essential.

- In Europe, the GDPR enforces stringent data protection rules, requiring cloud providers to implement robust security measures and obtain user consent for data processing. Companies must comply with data localization laws in certain member states. The EU-U.S. Data Privacy Framework governs transatlantic data transfers, affecting multinational cloud services.

- In China, the Cybersecurity Law mandates strict data localization, requiring cloud providers to store certain data within China. The Personal Information Protection Law (PIPL) regulates data collection and transfer, enforcing stringent cross-border transfer requirements. Companies operating cloud services must comply with national security reviews and sector-specific regulations affecting data storage and encryption.

- In Japan, the Act on the Protection of Personal Information (APPI) governs cloud data processing, requiring security compliance and consent for data transfers. Japan’s data adequacy agreement with the EU facilitates cross-border transfers, while the Telecommunications Business Act regulates cloud service handling personal and business data.

Competitive Landscape

The visual cloud industry is characterized by a number of market players engaging in strategic partnerships to integrate generative AI into enterprise technology. These collaborations enable companies to leverage advanced AI-driven automation, streamline workflows, and optimize decision-making processes.

By integrating generative AI into cloud-based platforms, businesses can enhance operational efficiency, improve customer engagement, and strengthen cybersecurity measures.

Such initiatives facilitate AI-powered solutions across industries, including IT services, finance, and healthcare. As organizations prioritize AI adoption for digital transformation, these strategic alliances are accelerating the expansion of AI-driven enterprise solutions.

- In January 2025, ServiceNow and Google Cloud expanded their partnership to enhance the integration of generative AI across enterprise technology layers. ServiceNow's Now Platform and complete suite of workflows will be accessible on Google Cloud Marketplace., while its Customer Relationship Management (CRM), IT Service Management (ITSM), and Security Incident Response (SIR) solutions will be available on Google Distributed Cloud (GDC).

List of Key Companies in Visual Cloud Market:

- Amazon.com, Inc.

- Microsoft

- Google

- IBM

- Oracle

- Zoom Communications, Inc.

- Alibaba Cloud

- Avaya

- Cisco Systems Inc.

- Adobe

- NVIDIA Corporation

- Salesforce

- Broadcom

- ServiceNow

- Advanced Micro Devices, Inc.

Recent Developments (Partnerships/Agreements/Product Launch)

- In February 2025, Zoom Communications, Inc. and Mitel announced the global rollout of a hybrid cloud solution that seamlessly integrates Zoom Workplace and Zoom AI Companion with Mitel’s flagship communications platforms, including its leading telephony solutions. This offering addresses the increasing enterprise demand for hybrid unified communications (UC) by providing a "best-of-both-worlds" approach. It enables organizations to combine robust, mission-critical communication capabilities with advanced collaboration features, enhancing business productivity and operational efficiency.

- In June 2024, Cisco introduced new capabilities to the Cisco Security Cloud, expanding its cross-domain security platform to support evolving cybersecurity needs. The company also unveiled Cisco Hypershield, an advanced security architecture designed to protect modern AI-scale data centers. Hypershield integrates enforcement points within virtual machines and Kubernetes clusters in public cloud environments using eBPF, an open-source technology eBPF.

- In February 2024, Hitachi Vantara, a subsidiary of Hitachi specializing in data storage, infrastructure, and hybrid cloud management, expanded its partnership with Cisco. The collaboration introduced Hitachi EverFlex with Cisco Powered Hybrid Cloud, a suite of hybrid cloud services leveraging automation and predictive analytics to enhance infrastructure management, cost efficiency, and operational performance.