Market Definition

Telehealth is a remote healthcare service that utilizes technology, including video conferencing and secure messaging, to facilitate virtual consultations between patients and healthcare providers. It enables individuals to receive medical advice, access treatments, and manage their health without the need for in-person visits to a medical facility.

Telehealth enhances convenience, reduces costs, and significantly improves accessibility to healthcare services, particularly in scenarios where physical appointments are impractical. Its adoption has reached unprecedented levels, with significant utilization in the fields of radiology, cardiology, behavioral health, and virtual consultations.

Telehealth Market Overview

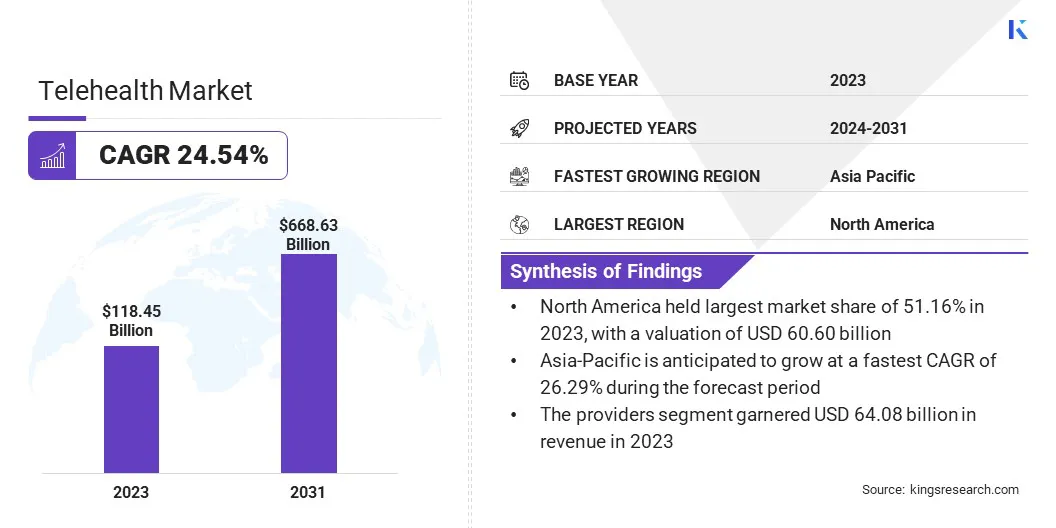

Global telehealth market size was valued at USD 118.45 billion in 2023, which is estimated to be valued at USD 143.92 billion in 2024 and reach USD 668.63 billion by 2031, growing at a CAGR of 24.54% from 2024 to 2031.

The rising adoption of telehealth facilities by patients, physicians, and government authorities, due to improved internet connectivity and technological advancements, is boosting the market. Access to healthcare through specific applications and video consultations enables communication between patients and doctors in remote locations, eliminating the need to visit hospitals or clinics.

Moreover, the market is propelled by favorable government initiatives to expand telehealth by making healthcare services more accessible and convenient for patients. The focus on cost-effective and efficient healthcare solutions further propels the adoption of telehealth services.

- In 21 November 2024, the VietNam Ministry of Health (MOH), in collaboration with the United Nations Development Programme (UNDP) and the Korean Foundation for International Healthcare (KOFIH), officially launched the project “Telehealth to improve access to healthcare services for disadvantaged groups in Viet Nam.” This project aims to improve the health of disadvantaged populations by boosting digital transformation in health and enhancing the accessibility and quality of grassroots health services.

Telehealth services are rapidly expanding, particularly in cardiology, behavioral health, radiology, and online consultations. This growth is fueled by a surge in startup funding and the introduction of new solutions and services, especially those designed for virtual consultations.

- In March 2023, Royal Philips introduced Philips Virtual Care Management. It includes flexible solutions and services that help various healthcare stakeholders effectively engage with patients, including health systems, payers, providers, and employer groups.

Major companies operating in the telehealth market are Teladoc, AMD Global Telemedicine, Inc., Amwell, Medtronic, Cerner, CISCO Systems, Doctor On Demand, Siemens Healthcare, GE HealthCare, Doximity, MDLive, PlushCare, Doxy.me, Vidyo, and CareCloud, Inc.

Regulations, particularly the Health Insurance Portability and Accountability Act (HIPAA) of 1996 and its amendments under the Health Information Technology for Economic and Clinical Health (HITECH) Act, positively impact market growth.

These regulations play a crucial role in ensuring digital health information's secure handling and privacy, shaping the operational framework and compliance standards for telehealth services, especially in the U.S.

Key Highlights:

- The global telehealth industry size was valued at USD 118.45 billion in 2023.

- The market is projected to grow at a CAGR of 24.54% from 2024 to 2031.

- North America held a market share of 51.16% in 2023, with a valuation of USD 60.60 billion.

- The telecare segment garnered USD 35.68 billion revenue in 2023.

- The software segment aggregated to reach USD 55.71 billion in 2023.

- The web-based segment is expected to reach USD 182.76 billion by 2031.

- The providers segment is expected to reach USD 429.21 billion by 2031.

- The telehealth industry in Asia Pacific is anticipated to grow at a CAGR of 26.29% during the forecast period.

Market Driver

"Integration of Technologies Such as Blockchain and AI"

The integration of advanced technologies like blockchain and AI significantly enhances the potential of the telehealth market. In addressing infectious diseases, telehealth enables timely and efficient healthcare by allowing remote diagnosis, monitoring, and treatment. This approach helps curb disease spread, facilitates early interventions, and alleviates pressure on traditional healthcare systems.

Blockchain’s decentralized and secure framework ensures data integrity and privacy, addressing key concerns in healthcare information exchange. AI, with its capabilities for accurate diagnostics, personalized treatment plans, and predictive analytics, empowers healthcare providers to analyze patient data remotely, enabling informed decision-making and improved outcomes.

Additionally, AI-driven chatbots and virtual assistants enhance patient experiences through timely information, scheduling, and continuous support. Together, telehealth and these technologies present a transformative opportunity to advance healthcare delivery in the face of ongoing and emerging infectious threats.

- In January 2025, Helfie AI, an Australian health tech startup, introduced a telehealth platform integrating AI and blockchain to enable self-testing for conditions like COVID-19, tuberculosis, and sexually transmitted infections (STIs). The platform has gained over 70 corporate and government clients globally.

Market Challenge

"Concerns Pertaining to Hygiene, Cleanliness, and Behavioral Barriers"

One of the significant obstacles is the challenge of ensuring hygiene and cleanliness standards in virtual healthcare interactions, particularly when traditional physical examinations are not possible. This hurdle demands the development of standardized protocols and the integration of remote monitoring devices to maintain cleanliness without compromising the accuracy of assessments.

Additionally, behavioral barriers to the widespread adoption of telehealth services must be addressed through extensive education and awareness campaigns, emphasizing the efficacy, convenience, and safety of virtual care.

Market Trend

"Focus on Personalized and Preventive Care Through Digital Platforms"

The telehealth market is increasingly focusing on personalized and preventive care through digital platforms, aiming to tailor healthcare services to individual needs and proactively address health issues before they escalate. This approach leverages advanced technologies to analyze patient data, enabling healthcare providers to offer customized care plans and early interventions.

Digital health tools, such as mobile applications and wearable devices, facilitate continuous monitoring of health metrics, empowering patients to engage actively in their health management. For instance, health apps can provide personalized tips, enhancing patient engagement and adherence to preventive measures.

- In Jan 2025, MyBVI is a smartphone application that uses two photos to assess risks for heart disease, stroke, and diabetes. It provides a Body Volume Index (BVI) score, which is 23% more accurate than BMI, offering a more precise measure of body composition and health risks.

- Function Health, co-founded by Dr. Mark Hyman, offers personalized health testing with extensive blood tests covering over 105 metrics. It provides detailed health reports without prescribing specific treatments, emphasizing prevention and proactive health management.

Telehealth Market Report Snapshot

| Segmentation |

Details |

| By Delivery Model |

Web-Based, Cloud-Based, On-Premises |

| By Application |

Telecare, Teleradiology, Telepsychiatry, Teleconsultation, Tele-ICU, Others |

| By End User |

Payers, Providers, Patients |

| By Product |

Software (Telehealth platforms, Mobile health applications, EHR-integrated telehealth solutions), Hardware (Telehealth kiosks, Wearable devices, Diagnostic instruments), Services (Tele-consultation, Tele-monitoring, Tele-education, Tele-surgery) |

| By Region |

North America: U.S., Canada, Mexico |

| Europe: France, U.K., Spain, Germany, Italy, Russia, Rest of Europe |

| Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific |

| Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa |

| South America: Brazil, Argentina, Rest of South America |

Market Segmentation:

- By Product (Software, Hardware, Services): The software segment earned USD 55.71 billion in 2023, due to its applications, favorable government initiatives, and a rise in demand for technologically advanced healthcare IT solutions.

- By Delivery Model (Web-based, Cloud-based, On-premises): The web-based segment held 45.90% of the market in 2023, owing to its rising adoption among enterprises.

- By Application (Telecare, Teleradiology, Telepsychiatry, Teleconsultation, Tele-ICU, Others): The teleradiology segment is estimated to grow at a CAGR of 28.25% over the forecast period, owing to the advancements in imaging technology enabling accurate remote diagnoses and the rising demand for remote healthcare solutions.

- By End User (Payers, Providers, Patients): The providers segment is projected to reach USD 429.21 billion by 2031, due to the rising awareness among healthcare professionals.

Telehealth Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America accounted for a significant market share of around 51.16% in 2023, valued at USD 60.60 billion. Key factors driving the market in the region include the higher healthcare IT expenditure, rapid adoption of smartphones, a significant shortage of primary caregivers, advancements in coverage networks, growing geriatric population, surge in chronic disease prevalence, increasing healthcare costs, and a rising need for enhanced prevention and management of chronic conditions.

The telehealth market in the U.S. dominates the region, owing to innovative software development, advanced healthcare management, and the presence of several market players operating across segments such as mobile and network operations.

However, the market in Asia Pacific is anticipated to witness the fastest growth over the forecast period with a CAGR of 26.29%. Factors such as the growing investments and geriatric population in countries such as Japan and India, along with technological advancements in digital health and research initiatives undertaken by the key players in the region, are anticipated to contribute to the market growth.

- For instance, in 2023, the Australian Government invested around USD 107.2 million in digital health programs and innovations to update their healthcare system.

Regulatory Framework Also Plays a Significant Role in Shaping the Market.

- In North America, the U.S. has a dual-level regulatory system with federal and state authorities overseeing telehealth services. At the federal level, the Health Insurance Portability and Accountability Act (HIPAA) ensures the privacy and security of patient information. State-level regulations govern medical licensing, with some states adopting parity laws that require equal reimbursement for telehealth and in-person services. Additionally, the Interstate Medical Licensure Compact (IMLC) facilitates multi-state licensing for physicians.

- In Canada, telehealth is regulated by federal and provincial governments. The Personal Information Protection and Electronic Documents Act (PIPEDA) governs data privacy for telehealth services, while provincial authorities manage licensure and healthcare delivery.

- In Asia Pacific, countries like China, Japan, India, and Australia have diverse regulatory approaches to telehealth. In China, the National Health Commission (NHC) oversees telemedicine practices, with specific guidelines for internet hospitals and remote diagnostics. Data privacy is protected under the Personal Information Protection Law (PIPL) and Cybersecurity Law, ensuring compliance with strict localization and security requirements.

- Japan’s telehealth framework, regulated by the Ministry of Health, Labour and Welfare (MHLW), allows telemedicine under certain conditions. The Act on the Protection of Personal Information (APPI) governs data protection, emphasizing patient consent and secure data handling.

- India’s telehealth framework, outlined in the Telemedicine Practice Guidelines, 2020, standardizes remote healthcare services.

- In Australia, the Medicare Benefits Schedule (MBS) provides coverage for telehealth services, with significant expansion during the pandemic. The Therapeutic Goods Administration (TGA) regulates digital health products, while data privacy is ensured under the Privacy Act, 1988, and the My Health Records Act, 2012.

Competitive Landscape

The market is characterized by a number of participants, including both established corporations and rising organizations. The telehealth market is highly competitive, driven by technological advancements, service differentiation, and evolving consumer needs.

Key players, including established firms and emerging startups, compete by offering comprehensive solutions such as virtual consultations, remote monitoring, and AI-driven diagnostics. Technological innovation is central, with AI, IoMT devices, and blockchain enabling personalized care, real-time monitoring, and secure data management.

Companies also focus on integrated healthcare ecosystems that combine teleconsultations, e-prescriptions, and hybrid care models to enhance user experience and streamline workflows. Strategic collaborations with insurers, pharmaceutical companies, and technology providers further strengthen market presence and scalability.

Regulatory adaptability and cost efficiency are critical for success, as telehealth companies navigate diverse legal environments and price-sensitive markets. The telehealth market is marked by consolidation, with mergers and acquisitions driving scale and diversification. Consumer trust, built through robust data security, transparent pricing, and clinical excellence, remains a key differentiator.

Key market players focus on improving digital health experience by providing numerous solutions through different subscription plans and emphasizing data security while some are developing Chatbot services for basic medical inquiries and one-time consultations.

For instance, WeChat offers Chatbot services in China for basic medical inquiries and other mobile health solutions such as booking appointments, accessing medical records, and paying medical bills.

- In June 2024, MetroHealth and MUSC Health launched Ovatient, the first virtual healthcare company. Ovatient integrates with hospital systems and patients’ medical records via Epic and MyChart, providing a personalized patient experience that empowers care teams with nearly real-time data.

List of Key Companies in Telehealth Market:

- Teladoc

- AMD Global Telemedicine, Inc.

- Amwell

- Medtronic

- Cerner

- CISCO Systems

- Doctor On Demand

- Siemens Healthcare

- GE HealthCare

- Doximity

- MDLive

- PlushCare

- Doxy.me

- Vidyo

- CareCloud, Inc.

Recent Developments:

- In October 2023, Glenn Gaunt MD, announced its official launch, introducing an alternative to traditional healthcare. The platform offers accessible and convenient healthcare services, enabling patients to receive medical attention from the comfort of their homes.

- In September 2023, Apollo Telehealth introduced Tele-Emergency ICU services across nine NTPC plants, enhancing critical care capabilities. This initiative aims to provide remote medical supervision and support for emergency situations, leveraging advanced telehealth technologies.

- In August 2023, Spark Biomedical launched telehealth services for Sparrow Ascent to improve patient access to opioid withdrawal treatment. Sparrow Ascent is a medication-assisted treatment (MAT) program that provides comprehensive care for individuals struggling with opioid use disorder. The program utilizes a combination of medication, counseling, and support services to help patients achieve long-term recovery.