Market Definition

The virtual office market offers remote office services, where individuals and companies can conduct their professional activities without having a traditional physical office. The virtual office service usually covers a business address, mail-handling, telephone reception, access to meeting rooms, and administrative services that are provided through online platforms or third-party providers.

This market serves freelancers, startups, small and medium-sized enterprises (SMEs), and large corporations seeking flexibility, cost savings, and operational scalability. Virtual offices enable companies to experience the prestige and functionality of a physical office at a much lower cost by utilizing both physical and digital resources to facilitate remote operations.

Virtual Office Market Overview

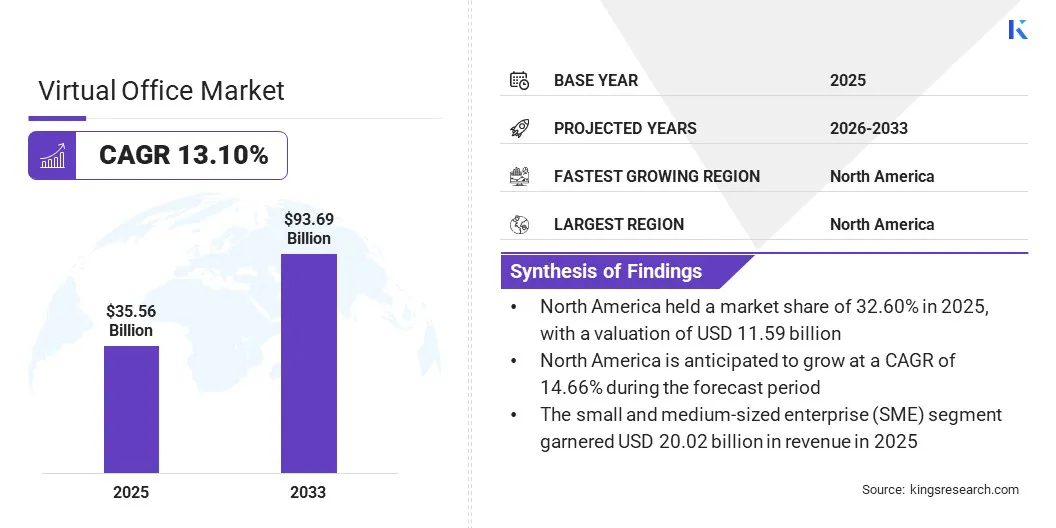

The global virtual office market size was valued at USD 35.56 billion in 2025 and is projected to grow from USD 39.59 billion in 2026 to USD 93.69 billion by 2033, exhibiting a CAGR of 13.10% during the forecast period. This robust growth is supported by the rising use of remote and hybrid work systems, along with cost-saving benefits for businesses and advancements in digital collaboration technologies.

Major companies operating in the global virtual office industry are International Workplace Group plc, WeWork Companies Inc., Servcorp, The Executive Centre, Industrious, Davinci virtual office, alliancevirtualoffices.com, Opus Virtual Offices, iPostal1, Awfis Space Solutions Limited, instaspaces.in, The Instant Group, Mindspace, Venture X, and Vast Coworking.

The growth of the market is also boosted by the increased demand for flexible business solutions, international business growth, and the necessity of a professional business address without any significant overhead expenses. The market is expected to record long-term growth and innovation in the next few years as organizations continue to concentrate on flexibility and operational efficiency.

- In May 2025, Servcorp introduced a new workspace in Riyadh, Saudi Arabia, offering premium virtual office services and flexible workspaces. The center has state-of-the-art facilities to cater to local and international companies, exemplifying Servcorp’s interest in expanding its virtual office presence in key international markets.

Key Market Highlights

- The global virtual office market size was USD 35.56 billion in 2025.

- The market is projected to grow at a CAGR of 13.10% from 2025 to 2033.

- North America held a share of 32.60% in 2025, valued at USD 11.59 billion.

- The address segment garnered USD 11.52 billion in revenue in 2025.

- The cloud-based segment is expected to reach USD 54.65 billion by 2033.

- The small and medium-sized enterprise (SME) segment is anticipated to witness the fastest CAGR of 13.84% over the forecast period.

- The IT & telecommunications segment garnered USD 11.59 billion in revenue in 2025.

- Europe is anticipated to grow at a CAGR of 13.47% through the projection period.

How is the shift toward remote and hybrid work driving market growth?

The growth of remote and hybrid work models is a major driver of the virtual office market. With the rising adoption of flexible working arrangements by businesses, there has been a decline in the demand for traditional offices. Companies are seeking ways for employees to work effectively from any place while still representing the company professionally. Virtual offices offer essential services such as business addresses, mail handling, and access to meeting rooms without the costs or commitments of physical offices.

According to the Australian Bureau of Statistics (ABS), as of August 2025, 36% of employed people regularly worked from home, reflecting the sustained shift toward remote work arrangements. This adaptability allows companies to attract and retain talent from a wider geographic area and respond quickly to changing business environments. With remote work and hybrid work becoming the new norm, the market is growing as demand for virtual office solutions continues to rise.

How are data security and privacy concerns hindering the growth of the virtual office market?

Businesses are becoming increasingly dependent on online platforms to handle sensitive information and communication. Cyberattacks, data breaches, and unauthorized access are likely to jeopardize client confidentiality and the reputation of organizations. Since virtual offices usually involve accessing important business records and personal information over the Internet, it is important to ensure that robust security measures are in place.

Regulatory compliance, such as adhering to the GDPR or other data protection laws, adds further complexity for providers operating across multiple jurisdictions.

To address these challenges, businesses are investing in advanced cybersecurity solutions, including end-to-end encryption, multi-factor authentication, and secure cloud storage. Furthermore, periodic training for staff on best practices in data protection can enhance organizational security against possible attacks.

How is the integration of advanced technology influencing the growth of the virtual office market?

The growing use of advanced technology is one of the most important trends in the virtual office industry. Virtual office providers are adopting artificial intelligence and automation to streamline administrative processes such as virtual reception, call handling, and digital mail management. The use of cloud-based collaboration tools and secure virtual meeting rooms has become standard, enabling teams to communicate and share documents efficiently from anywhere.

Additionally, AI-driven workspace apps and assistants are being introduced by industry leaders to provide an enhanced user experience, improve productivity, and strengthen operational control.

On January 3, 2026, SoWork reported that remote work is being transformed by AI-driven virtual offices that can simulate face-to-face collaboration through avatars, spatial audio, and immersive digital workspaces. This has resulted in an 83% increase in productivity, and a 41% reduction in meetings, with technologies such as meeting summaries, action items extraction, and team analytics saving teams an average of 3.5 hours per week.

With more companies demanding efficient and flexible solutions, the continued adoption of advanced technology is likely to become the new standard for service quality, fueling market growth.

Virtual Office Market Report Snapshot

|

Segmentation

|

Details

|

|

By Type

|

Address, Communication, Mail Handling, Reception/Virtual Assistant, and Others

|

|

By Deployment

|

On-premise, Cloud-based, and Hybrid

|

|

By Organization Size

|

Small and Medium-sized Enterprise (SME), and Large Enterprise

|

|

By End User Vertical

|

Banking, Financial Services, and Insurance (BFSI), Healthcare, IT & Telecommunications, Commercial, and Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Type (Address, Communication, Mail Handling, Reception/Virtual Assistant, and Others): The address segment earned USD 11.52 billion in 2025, mainly because of the increasing demand by businesses to have the prestigious business addresses without incurring the expenses of renting physical office space. It is especially sought-after by startups, freelancers, and small businesses that aim to improve their professional image and credibility while maintaining operational flexibility and minimizing costs.

- By Deployment (On-premise, Cloud-based, and Hybrid): The cloud-based segment held a share of 52.60% in 2025, as it can provide scalable, affordable, and easily accessible solutions to businesses of any size. The rapid adoption of cloud technology facilitates effortless remote work, data storage, and integration with other digital tools, which makes it a preferred option for organizations adopting flexibility and efficiency in virtual offices.

- By Organization Size (Small and Medium-sized Enterprise (SME) and Large Enterprise): The small and medium-sized enterprise (SME) segment is projected to reach USD 55.61 billion by 2033, due to the growing popularity of virtual office solutions that offer organizations cost savings, flexibility in their operations, and global market access. The SMEs are rapidly using these services to build a professional presence, streamline business processes, and facilitate remote work, boosting segmental growth.

- By End User Vertical (Banking, Financial Services, and Insurance (BFSI), Healthcare, IT & Telecommunications, Commercial, and Others): The IT & telecommunications segment is anticipated to grow at a CAGR of 15.26% through the projection period, due to the high concentration of the sector on digital transformation and remote working facilitation. The growing use of cloud-based communication tools, virtual collaboration platforms, and the need for flexible workspace are creating a strong demand for virtual office solutions, aiding segmental expansion.

What is the market scenario in North America and Europe?

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America virtual office market share stood at 32.60% in 2025, valued at USD 11.59 billion. This strong market presence is largely attributed to the region’s highly developed digital infrastructure and the early adoption of cutting-edge communication technologies. The presence of a strong business environment, extensive broadband availability, and robust demand for affordable business solutions has helped the region to gain prominence in the market.

The use of virtual offices is propelled by the evolution of remote work, particularly among technology companies, startups, and professional service providers. Moreover, increased funding in cloud services and collaboration applications is highlighting the need for service providers. As innovation continues and the regulatory climate is favorable, North America will continue to be a major player in the market.

The Europe virtual office market is set to grow at a CAGR of 13.47% over the forecast period. This growth is supported by the increasing interest in sustainability, flexible working, and cross-border expansion of business in the region. Many European countries are seeing a surge in remote work adoption, facilitated by evolving labor regulations and a highly skilled workforce.

Moreover, the increase in the number of startups and SMEs that seek to increase their presence in new markets is fueling the demand for virtual office services. The rise in connectivity in the continent, along with investment in digital infrastructure and smart-city projects, is also contributing to the adoption of virtual office solutions in Europe.

- In May 2025, Nordic cluster organizations collaborated with the National Institute for Health and Care Research (NIHR) to open the Nordic Virtual Office. The project is aimed at helping healthcare companies access the UK market, enabling collaboration, innovation, and a smoother entry of Nordic health solutions into the UK healthcare market.

Regulatory Frameworks

- In the United Arab Emirates, Economic Substance Regulations (ESR) regulate the demonstration of a substantial business presence. Such regulations mandate that virtual office companies demonstrate an actual economic presence at the registered address to be entitled to tax benefits, as well as adhere to international standards.

- In the UK, the Companies Act 2006 regulates business registration and address requirements. It requires that a business have a registered office address, and virtual office solutions are a valuable and legally accepted alternative for incorporating a company and facilitating communication.

- In the EU, data privacy and protection are regulated by the General Data Protection Regulation (GDPR). It sets stringent criteria for gathering, processing, and storing personal information, ensuring that virtual office providers can manage customer information safely and transparently.

Competitive Landscape

The competitive landscape of the virtual office market is highly dynamic and marked by both global and regional providers offering a wide range of services. The competition revolves around issues like pricing, technological strengths, customization of services, and geographical coverage. Providers offer differentiated features such as mail handling, call management, access to meeting spaces, and integration of enhanced digital tools to facilitate remote collaboration.

Remote and hybrid work have intensified competition in the market, which has stimulated constant innovation and service portfolio growth. Strategic partnerships, investments in technology, and a focus on customer experience are key strategies as companies strive to enhance their offerings and secure a larger share of the growing market.

- In June 2025, ITOCHU Corporation introduced the protein drink Tanpaku Charge, created through its internal Virtual Office platform, which allows cross-departmental collaboration. The platform enables interaction between departments, supports innovation, accelerates product development, and is part of the overall strategy of ITOCHU to use virtual office systems to improve business performance and adapt to market demands.

Key Companies in The Virtual Office Market

- International Workplace Group plc

- WeWork Companies Inc.

- Servcorp

- The Executive Centre

- Industrious

- Davinci virtual office

- alliancevirtualoffices.com

- Opus Virtual Offices

- iPostal1

- Awfis Space Solutions Limited

- instaspaces.in

- The Instant Group

- Mindspace

- Venture X

- Vast Coworking

Recent Developments (Launch)

- In March 2025, Nexudus introduced a Virtual Offices module designed for workspace operators to provide services including mail handling and business addresses. This module helps operators diversify their offerings and generate additional revenue while meeting the needs of remote and hybrid working environments.