Market Definition

The CoWoS (Chip-on-Wafer-on-Substrate) market refers to the ecosystem of advanced semiconductor packaging technology that enables the heterogeneous integration of multiple semiconductor dies. These dies include logic processors, GPUs, AI accelerators, SoCs, chiplets, and high-bandwidth memory (HBM) assembled into a single, high-performance package using chip-on-wafer-on-substrate architecture. Rising investments in advanced packaging technologies, semiconductor fabrication capacity expansion, and the next-generation processor development is further creating growth opportunities for emerging AI, HPC, and data-centric computing platforms in the CoWoS industry.

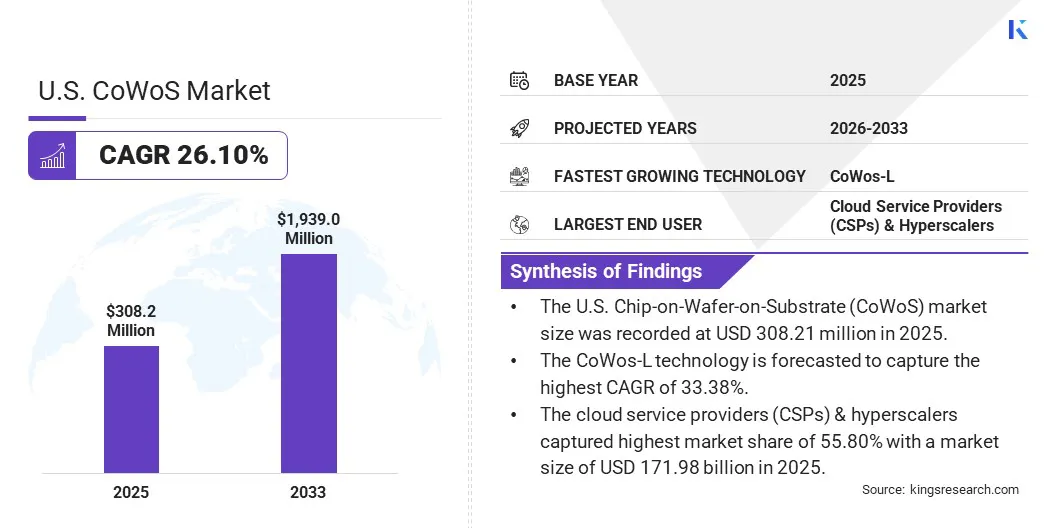

CoWoS Market Overview

The U.S. CoWoS market size was valued at USD 308.21 million in 2025 and is projected to reach USD 1,939.02 million by 2033, representing a CAGR of 26.10% over the forecast period. The market growth is driven by the demand for advanced packaging that integrates multiple processors, high-bandwidth memory (HBM) stacks, and memory dies on a single chip. This technology addresses the massive computational demands of AI workloads and High-Performance Computing (HPC) without altering the physical limitations of the chip.

Key players operating in the market, including Taiwan Semiconductor Manufacturing Company, Samsung Electronics Co., Ltd., ASE Technology Holding Co, Ltd., Amkor Technology, Inc., Intel Corporation, NVIDIA Corporation, Advanced Micro Devices, Inc., Broadcom Inc., Deca Technologies, Micron Technology, Inc., Powertech Technology Inc. and others, are boosting production by strategic capacity expansion in order to address the shortages in the chip supply across the U.S.

- In June 2026, TSMC and Amkor Technology announced a 10-year strategic partnership to expand advanced semiconductor packaging and testing capabilities in Arizona (U.S.). The agreement involves TSMC procuring advanced packaging and testing services from Amkor to address rising demand for high-performance computing, artificial intelligence, and advanced electronics.

Key Market Highlights:

- The U.S. Chip-on-Wafer-on-Substrate (CoWoS) market size was recorded at USD 308.21 million in 2025.

- The market is projected to grow at a CAGR of 26.10% from 2026 to 2033.

- The CoWos-L technology is forecasted to capture the highest CAGR of 33.38% over the forecast period, reaching an estimated valuation of USD 1149.38 million in 2033, up from USD 120.20 million in 2025.

- The ASIC component type garnered the highest market share of 63.40% in 2025, with a valuation of USD 195.40 million.

- The cloud service providers (CSPs) and hyperscalers captured the highest market share of 55.80%, with a market size of USD 171.98 million in 2025.

Increasing demand for the state-of-the-art AI, machine learning, and data center applications is leading to higher demand for semiconductor packaging technologies such as CoWoS. The packaging involves stacking multiple high-bandwidth memory (HBM) chips with their GPUs on a single substrate, resulting in size reduction and performance enhancements to handle AI and machine learning workloads.

The U.S. dominance in data centers and high-performance computing fuels the demand for GPU deployments to handle large-scale AI training and inference tasks. Data centers process enormous datasets, which creates unprecedented demand for high enterprise logic chips that offer substantially higher memory bandwidth, storage capacity, and energy efficiency.

- In January 2025, OpenAI, SoftBank, Oracle, and the Abu Dhabi-based investment fund MGX announced the Stargate AI project, a USD 500 billion 10 GW artificial intelligence computing infrastructure initiative. Later, the project was updated with the installation of 400,000 NVIDIA GB200 superchips for training and running artificial intelligence (AI) systems.

How does the concentration of CoWoS packaging capacity negatively impact the U.S. semiconductor market?

Constrained supply, shifting manufacturing capacity allocation, and surging AI and data center demand fuel the demand for enterprise-grade, high-capacity, and high-performance memory solutions leading to the occupancy of CoWoS packaging facilities.

AI model training, deployment, and inference require more memory as GPUs necessitate substantial volumes of fast memory to handle complex AI models. This accelerates demand for advanced memory technologies and influences capacity allocation across the global memory market.

CoWoS is regarded as one of the most important bottlenecks in the AI semiconductor supply chain as it connects leading-edge logic with HBM in advanced AI packages. The property enables its utility to fit HBM next to GPUs and AI accelerators, leading to growth in its adoption across HPC computing environments. The concentration of CoWoS capacity at TSMC acts as a significant restraint for the U.S., as limited production capacity and reported oversubscription of CoWoS facility till 2026 make it the single tightest part of the AI semiconductor stack. This scenario hampers the widespread growth avenues for the overall semiconductor supply chain.

For instance, in December 2025, CoWoS-S and CoWoS-L lines of TSMC are reported fully booked with lead times ranging from 52 to 78 weeks, where the company expanded monthly capacity by 120,000–130,000 wafers per month to address total 2026 demand, which is estimated near 1.0 million wafers. Additionally, high customer concentration with NVIDIA accounting for about 60% of CoWoS packaging capacity and the top three customers, including NVIDIA, Broadcom, and AMD, together utilizing over 85% of the total TSMC CoWoS capacity restrains the market growth avenues for the U.S. semiconductor industry.

To address the challenge, market players are investing in advanced process technologies and next-generation chip fabrication facilities that integrate multiple chiplets within a single package, thus addressing the rising demand for next-generation AI and high-performance computing (HPC) chips to handle workloads.

- In March 2026, Intel Corporation rolled out its advanced EMIB-T (Embedded Multi-die Interconnect Bridge Through Silicon) packaging technology into production. The move is targeted at challenging the advanced packaging monopoly of TSMC amid severe industry-wide AI chip supply bottlenecks.

How is the adoption of Panel-Level Packaging (PLP) and CoPoS emerging as a notable trend in the U.S. advanced semiconductor packaging market?

Panel-Level Packaging (PLP) replaces traditional circular wafers with large rectangular panels to improve manufacturing efficiency, reduce costs, and support high-volume production. The technology involves integration of multiple dies and high-density interconnects on a larger processing area. This results in lower cost per package, higher throughput, improved electrical and thermal performance, and greater design flexibility, leading to enhanced applicability across AI accelerators, high-performance computing (HPC), automotive electronics, 5G, and mobile devices. The adoption of chiplet architectures and surge in demand for high-performance, energy-efficient systems is anticipated to position PLP as a foundational technology in advanced semiconductor packaging.

- In July 2026, Intel and TSMC unveiled plans to accelerate the adoption of panel-level packaging (FO-PLP) and glass substrate technologies to support the rising size and complexity of AI and high-performance computing chips.

Moreover, the introduction of innovative technologies such as Chip-on-Panel-on-Substrate, which is also known as “panel-level advanced packaging technology," is creating new growth avenues for the market. CoPoS replaces the silicon interposer with a glass-based substrate layered with ABF, which enables the fabrication of larger AI chip packages.

- In June 2026, TSMC launched a pilot line using CoPoS at the Longtan facility operated by its subsidiary VisEra Technologies. The company is targeting limited-volume production during the second half of 2026 and 2027 and parallelly continuing technology verification and process refinement.

- In March 2026, NVIDIA showcased the Feynman AI chip at GTC 2026, which is planned for launch in 2028. The chip is the first to be manufactured using a 1 nm-class process and is designed to push limitations of cooling and power management in servers.

CoWoS Market Report Snapshot

|

Segmentation

|

Details

|

|

By Technology

|

CoWos-S, CoWos-R, CoWos-L

|

|

By Component Type

|

ASIC, CPU, FPGA, GPU, Others

|

|

By End User

|

Cloud Service Providers (CSPs) & Hyperscalers, AI Cloud & GPU-as-a-Service Providers, Enterprise Data Centers, Telecommunications & Networking, Government, Defense & Supercomputing Centers, Others

|

|

By Country

|

U.S.

|

Market Segmentation

- By Technology (CoWos-S, CoWos-R, CoWos-L). The CoWos-L technology is forecasted to capture the highest CAGR of 33.38% over the forecast period, reaching an estimated valuation of USD 1149.38 million in 2033 from USD 120.20 million in 2025. The high growth rate is attributable to the adoption of large AI accelerators, which require advanced multi-chip integration and higher interconnect density to handle next-generation AI and HPC workloads.

- By Component Type (ASIC, CPU, FPGA, GPU, Others). The ASIC component type garnered the highest market share of 63.40% in 2025 with a valuation of USD 195.40 million in 2025. The high share is due to the deployment of AI accelerators and processors that rely on CoWoS packaging to deliver superior performance, power efficiency, and memory bandwidth.

- By End User (Cloud Service Providers (CSPs) & Hyperscalers, AI Cloud & GPU-as-a-Service Providers, Enterprise Data Centers, Telecommunications & Networking, Government, Defense & Supercomputing Centers, and Others). The cloud service providers (CSPs) & hyperscalers captured the highest market share of 55.80% with a market size of USD 171.98 million in 2025. The rise in investments in AI infrastructure and hyperscale data center expansion to address generative AI and high-performance computing workloads contributes to the high share.

The dominance of the U.S. in data centers, artificial intelligence, and high-performance computing fuels the demand for logic chips required to train, deploy, and enhance the computational power of AI models. The rise in demand is driving investments in the U.S. semiconductor industry to increase chip production, with the CHIPS and Science Act acting as a pivotal base boosting new private investments in semiconductor manufacturing estimated at USD 450 billion across 28 states in the U.S. The demand for efficient chips which combine multiple dies and pack on a single substrate and offer improved power efficiency, thermal performance, and compact footprint critical for AI, HPC, and cloud workloads drives the growth of the CoWoS market in the U.S.

Additionally, the advanced LLMs and increasing generative AI applicability across the commercial and industrial landscape of the U.S. further fuel high-capacity and fast memory processing chips that handle the rising computing workloads. The transition of artificial intelligence beyond pilot projects towards embedding AI directly into core business operations further drives the demand for efficient computing chips, thereby creating growth avenues for CoWoS in the U.S. market.

- In April 2026, the Semiconductor Equipment and Materials International (SEMI) projected investments exceeding USD 151 billion in 300 mm memory fabrication equipment by 2027. The high demand is driven by strong AI-led demand for advanced memory technologies, including HBM, DDR5, and 3D NAND. CoWoS equipment spending is further anticipated to reach USD 37 billion, driven by rising adoption of AI accelerators and cloud infrastructure.

Regulatory Frameworks

- The SEMI S2 guidelines specify guidelines for maintaining chemical emissions from semiconductor equipment to be kept in the air extremely low, as less than 1% of the American Conference of Governmental Industrial Hygienists (ACGIH) threshold limit value (TLV) or permissible exposure limit (PEL) during normal equipment operation.

- The Semiconductor Superiority Act amends the CHIPS and Science Act and extends Section 48D tax credits to space-based semiconductor manufacturing. The Act is targeted at boosting U.S. investment in microgravity chip production; strengthening domestic semiconductor capabilities; improving supply chain resilience; and enhancing global competitiveness.

Competitive Landscape

Key players operating in the market are incorporating strategic mergers, acquisitions, and technical collaborations to strengthen their competitive positioning and capture a larger share of the market. Market players are emphasizing expansion of advanced packaging capacity, strengthening supply chain capabilities, and securing long-term manufacturing partnerships to address the rising demand for AI and high-performance computing applications. Companies are further undertaking strategic acquisitions to accelerate capacity expansion and gain access to advanced production infrastructure and investing in next-generation packaging technologies to cater to future demands for AI chips.

- In April 2026, Taiwan Semiconductor Manufacturing Company (TSMC) unveiled plans to open an advanced chip packaging facility in Arizona by 2029 to support the growing demand for AI chips and strengthen semiconductor manufacturing in the United States. The plant will provide CoWoS and 3D-IC packaging technologies, which are essential for assembling modern AI processors used by companies such as Nvidia and Apple.

- In January 2026, Micron Technology, Inc. signed a Letter of Intent for the acquisition of the P5 fabrication site of PSMC in Tongluo, Taiwan, for USD 1.8 billion. The acquisition is targeted at expanding the CoWoS production and addressing rising global demand for memory solutions.

- In April 2025, TSMC Limited announced the expansion of CoWoS capabilities to support larger interposers. The company announced a transition from 3.5X reticle size to 5X, 9X, and beyond to address the rising AI demand for logic and HBM.

Key Companies In The U.S. CoWoS Market :

- Taiwan Semiconductor Manufacturing Company Limited

- Samsung Electronics Co., Ltd.

- ASE Technology Holding Co, Ltd.

- Amkor Technology, Inc.

- Intel Corporation

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Broadcom Inc.

- Marvell Technology, Inc.

- Deca Technologies, Inc.

- Micron Technology, Inc.

- Powertech Technology Inc.

- United Microelectronics Corporation

- Chipbond Technology Corporation

- JCET Group Co., Ltd.

Recent Developments

- In June 2026, AMD introduced Versal Premium Gen 2 Memory-on-Package (MoP) adaptive SoCs, which integrate up to 32 GB of LPDDR5X memory directly into the chip package and deliver 288 GB/s memory bandwidth, resulting in board space reduction by up to 60%.

- In October 2025, TSMC introduced Direct-to-Silicon Liquid Cooling Integrated on CoWoS Platform, which addresses thermal challenges associated with HPC and AI applications. The innovation enables higher power densities, improved thermal efficiency, and enhanced performance for AI accelerators and high-bandwidth memory (HBM)-based processors while supporting next-generation multi-die architectures.

- In February 2025, NVIDIA scaled its CoWoS orders from TSMC owing to the strong demand for Blackwell architecture GPUs of NVIDIA. The company secured approximately 70% of TSMC's CoWoS-L advanced packaging capacity for 2025, with total annual shipments expected to surpass 2 million units.