Market Definition

The market comprises advanced nuclear imaging systems and specialized radiotracers that visualize metabolic processes to detect pathology at the molecular level. These hybrid modalities include PET/CT and PET/MRI and are used in pcritical diagnostic and monitoring workflows across oncology, cardiology, and neurology by enabling precision, non-invasive, early-stage disease identification.

Sustained market growth supported by the global shift toward value-based care, increasing demand for accurate disease staging. It is further fueled by the expanding adoption of novel biomarkers and high-sensitivity scanners in hospitals and diagnostic centers.

Positron Emission Tomography Market Overview

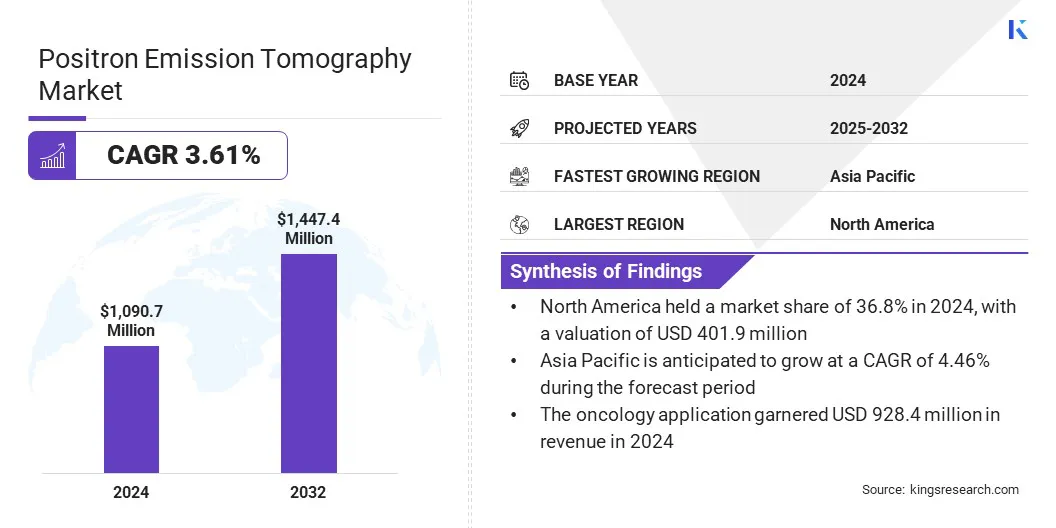

The global positron emission tomography market size was valued at USD 1090.7 million in 2024 and is projected to grow from USD 1130.0 million in 2025 to USD 1447.4 million by 2032, exhibiting a CAGR of 3.61% during the forecast period.

The increase in cancer and cardiovascular diseases, coupled with the expansion of precision diagnostics, is accelerating adoption of positron emission tomography systems. Additionally, rising hospital investments, radiotracer innovation, and growing oncology and cardiology applications are creating potential growth opportunities.

Major companies operating in the positron emission tomography industry are GE HealthCare, Siemens Healthineers AG, Philips, Canon Medical Systems Corp., United Imaging Healthcare Co. Ltd., Mediso Ltd., CMR Naviscan Corporation, Bruker Corporation, Positron Corporation, Agfa HealthCare NV, Segami Corporation, SOFIE Biosciences, Iorporation, SOFIE Biosciences, Inc., Eckert & Ziegler Strlzg AG, and Neusoft Medical Systems Co. Ltd..

The accelerating adoption of precision medicine fueled by breakthroughs in novel radiotracers and the emergence of theranostics acts as a significant driver for market growth. As clinical workflows integrate specialized isotopes such as Gallium-68 and Zirconium-89, diagnostic centers can offer superior specificity in oncology and neurology applications compared to traditional modalities.

This technological evolution enables accurate disease staging, directly influencing treatment efficacy and cost-containment strategies. Consequently, the push for value-based care is incentivizing substantial investment in next-generation positron emission tomography (PET) systems to support these advanced diagnostic capabilities.

- In November 2025, GE HealthCare received the CE mark for its Omni 128cm total body PET/CT system, a critical advancement in high-sensitivity molecular imaging. This milestone enables head-to-thigh imaging in a single bed position, significantly reducing scan times and radiation doses while optimizing clinical workflows for oncology and pediatric patients.

Key Highlights:

- The positron emission tomography industry size was recorded at USD 1090.7 million in 2024.

- The market is projected to grow at a CAGR of 3.61% from 2025 to 2032.

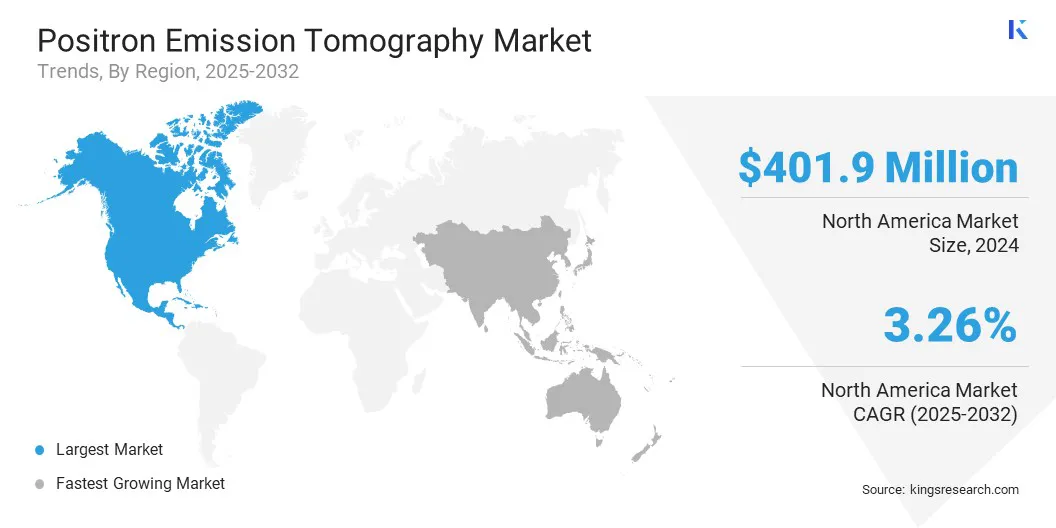

- North America held a share of 36.8% in 2024, valued at USD 401.9 million.

- The full-ring pet scanners segment garnered USD 899.2 million in revenue in 2024.

- The PET/CT modality segment accounted for a valuation of USD 918.2 million in 2024.

- The 18F-Fluorodeoxyglucose (18F-FDG) segment is anticipated to witness the fastest CAGR of 3.28% during the forecast period.

- The oncology segment held a share of 85.1% in 2024, valued at USD 928.4 million.

- The hospitals segment is expected to reach 765.7 million by 2032.

- Asia Pacific is anticipated to grow at a CAGR of 4.5% over the forecast period.

How advancements in digital scanning technology and the growing demand for hybrid imaging modalities are fueling market expansion?

The commercialization of digital PET and total-body scanners offer superior sensitivity compared to traditional analog systems, which is leading to widespread adoption. Reductions in scan time and radiotracer dose enable higher daily exam volumes and better utilization of high-value PET systems, strengthening operational ROI for imaging providers.

This shift is further accelerated by the integration of hybrid PET/MRI modalities, which minimize radiation exposure, making them critical for pediatric and longitudinal studies. Consequently, healthcare providers are prioritizing capital expenditure on these high-efficiency systems to optimize clinical workflows and expand diagnostic service lines.

- In December 2024, Siemens Healthineers acquired Advanced Accelerator Applications Molecular Imaging from Novartis, adding 13 European manufacturing sites to its PETNET network. The acquisition expands Siemens’ radiopharmaceutical production and distribution capacity, including 18F-FDG, improving supply access for oncology and neurology diagnostics.

How do high capital expenditure and radiotracer supply chain constraints hinder the growth of the positron emission tomography market?

The substantial capital expenditure required for acquiring hybrid modalities, particularly PET/CT and PET/MRI systems, represents a primary barrier to market scalability. Diagnostic centers face compounded difficulties managing the logistical constraints of short-lived radiotracers, such as 18F-FDG and 68Ga-based agents, alongside stringent regulatory compliance for radioactive materials.

These financial and operational hurdles restrict procurement capabilities in cost-sensitive healthcare segments. Consequently, this infrastructural challenge hinders the widespread application of molecular imaging in oncology and neurology, slowing the long-term adoption of precision diagnostics.

To address financial barriers, manufacturers are prioritizing cost-efficient partial-ring scanner designs and implementing managed service financing models to reduce upfront capital expenditure. The expansion of decentralized cyclotron networks streamlines the distribution of 18F-FDG and 68Ga-based tracers, mitigating supply chain risks.

Simultaneously, embedding AI-driven workflow automation into PET/CT systems maximizes patient throughput, improving economic viability for diagnostic imaging centers and fostering long-term adoption in oncology.

How is the integration of hybrid imaging modalities and AI-driven reconstruction improving diagnostic precision and operational throughput in PET?

The positron emission tomography market is witnessing a notable shift toward hybrid imaging, integrating PET/MRI and PET/CT modalities to elevate diagnostic granularity. This progression enables healthcare providers to utilize radiotracers such as 68Ga for precise theranostic applications in oncology. Furthermore, the incorporation of AI-driven reconstruction algorithms optimizes scan durations, thereby enhancing operational throughput for hospitals and maximizing revenue potential.

- In January 2025, Positron Corporation introduced the NeuSight PET-CT, a cost-effective 64-slice hybrid system positioned to accelerate adoption in emerging and value-tier markets. The platform supports oncology and cardiac PET applications at a lower price point, enabling high-volume imaging centers to increase throughput and strengthen unit economics while maintaining diagnostic performance.

Positron Emission Tomography Market Report Snapshot

|

Segmentation

|

Details

|

|

By Product Type

|

Full-Ring PET Scanners, Partial-Ring PET Scanners

|

|

By Modality

|

Stand-Alone PET, PET/CT, PET/MRI

|

|

By Radiotracer / Isotope

|

18F-Fluorodeoxyglucose (18F-FDG), 68Ga-Based Tracers (DOTATATE, PSMA), 82Rb & 13N-Ammonia (Cardiac), 64Cu & Zirconium-89 Immuno-PET

|

|

By Application

|

Oncology, Cardiology, Neurology, Inflammation, Others

|

|

By End-User

|

Hospitals, Diagnostic Imaging Centers, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Product Type (Full-Ring PET Scanners and Partial-Ring PET Scanners): The full-ring PET scanners segment earned USD 899.2 million in 2024, mainly driven by increased oncology screening demand and technological advancements in image resolution.

- By Modality (Stand-Alone PET, PET/CT, and PET/MRI): The PET/MRI segment held a 13.55% market share in 2024, fueled by superior soft-tissue contrast and reduced ionizing radiation exposure.

- By Radiotracer/Isotope (18F-Fluorodeoxyglucose (18F-FDG), 68Ga-Based Tracers (DOTATATE, PSMA), 82Rb & 13N-Ammonia (Cardiac), and 64Cu & Zirconium-89 Immuno-PET): The 68Ga-Based Tracers (DOTATATE, PSMA) segment is projected to reach USD 150.7 million by 2032, supported by expanding theranostic applications and favorable reimbursement shifts for neuroendocrine and prostate cancer imaging.

- By Application (Oncology, Cardiology, Neurology, Inflammation, and Other): The oncology segment held a share of 85.1% in 2024, propelled by rising cancer incidence and the importance of PET in early diagnosis and treatment monitoring.

- By End-User (Hospitals, Diagnostic Imaging Centers, and Others): The diagnostic imaging centers segment is projected to reach USD 573.5 million by 2032, owing to increasing outpatient service demand and enhanced cost-efficiencies compared to traditional hospital-based settings

What is the market scenario in North America and the Asia Pacific region?

Based on region, the positron emission tomography market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

North America positron emission tomography market held a share of 36.8% in 2024, valued at USD 401.9 million. This position reflects the region’s advanced healthcare infrastructure and early adoption of hybrid imaging modalities such as PET/CT.

Rising oncological and neurological diseases continues to elevate demand for high-precision diagnostics, supporting growth in full-ring PET scanner deployments. Moreover, substantial capital allocation toward modernizing diagnostic centers and the presence of key industry players reinforce the region’s market position.

- In October 2024, Positron Corporation secured an agreement to provide three NeuSight PET/CT 64-slice scanners to a leading cardiovascular diagnostic, management, and treatment practice. This expansion of the PET/CT modality enhances clinical diagnostics and accessibility, offering significant growth opportunities through high-performance imaging solutions in the molecular imaging industry.

The Asia-Pacific positron emission tomography industry is set to grow at a CAGR of 4.5% over the forecast period. This expansion is propelled by rapid economic development and increasing healthcare expenditure across key economies such as China and India.

Government initiatives aimed at improving cancer care infrastructure are also stimulating the demand for cost-effective, high-performance imaging solutions. Additionally, the increase in the geriatric population and the modernization of hospital frameworks by local healthcare providers are catalyzing the broad uptake of positron emission tomography solutions in the long term.

- In May 2025, Mahajan Imaging and Labs introduced the 128-slice digital PET-CT Omni Legend scanner in India. The system reduces radiation exposure by 60%, offers 1.4 mm spatial resolution for earlier cancer detection, and leverages AI to enhance lesion identification and accelerate scanning.

Regulatory Frameworks

- The U.S. regulates positron emission tomography systems through the FDA, covering device approval, radiopharmaceutical safety, clinical validation, and manufacturing compliance under medical device and nuclear medicine regulations.

- In the EU, the EMA and national competent authorities oversee positron emission tomography radiopharmaceuticals, while imaging systems comply with the medical device regulation, ensuring safety, performance, and post-market surveillance requirements.

- In APAC, China regulates positron emission tomography scanners and radiotracers through the NMPA, enforcing strict approval pathways, clinical evidence requirements, and radiation safety standards for nuclear imaging facilities.

- Japan governs the PET market through the PMDA, regulating imaging equipment and radiopharmaceuticals under pharmaceutical and medical device laws, with strong emphasis on quality, radiation exposure control, and clinical efficacy.

- Globally, the International Atomic Energy Agency (IAEA), , often in collaboration with the World Health Organization (WHO), establishes the standard for radiation safety, clinical use standards, and ethical practices for positron emission tomography, supporting harmonization while allowing region-specific regulatory implementation.

Competitive Landscape

The positron emission tomography industry is highly competitive and fragmented, featuring players ranging from established corporations to emerging vendors. Major participants such as GE HealthCare, Siemens Healthineers AG, and Philips leverage extensive imaging ecosystems to offer scalable solutions.

Meanwhile, players comprising United Imaging Healthcare Co. Ltd., Mediso Ltd., and Bruker Corporation emphasize high-performance clinical capabilities. This diverse landscape fosters rapid innovation, strategic partnerships, and continuous product developments.

- In August 2025, Positron Corporation secured a multi-unit sale of its NeuSight 64-slice PET-CT systemsto U.S. based nuclear cardiology group specializing in advanced cardiovascular diagnostics and interventional care. The agreement strengthens clinical capacity in nuclear cardiology and accelerates the adoption of cost-effective, high-resolution hybrid imaging solutions for advanced cardiovascular diagnostics.

Key Companies in Positron Emission Tomography Market:

- GE HealthCare

- Siemens Healthineers AG

- Koninklijke Philips N.V.,Canon Medical Systems Corp.

- United Imaging Healthcare Co. Ltd.

- Mediso Ltd.

- CMR Naviscan Corporation

- Bruker

- Positron Corporation

- SOFIE Co.

- Neusoft Medical Systems Co. Ltd.

- Hitachi Ltd.

- Oncovision

- MinFound Medical Systems Co., Ltd

- MR Solutions Ltd.

Recent Developments

- In October 2025, Positron Corporation secured the Innovation Award for its PET-CT systems, recognized for enhancing clinical accessibility and diagnostic efficiency. This recognition addresses high capital barriers, offering affordable, high-throughput hybrid imaging solutions across oncology and cardiology.

- In November 2024, Positron Corporation partnered with Upbeat Cardiology Solutions to offer turnkey PET-CT leasing and clinical services. This initiative aims to lower capital barriers for private practices, fueling global adoption of hybrid imaging and high-throughput diagnostics within the growing cardiovascular imaging segment.

- In July 2022, Canon Medical Systems USA acquired NXC Imaging to expand its U.S. Upper Midwest footprint. This move strengthens sales of full-ring PET/CT scanners and 18F-FDG isotopes, optimizing regional access to oncology diagnostics and positioning Canon to capture rising demand for hybrid PET/MRI systems.