Market Definition

The market involves technologies that generate electricity by recovering low- to high-temperature waste heat from industrial operations using organic rankine cycle systems. The market includes systems operating across varied capacity and temperature ranges, deployed in manufacturing facilities, refineries, petrochemical plants, and waste incineration units.

ORC Waste Heat to Power Market Overview

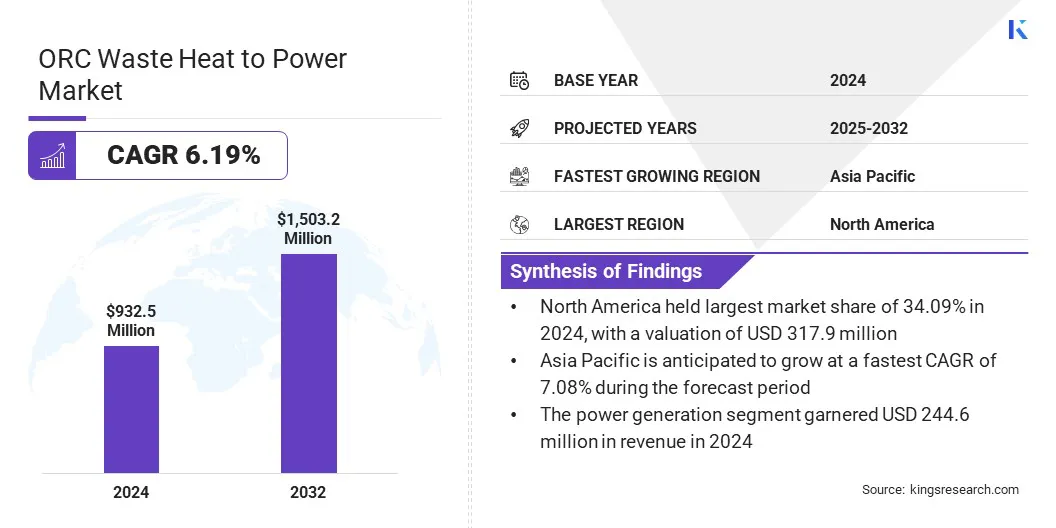

The global ORC waste heat to power market size was valued at USD 932.5 million in 2024 and is projected to grow from USD 987.3 million in 2025 to USD 1,503.2 million by 2032, exhibiting a CAGR of 6.19% over the forecast period. This growth is supported by the expansion of energy-intensive industries seeking efficient waste heat recovery solutions amid rising energy costs.

Increasing adoption of ORC systems in oil and gas processing facilities reflects rising demand for technologies that convert continuous process heat into electricity to improve operational stability. This efficiency-driven adoption gains momentum as operators pursue structured energy recovery solutions to reduce power costs and ensure uninterrupted processing.

Key Market Highlights:

- The ORC waste heat to power industry was recorded at USD 932.5 million in 2024.

- The market is projected to grow at a CAGR of 6.19% from 2025 to 2032.

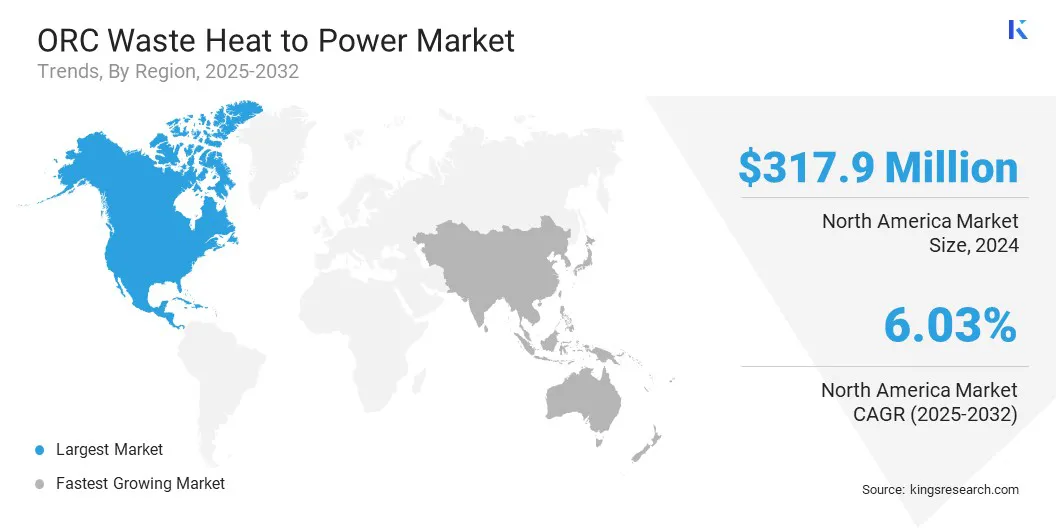

- North America held a share of 34.09% in 2024, valued at USD 317.9 million.

- The 1–5 MW segment garnered USD 360.1 million in revenue in 2024.

- The below 150°C segment is expected to reach USD 627.2 million by 2032.

- The industrial processes segment is anticipated to witness the fastest CAGR of 6.62% over the forecast period.

- Asia Pacific is anticipated to grow at a CAGR of 7.08% through the projection period.

Major companies operating in the ORC waste heat to power market are ALFA LAVAL, Mitsubishi Heavy Industries, Ltd. (Turboden S.p.A.), E.ON SE, ENOGIA, Siemens AG, BE Petrothai Group, ORCAN ENERGY AG, EXERGY INTERNATIONAL SRL, Climeon, AURA GmbH & Co. KG, Thermax Limited, Ormat, Triogen, BITZER Kühlmaschinenbau GmbH, and INTEC Engineering GmbH.

ORC units perform reliably across upstream and downstream operations where heat availability remains stable. System integration enhances performance visibility and supports compliance with energy management standards.

- In October 2025, Turboden S.p.A., a Mitsubishi Heavy Industries Group company, announced the commissioning of North America’s first waste heat to power project in a steam-assisted gravity drainage facility. The ORC installation converts recovered heat into carbon-free electricity, offsetting a significant portion of grid consumption and strengthening Turboden’s position in high-temperature industrial applications.

How Is Industrial Waste Heat Utilization Accelerating ORC Adoption?

Rising industrial focus on waste heat utilization to reduce energy costs is driving structured recovery of unused thermal energy across energy-intensive facilities. Manufacturers are increasingly prioritizing predictable, measurable, and reliable waste heat recovery solutions to lower dependence on grid-based power and stabilize long-term energy expenditures.

ORC systems address this need by enabling scalable power generation across varied temperature ranges while delivering consistent performance. Their ability to integrate with existing industrial processes supports continuous energy recovery without disrupting operations. Ongoing advancements in ORC equipment efficiency and system control further enhance reliability, reinforcing adoption as part of long-term industrial energy optimization strategies.

- In November 2024, Exergy International announced an agreement with Maren Maraş Elektrik Üretim A.Ş. for supplying two geothermal power plants in the Aydın region in Turkey.

What factors create financial barriers to industrial ORC adoption?

High upfront capital requirements create a major financial barrier to ORC implementation in industrial facilities. Project costs include specialized equipment, engineering design, system integration, and site-specific customization, which increase initial investment levels. These constraints are more visible in capital-constrained facilities, where long payback periods affect investment priorities and slow adoption.

Industrial operators, therefore evaluate ORC projects selectively, focusing on sites with stable and predictable waste heat availability that can support long-term financial commitments.

To reduce these barriers, organizations are adopting phased investment approaches and strengthening project-financing structures. Companies are also exploring leasing and third-party ownership models to lower initial capital pressure. Pilot projects and performance-based deployments are improving financial clarity and supporting gradual, scalable ORC system adoption.

How is wider integration of ORC systems across heavy industries driving market growth?

Broader integration of ORC systems across heavy industries such as cement manufacturing, steel production, glass processing, and petrochemicals is supporting market growth, as these sectors operate with continuous and high-grade thermal loads suitable for waste heat recovery. Industrial operators are deploying ORC units to convert unused process heat into electricity, improving energy efficiency and lowering dependence on grid power.

Adoption is strongest in facilities with stable heat availability that enables predictable power generation and long-term planning. Rising electricity costs and energy intensity further encourage integration of ORC systems to strengthen operational resilience and support cost control across energy-intensive production environments.

- In November 2025, Orcan Energy announced it aims to use Howden’s high-efficiency turbo-expander technology in its industrial waste-heat-to-electricity systems to improve power generation performance. The collaboration targets the conversion of large-scale industrial waste heat into clean electricity, increasing overall energy recovery and reducing emissions from heat-intensive processes.

ORC Waste Heat to Power Market Report Snapshot

|

Segmentation

|

Details

|

|

By Capacity

|

Below 1 MW, 1–5 MW, Above 5 MW

|

|

By Temperature

|

Below 150°C, 150 - 350°C, Above 350°C

|

|

By Application

|

Power Generation, Industrial Processes, Oil & Gas and Petrochemicals, Waste Incineration & MSW Plants, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Capacity (Below 1 MW, 1–5 MW, and Above 5 MW): The 1–5 MW segment generated USD 360.1 million in 2024, mainly due to strong deployment in industrial facilities requiring mid-scale heat recovery systems that balance installation feasibility and consistent electricity generation performance.

- By Temperature (Below 150°C, 150 - 350°C, and Above 350°C): The 150–350°C segment is poised to record a CAGR of 6.21% over the forecast period, propelled by the widespread suitability of this temperature range for ORC systems across diverse industrial processes requiring stable thermal conversion.

- By Application (Power Generation, Industrial Processes, Oil & Gas and Petrochemicals, Waste Incineration & MSW Plants, and Others): The power generation segment is estimated to hold a share of 26.26% by 2032, fueled by increased adoption of ORC units within facilities seeking reliable onsite electricity production and improved utilization of available thermal resources

What is the market scenario in North America and Asia Pacific region?

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

The North American ORC waste heat to power market share stood at 34.09% in 2024, valued at USD 317.9 million, supported by sustained deployment across energy-intensive industrial corridors. Market growth is driven by continuous thermal loads in industries such as cement, metals, chemicals, and refining, which enable predictable electricity generation from waste heat.

Industrial operators are increasingly implementing structured energy management programs to reduce grid dependence and manage long-term power costs, strengthening demand for ORC systems. Continued investments by manufacturers and utilities in industrial modernization and efficiency upgrades are further supporting the adoption by enabling the conversion of unused process heat into stable and measurable power output.

- In September 2025, Baker Hughes announced the design and supply of critical equipment for geothermal Organic Rankine Cycle power plants under Fervo’s Cape Station Phase II project. Upon commissioning, the five ORC units are expected to deliver roughly 300 megawatts of reliable power to the grid, supporting substantial residential electricity demand.

The Asia Pacific ORC waste heat to power industry is set to grow at a CAGR of 7.08% over the forecast period, driven by the rapid expansion of energy-intensive industries and rising interest in structured heat recovery solutions. Industrial facilities continue to scale capacity, creating stronger demand for technologies that convert surplus thermal energy into electricity.

Manufacturing clusters prioritize ORC systems for operational stability where heat availability remains consistent. Growth is also supported through increasing investments in process optimization and adoption of systems capable of operating across varied temperature conditions.

Regulatory Frameworks

- In the European Union, the Industrial Emissions Directive (IED) governs emission control standards for energy-intensive facilities. It establishes uniform environmental requirements that encourage the adoption of heat recovery technologies, including ORC systems, to improve thermal efficiency and reduce operational emissions.

- In the U.S., the Clean Air Act regulates air pollutant emissions from industrial sources. It encourages facilities to implement technologies that lower thermal losses and improve energy conversion efficiency, strengthening the relevance of ORC-based recovery systems.

- In China, the Industrial Energy Conservation Regulation supervises energy use standards across heavy industries. It reinforces demand for heat recovery systems by requiring optimization of thermal resources, thereby enhancing adoption prospects for ORC solutions.

- In Japan, the Energy Conservation Act enforces structured energy efficiency measures for industrial operators. It encourages the utilization of waste heat streams through compliant technologies, strengthening alignment between regulatory requirements and ORC system deployment.

Competitive Landscape

Key players in the ORC waste heat to power market are strengthening competitive positioning through strategies centered on scaling operations, expanding portfolios, and refining system performance.

Companies are developing ORC configurations suited to a wide range of temperature profiles and capacity needs, supporting deployment across diverse industrial settings. Market participants are expanding manufacturing and engineering capabilities to shorten delivery timelines and support rising demand.

- In June 2025, E.ON Energy Infrastructure Solutions and Orcan Energy jointly commissioned an ORC system at the Kristall-Glasfabrik Amberg production site. The installation enhances energy efficiency in glass manufacturing and supports emission reduction efforts. The facility produces approximately 23 million crystal and tableware glass units annually.

Key Companies in ORC Waste Heat to Power Market:

- ALFA LAVAL

- Mitsubishi Heavy Industries, Ltd. (Turboden S.p.A.)

- ON SE

- ENOGIA

- Siemens AG

- BE Petrothai Group

- ORCAN ENERGY AG

- EXERGY INTERNATIONAL SRL

- Climeon

- AURA GmbH & Co. KG

- Thermax Limited

- Ormat

- Triogen

- BITZER Kühlmaschinenbau GmbH

- INTEC Engineering GmbH

Recent Developments (Partnerships)

- In October 2025, Turboden America LLC announced the award of Phase II of the Cape Station geothermal project, expanding its collaboration with Fervo Energy. The phase includes supplying three 60-MWe ORC units, increasing total capacity, and supporting deployment of Fervo’s second-generation modular plant design at the Cape Station site.