Market Definition

The LNG (Liquefied Natural Gas) bunkering market refers to the global industry engaged in the supply and distribution of LNG as a marine fuel for ships and vessels. It combines infrastructure development, logistics, and storage solutions with the growing demand for environmentally sustainable maritime operations. These services allow shipping companies to minimize emissions, comply with more stringent environmental regulations, and maximize fuel efficiency while optimizing operational costs.

The integration and analysis of extensive logistical and operational data allow LNG bunkering providers to enhance supply chain management, improve delivery efficiency, and tailor services to specific port and vessel requirements.

LNG Bunkering Market Overview

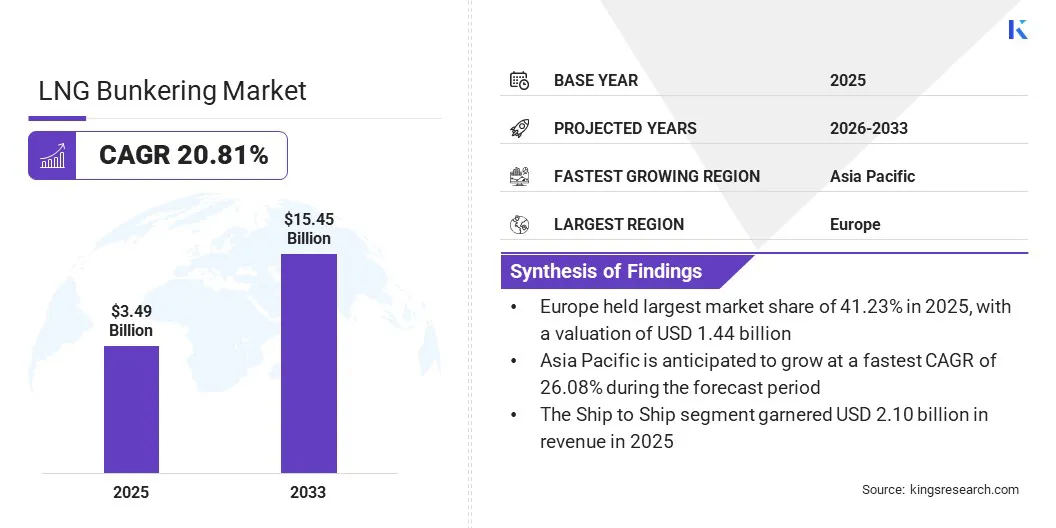

The global LNG bunkering market size was valued at USD 3.49 billion in 2025 and is projected to grow from USD 4.11 billion in 2026 to USD 15.45 billion by 2033, exhibiting a CAGR of 20.81% during the forecast period. This rapid expansion is fueled by stringent environmental regulations and the global shift toward cleaner marine fuel alternatives.

Major companies operating in the global LNG bunkering industry are Shell.com, TotalEnergies, Gasum Ltd, Exxon Mobil Corporation, ENGIE SA, Peninsula, Seaside LNG, KOREA LNG BUNKERING, Stabilis Solutions, Inc., Fluxys, Mitsui O.S.K Lines, Titan LNG, Petroliam Nasional Berhad (PETRONAS), Cryostar, and Crowley.

The increased implementation of LNG, along with emerging alternatives such as bio-LNG, is propelled by its low emissions profile, regulatory acceptance, and the need to decarbonize the shipping sector. Market growth is expected to gain further momentum in the coming years due to continued investment in infrastructure and advancements in technology.

- In October 2024, Bunker One launched its first physical LNG bunker supply service, marking a significant step in expanding its alternative fuel offerings. The initiative supports the decarbonization goals of the maritime sector by providing cleaner LNG fuel to shipping and strengthening Bunker One’s position in sustainable shipping solutions and the global energy transition.

Key Highlights

- The global LNG bunkering market size was USD 3.49 billion in 2025.

- The market is projected to grow at a CAGR of 20.81% from 2026 to 2033.

- Europe held a share of 41.23% in 2025, valued at USD 1.44 billion.

- The ship to ship segment garnered USD 2.10 billion in revenue in 2025.

- The container fleet segment is expected to reach USD 6.77 billion by 2033.

- Asia Pacific is anticipated to grow at a CAGR of 26.08% through the projection period.

How is the expansion of bunkering infrastructure fueling market growth?

The expansion of LNG bunkering infrastructure is an important driver of the development of the LNG bunkering market. The availability and reliability of supply are also increasing with the growing number of ports worldwide investing in specialized storage, distribution, and refueling activities. Such innovations reduce logistical problems and allow shipping companies to transition to the use of LNG as a marine fuel.

An established system of bunkering centers improves confidence in the supply of LNG and helps vessel operators to conduct their operations more efficiently and cost-effectively. This increased infrastructure is making LNG a viable and attractive option within the maritime sector, supporting the adoption of cleaner fuel options.

- In October 2024, TotalEnergies revealed plans to expand its global LNG (liquefied natural gas) bunkering services by signing new contracts to supply them and developing infrastructure. This program aims to improve LNG bunkering capabilities at major ports in Europe, Asia, and the Middle East. The business plan will support the decarbonization of the shipping sector by providing a cleaner alternative to conventional marine fuels, thus enhancing supply chain efficiency.

How does limited port infrastructure affect the expansion and accessibility of the LNG bunkering market?

Limited port infrastructure is a major obstacle to the widespread adoption of LNG bunkering in the maritime industry. There are currently few ports in the world that have dedicated LNG bunkering stations, which creates significant geographic supply gaps. This limits the operational flexibility of LNG-powered vessels, particularly on shipping routes that lack access to suitable ports.

This leads to logistical problems and higher costs for shipping companies, particularly in terms of route planning and fuel stops. Infrastructure deficiencies also hinder the development of the industry, since investments in LNG-driven vessels are dependent on the availability of good bunkering facilities.

To address this challenge, stakeholders are investing more in the development and expansion of LNG infrastructure in major ports across the globe. Moreover, the establishment of global standards and safety measures can help accelerate the adoption of LNG bunkering systems while ensuring safe and efficient operations.

How is the integration of bio-LNG and synthetic LNG positively influencing the LNG bunkering market?

One of the key market trends is the incorporation of bio-LNG and synthetic LNG into existing supply chains. Bio-LNG, produced from renewable biomass, and synthetic LNG, derived from renewable electricity and captured carbon, can further reduce the carbon footprint of marine transport. With this integration, shipping companies can comply with an ever-growing number of strict environmental standards and be in line with the global decarbonization objectives.

The substitution or mixing of traditional LNG with bio-LNG and synthetic LNG provides a flexible route through which the industry can evolve into a carbon-neutral shipping industry. With the ongoing increase in demand for viable solutions, the production, certification, and supply of these alternative fuels are likely to influence the market.

- In April 2026, Kawasaki Kisen Kaisha, Ltd. (“K” Line) started operating ISCC-EU certified carbon-neutral bio-LNG fuel on its LNG-powered car carriers under a long-term procurement contract. This project is expected to assist in reducing greenhouse gas emissions by about 60,800 tons annually and support the achievement of the 2050 net-zero emissions target and overall decarbonization goals.

LNG Bunkering Market Report Snapshot

|

Segmentation

|

Details

|

|

By Product Type

|

Truck to Ship, Port to Ship, Ship to Ship, and Portable Tanks

|

|

By Application

|

Container Fleet, Tanker Fleet, Cargo Fleet, Ferries, Inland Vessels, and Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Product Type (Truck to Ship, Port to Ship, Ship to Ship, and Portable Tanks): The ship to ship segment earned USD 2.10 billion in 2025, mainly because of its operational effectiveness and ability to transfer large amounts of LNG between vessels at sea or in port. This process reduces downtime and enhances flexibility in fueling schedules, which is particularly appealing to shipping companies with short turnaround times. Moreover, ship to ship bunkering supports the sustained operations of larger fleets, contributing to its robust revenue growth.

- By Application (Container Fleet, Tanker Fleet, Cargo Fleet, Ferries, Inland Vessels, and Others): The container fleet segment held a share of 39.33% of the market in 2025, as it demanded LNG as a cleaner marine fuel amid tightening emission regulations. This was further reinforced by the growth of global containerized trade and the adoption of LNG-powered vessels by the largest shipping companies. Container fleets are also highly favored due to the cost-effectiveness and environmental benefits of LNG, which contribute to their major role.

What is the market scenario in Europe and Asia Pacific?

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Europe LNG bunkering market share stood at 41.23% in 2025, valued at USD 1.44 billion. This leadership is facilitated by stringent regulatory standards and significant port infrastructure investments. The growth of bunkering infrastructure in major ports has made it more efficient to supply fuel to LNG-powered vessels, thereby boosting the use of LNG as a marine fuel.

The collaboration between government agencies, port authorities, and industrial stakeholders has simplified the working processes and increased the reliability of the supply chain. The incorporation of alternative fuels, including bio-LNG, is also underway, which indicates ongoing efforts to reduce emissions in maritime transportation. These factors are expected to sustain Europe’s leading position in the LNG bunkering industry over the forecast period.

- In March 2026, Anew Climate and Avenir fulfilled their first joint bio-LNG bunkering in Europe. This achievement indicates the potential of bio-LNG as a sustainable marine fuel that can support the shipping industry in transitioning to lower-carbon solutions, as well as the efforts of both companies to decarbonize and innovate maritime transport with improved environmental performance.

The Asia Pacific LNG bunkering market is set to grow at a CAGR of 26.08% over the forecast period. This growth is propelled by the rising number of LNG-powered vessels, ongoing port infrastructure development, and regulatory efforts to reduce maritime emissions. Several countries are actively developing LNG bunkering hubs to support international shipping routes and regional trade.

The introduction of modern technologies and the development of non-routine refueling options are enhancing operational efficiency and supply reliability. Strategic partnerships between public and private sector entities are facilitating rapid market development. These efforts are transforming Asia Pacific into a high-growth market for LNG bunkering services, contributing to the increased usage of cleaner marine fuel in the region.

- In March 2023, NYK and FueLNG completed the first LNG bunkering in Singapore of a pure car and truck carrier vessel. This achievement contributed to NYK’s objective of becoming a net-zero greenhouse gas emitter by the year 2050 and to FueLNG’s efforts to promote LNG as a marine fuel under Singapore’s strict safety regulations.

Regulatory Frameworks

- In the U.S., the US Coast Guard (USCG) regulations for LNG bunkering establish the standards and procedures for LNG fueling operations. These regulations ensure safe and reliable LNG bunkering practices, promoting operational safety.

- In the international context, ISO 20519:2021 regulates the bunkering of liquefied natural gas (LNG) fueled vessels. It specifies requirements for safe, reliable, and environmentally responsible LNG bunkering procedures for ships and marine technology. This standard supports the global maritime industry by enabling LNG adoption as a cleaner fuel and enhancing uniform safety and operational standards across the shipping sector.

Competitive Landscape

Both established energy providers and new entrants in the LNG bunkering market are investing in the development of strong infrastructure and the reliability of their services. Market players are also forming strategic alliances, adopting the latest state-of-the-art technologies, and enhancing operational efficiency to strengthen their competitive position.

The differentiation is being made more with innovative solutions, flexible service offerings, and a dedication to safety and sustainability. As the industry matures, competition is likely to increase, and further improvements in supply chain management, customer support, and the incorporation of alternative fuels within the LNG bunkering value chain are expected.

- In March 2025, Anglo-Eastern introduced an advanced maritime training LNG/ammonia bunkering station skid. This training skid was created in collaboration with major manufacturers and is intended to increase the competence and safety of crews working with alternative marine fuels. This project is in line with the maritime industry’s transition toward cleaner energy sources and reflects Anglo-Eastern’s commitment to environmental sustainability and enhanced training standards.

Key Companies In The LNG Bunkering Market

Recent Developments (Partnerships/Agreements/Joint Venture)

- In July 2025, TotalEnergies and CMA CGM launched a joint venture focused on LNG bunkering logistics. The partnership supplies liquefied natural gas to vessels and expands LNG supply infrastructure. Their combined expertise in the energy and shipping sectors helps decarbonize the maritime sector and promote cleaner fuels within the international shipping community.

- In March 2026, Stolt-Nielsen and NYK Line established a strategic joint venture in Avenir LNG, with NYK acquiring a 50-percent stake. This joint venture enhances the presence of both companies in small-scale LNG and LNG bunkering and helps the maritime sector shift toward LNG and bio-LNG fuels, promoting global sustainability.

- In January 2026, Galveston LNG Bunker Port announced a strategic partnership with TOTE Services to advance the LNG bunker vessel fleet on the U.S. Gulf Coast. The purpose of this partnership is to expand LNG bunkering facilities, improve the reliability of fuel supplies, and enable the maritime industry in the region to achieve sustainability and emissions reduction objectives.

- In October 2023, Seaspan and AES agreed on a Memorandum of Understanding to jointly develop the LNG bunkering business. The collaboration is intended to expand LNG bunkering facilities and services, facilitate the adoption of cleaner marine fuels, and help decarbonize the shipping sector in North America and the rest of the world.