Market Definition

The green steel market involves the production, distribution, and commercialization of steel made using environmentally sustainable methods. This means minimizing or eliminating carbon emissions by using alternative energy sources like hydrogen, renewable electricity, or carbon capture technologies, as opposed to traditional coal-based processes. The market comprises products, technologies, services, and supply chains that are centered on reducing the environmental impact of steel production.

Green Steel Market Overview

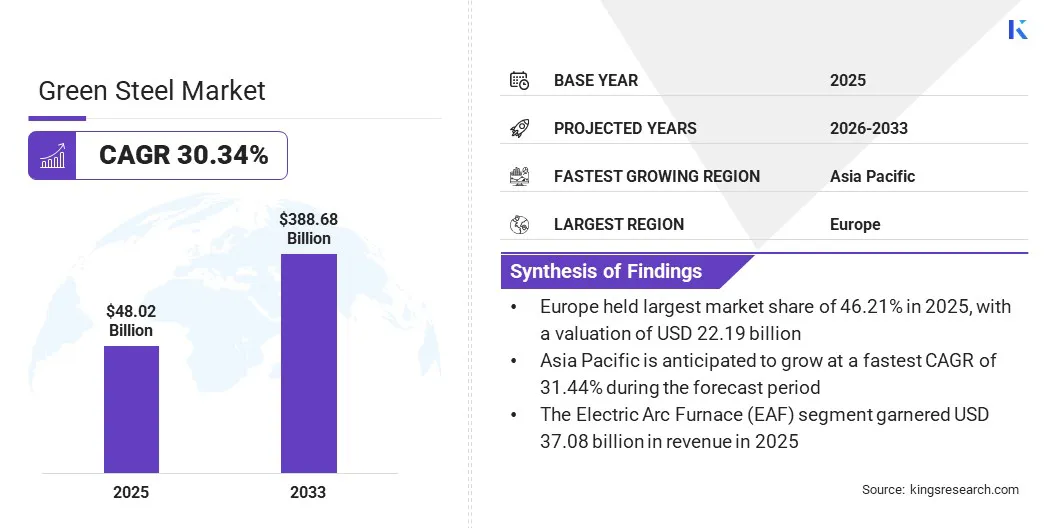

The global green steel market size was valued at USD 48.02 billion in 2025 and is projected to grow from USD 60.83 billion in 2026 to USD 388.68 billion by 2033, exhibiting a CAGR of 30.34% during the forecast period. The market is witnessing rapid growth, mainly driven by the increasing demand for environmentally responsible construction materials, sustainable automotive manufacturing, and cleaner industrial supply chains.

Major companies operating in the global green steel market are Nucor Corporation, ArcelorMittal, SSAB, Stegra AB, Tata Steel, NIPPON STEEL CORPORATION, Salzgitter AG, JFE Steel Corporation, voestalpine AG, JSW Group, LIBERTY Steel Group, Outokumpu, HBIS GROUP, SSG, and EMSTEEL.

Investments in renewable energy infrastructure, green hydrogen production, and next-generation steelmaking technologies are speeding up the commercialization of low-carbon steel production globally. Major steel producers are moving from pilot projects to commercial-scale deployments, and downstream industries are including green steel in their procurement plans to meet ESG commitments and regulatory requirements.

- In December 2024, Volkswagen Group and Thyssenkrupp Steel signed an MOU for the supply of green steel, specifically low-carbon bluemint Steel, from a future direct reduction plant. The partnership supports Volkswagen’s decarbonization and electromobility goals by introducing sustainable green steel solutions to the automotive value chain.

Key Market Highlights

- The global green steel market size was valued at USD 48.02 billion in 2025.

- The market is projected to grow at a CAGR of 30.34% from 2026 to 2033.

- Europe held a share of 46.21% in 2025, with a valuation of USD 22.19 billion.

- The electric arc furnace (EAF) segment garnered USD 37.08 billion in revenue in 2025.

- The renewable energy segment is expected to reach USD 289.73 billion by 2033.

- The specialty steel segment is anticipated to witness the fastest CAGR of 31.87% over the forecast period.

- The building & construction segment garnered USD 25.10 billion in revenue in 2025.

- Asia Pacific is anticipated to grow at a CAGR of 31.44% through the projection period.

How is the growing demand for sustainable construction and automotive materials driving market expansion?

The growing focus on sustainability in the construction and automotive industries is propelling the demand for green steel. Builders, contractors, and infrastructure companies are seeking low-carbon materials to minimize the environmental impact of buildings and major projects, and to comply with ever-tightening environmental regulations.

Similarly, automotive manufacturers are under growing pressure to reduce emissions across their entire value chain. While the electrification process is addressing vehicle emissions, minimizing embedded carbon in manufacturing processes has become equally important. Green steel allows automakers to significantly reduce Scope 3 emissions while providing structural integrity, durability, and performance.

- In June 2024, Volkswagen AG and Vulcan Green Steel announced a partnership to supply low-carbon green steel. The agreement supports Volkswagen’s decarbonization and sustainability goals by integrating green steel into its supply chain, furthering efforts to reduce emissions in automotive manufacturing and promote environmentally responsible mobility solutions.

How do the high cost of production and infrastructure constraints hinder the growth of the green steel market?

Green steel production, while environmentally beneficial, is considerably more expensive than conventional steelmaking. Hydrogen-based direct reduction, or electric arc furnaces (EAF) running on renewable energy, requires high capital costs, advanced infrastructure, and the availability of inexpensive renewable energy. The widespread availability and affordability of green hydrogen are also major hurdles, particularly in areas where infrastructure for its production is still at an early stage of development.

To overcome this challenge, industry leaders are investing in upgrading facilities or developing new production lines, increasing investments in research and development, forming strategic alliances, and advocating for supportive government policies and incentives. Production volumes are expected to grow, with costs expected to decrease over time as technology advances.

How is the rapid advancement and adoption of Hydrogen DRI-EAF technology impacting the development of the green steel market?

One of the major trends in the green steel industry is the fast-developing Hydrogen Direct Reduced Iron (H-DRI) with Electric Arc Furnace (EAF) technology, which substitutes coal with hydrogen in the reduction of iron, significantly reducing carbon emissions without sacrificing production efficiency benefits. The cost competitiveness of the hydrogen-based steelmaking route is expected to further improve as the price of renewable energy drops and green hydrogen production increases, thereby enabling broader commercial adoption.

Major steelmakers are heavily investing in pilot projects and scaling such technologies to achieve commercial viability. The push for Hydrogen DRI-EAF aligns with global decarbonization goals and is garnering heavy investments and strategic partnerships, setting higher standards for sustainable steelmaking.

- In May 2024, LIBERTY Primary Metals Australia completed magnetite testing for hydrogen-based DRI-EAF green steel production in Whyalla. The high-grade magnetite was determined to be superior to reference materials, enabling the final design of LIBERTY’s integrated green steel plant, powered by renewable energy, which is expected to be operational by 2027.

Green Steel Market Report Snapshot

|

Segmentation

|

Details

|

|

By Production Technology

|

Electric Arc Furnace (EAF) (Scrap-Based/Renewable Power), Hydrogen-Based Direct Reduction (H-DRI), and Others

|

|

By Energy Source

|

Renewable Energy (Solar/Wind/Hydropower), Green Hydrogen, Sustainable Biomass, and Others

|

|

By Product Form

|

Flat Steel, Long Steel, Tubular Steel, and Specialty Steel

|

|

By End User

|

Building & Construction, Automotive & Transportation, Consumer Goods & Appliances, Energy & Power Infrastructure, Machinery & Industrial Equipment, Packaging, and Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Production Technology (Electric Arc Furnace (EAF) (Scrap-Based/Renewable Power), Hydrogen-Based Direct Reduction (H-DRI), and Others): The electric arc furnace (EAF) segment earned USD 37.08 billion in 2025, due to its capacity to use recycled scrap steel and renewable electricity. This growth is further supported by the rising number of commercial-scale projects across the globe.

- By Energy Source (Renewable Energy (Solar/Wind/Hydropower), Green Hydrogen, Sustainable Biomass, and Others): The renewable energy segment held a share of 75.22% in 2025, owing to its easy accessibility, declining prices, and the ability to power electric arc furnaces with low carbon emissions. The increased focus on decarbonization in the steel industry has led producers to adopt solar, wind, and hydropower in their operations, reinforcing segmental dominance.

- By Product Form (Flat Steel, Long Steel, Tubular Steel, and Specialty Steel): The flat steel segment is projected to reach USD 243.12 billion by 2033, fueled by its extensive use in automotive manufacturing, construction, shipbuilding, and industrial equipment. The rising demand for green flat steel is further driven by the surging demand for sustainable building materials and lightweight vehicle parts, as manufacturers are emphasizing eco-friendly materials for large-scale industrial applications.

- By End User (Building & Construction, Automotive & Transportation, Consumer Goods & Appliances, Energy & Power Infrastructure, Machinery & Industrial Equipment, Packaging, and Others): The automotive & transportation segment is anticipated to grow at a CAGR of 32.37% over the forecast period, driven by the industry's shift toward lightweight and sustainable materials to meet stringent emission standards. Increased adoption of electric vehicles and rising pressure from regulators and consumers for greener supply chains are accelerating the demand for green steel in car manufacturing and transportation infrastructure.

What is the market scenario in Europe and Asia Pacific?

Based on region, the global green steel market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

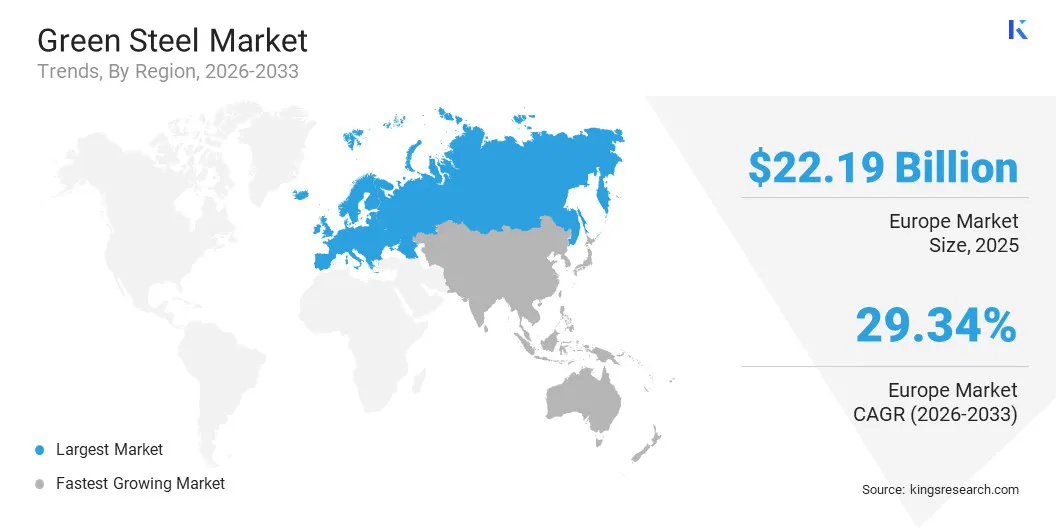

The Europe green steel market share stood at 46.21% in 2025, with a valuation of USD 22.19 billion. This leading position is supported by ambitious climate policies, strong carbon pricing mechanisms, and extensive investments in renewable energy and hydrogen infrastructure. The region has become a global hub for green steel innovation, with numerous large-scale projects under development across Sweden, Germany, and other European countries.

Regional market expansion is driven by robust demand from automotive manufacturers, construction companies, and industrial users. Commercialization is being accelerated by partnerships between steel producers, technology developers, and renewable energy companies.

- In May 2023, thyssenkrupp nucera partnered with H2 Green Steel to supply over 700 MW of electrolysis to Europe’s largest green steel plant in Sweden. The project will use green hydrogen to generate 5 million tons of steel annually by 2030, with the plant’s emissions reduced by as much as 95% through renewable energy.

The Asia-Pacific green steel market is set to grow at a CAGR of 31.44% over the forecast period. This expansion is propelled by rapid industrialization, rising environmental awareness, and government support for clean manufacturing technologies. Increasing investment in advanced steelmaking technologies and a strong emphasis on reducing environmental impact are driving the adoption of green steel. Regional governments are implementing supportive policies, incentives, and pilot initiatives to support the shift to low-carbon production.

The growth of end-use sectors such as construction, automotive, and infrastructure is also driving market growth as companies seek to meet sustainability targets and respond to consumer demand for greener products. Increased collaboration across the value chain is also fostering innovation and scale-up of green steel solutions in the region. The region’s strong manufacturing base and increasing demand for low-carbon industrial materials are expected to drive significant uptake of green steel solutions.

- In February 2025, Nissan announced that it had increased the use of green steel in Japan fivefold compared to 2023, a milestone achieved in fiscal year 2025. The progress is part of Nissan’s goal to reduce CO₂ emissions by 30% by 2030, and to achieve carbon neutrality in all operations by 2050.

Regulatory Frameworks

- In the European Union, the Emissions Trading System (EU ETS) incentivizes manufacturers to reduce carbon emissions by imposing costs on carbon-intensive production methods. This will prompt steel producers to invest in low-carbon technologies and integrate with renewable energy.

- India’s National Steel Policy (NSP) 2017 promotes energy-efficient and environmentally sustainable production of steel by adopting cleaner technologies and renewable energy sources.

Competitive Landscape

The global green steel market is highly competitive, with the presence of established steel manufacturers, new technology providers, renewable energy developers, and hydrogen infrastructure companies.

Key players are investing in R&D, strategic partnerships, and capacity expansion to gain leadership in the growing low-carbon steel sector. Companies are partnering with automotive manufacturers, construction companies, and energy suppliers to build integrated green steel value chains.

Competition is moving toward technology innovation, production efficiency, carbon reduction capabilities, renewable energy integration and access to green hydrogen resources. Strategic alliances and large investments are expected to continue to be important competitive differentiators as demand continues to grow.

- In September 2023, Schaeffler expanded its partnership with H2 Green Steel by increasing its equity stake to USD 116 million and expanding the strategic technology collaboration. This step supports Schaeffler’s goal of climate neutrality by 2040 through the use of green steel, which can reduce CO₂ emissions in the supply chain by up to 95 percent compared to conventional steel.

Key Companies In The Green Steel Market

- Nucor Corporation

- ArcelorMittal

- SSAB

- Stegra AB

- Tata Steel

- NIPPON STEEL CORPORATION

- Salzgitter AG

- JFE Steel Corporation

- voestalpine AG

- JSW Group

- LIBERTY Steel Group

- Outokumpu

- HBIS GROUP

- SSG

- EMSTEEL

Recent Developments

- In March 2026, researchers from CSIRO and the Indian Institute of Science achieved a world-first by demonstrating, at commercial scale, that incorporating agricultural waste into steelmaking processes can reduce sector emissions by up to 50 percent. This advancement establishes a scalable and sustainable method for significant emission reduction within the steel industry.

- In September 2024, Tata Steel signed a USD 580 million grant agreement with the UK Government for a USD 1.45 billion green steel project at Port Talbot. The investment will install an electric arc furnace, reduce industrial carbon emissions by 8%, and advance the UK’s leadership in sustainable steelmaking.

- In March 2026, Millcon Steel and Meranti Green Steel signed a Memorandum of Understanding to drive the growth of green steel in Thailand. The partnership will focus on producing low-carbon steel, cutting greenhouse gas emissions, and engaging with stakeholders to establish standards and mechanisms to enable the country to move toward sustainable and competitive steelmaking.

- In January 2024, the European Investment Bank and the Nordic Investment Bank announced a USD 430 million financing package (supported by InvestEU) for H2 Green Steel’s large-scale plant in Boden, Sweden. The project aims to produce green steel with up to 95% lower CO2 emissions, supporting the decarbonization of the steel industry and the EU’s climate targets.

- In April 2026, PT Garuda Yamato Steel commissioned a landmark 6.5 MWp solar power facility in Bekasi, Indonesia, to provide clean power to its steel manufacturing operations. The major investment advances GYS’s decarbonization goals, reduces greenhouse gas emissions, and fortifies GYS’s role in Indonesia’s sustainable industrial transformation.