Market Definition

The electric motor market involves designing, manufacturing and distribution of electromechanical devices which transform electrical energy into mechanical energy. Their widespread ability to drive machinery, equipment, appliances, and transportation across industrial, commercial, residential, automotive, and consumer applications drive the market development. Market trajectory is further influenced by varying industrial production levels, infrastructure development, electrification trends, and regulatory standards associated with energy consumption and carbon emissions.

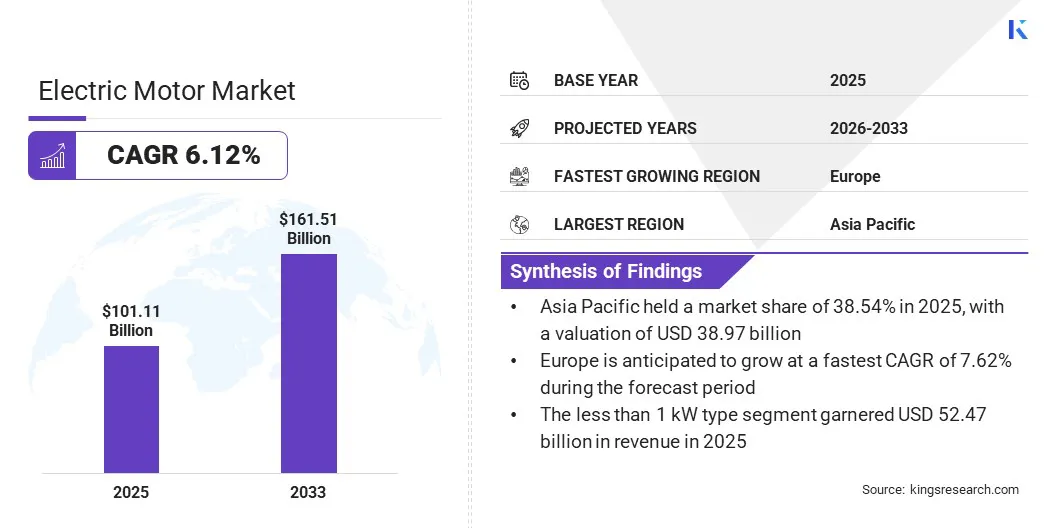

Electric Motor Market Overview

The global electric motor market size was valued at USD 101.11 billion in 2025 and is projected to reach USD 161.51 billion by 2033, representing a CAGR of 6.12% over the forecast period. Market growth is primarily driven by booming industrialization, which demands efficient electric motor designs across industrial pumps, air compressors, HVAC components, conveyor belt systems and industrial drive trains. Due to high energy consumption by electric motors (approximately 65% of industrial power consumption), the demand for designing energy-efficient motors is transitioning industry.

Additionally, the electrification of the automotive sector with widespread adoption of electric vehicles further fuels the market expansion. According to the International Energy Agency (IEA), electric vehicle sales exceeded 17 million globally in 2024 and over 20 million in 2025, signifying increasing demand for electric motors across transportation end-use verticals.

Major market players operating in the market include ABB, Danfoss A/S, Hitachi, Ltd., Johnson Electric Holdings Limited, Mitsubishi Electric Corporation, Nidec Motor Corporation, Schneider Electric, Siemens, Fuji Electric Co., Ltd., and others.

- In October 2025, YASA which is a subsidiary of Mercedes-Benz Group, introduced a "pancake" axial-flux electric motor capable of producing over 1,000 horsepower while weighing just 28 pounds (12.7 kg) and delivering a power density of 59 kW/kg.

Key Market Highlights:

- The electric motor market size was recorded at USD 101.11 billion in 2025.

- The market is projected to grow at a CAGR of 6.12% from 2026 to 2033.

- Asia Pacific electric motor market share was estimated at 38.54% with a valuation of USD 38.97 billion in 2025.

- The AC motor type captured the highest share of 73.20% and garnered USD 74.01 billion in revenue in 2025.

- The industrial end use captured the highest share of 38.12% and garnered USD 38.54 billion in revenue in 2025.

- Europe is anticipated to grow at a CAGR of 7.62% over the forecast period.

How is the increasing adoption of Industry 4.0 and smart manufacturing driving demand for electric motors?

The adoption of Industry 4.0 and smart factory automation is driving demand for electric motors as they act as critical components for automated machinery, connected manufacturing systems, predictive maintenance, energy-efficient operations, and collaborative robotics. Electric motors have evolved from basic mechanical propulsion into smart interconnected components. The inclusion of sensors in the motor systems helps in the collection and analysis of various factors, including temperature, vibration, and energy consumption data, which enables predictive maintenance and real-time performance optimization. This empowers the end users to identify potential production issues or manufacturing defects, leading to reduced maintenance costs and enhanced uptime.

Additionally, the electric motors play a vital role at the core of energy-efficient practices in smart factories. The sustainability factor empowers the manufacturers to design less energy-consuming motor designs as Variable Frequency Drives (VFDs) control electric motors. This minimizes energy waste and reduces operating costs while maintaining optimum motor performance levels.

- In November 2025, NIDEC Motor Corporation launched the TEFC Inverter Duty Closed Coupled Pump (CCP) motor line at Groundwater Week 2025. The motors offer enhanced performance and energy savings in variable-speed pumping applications used in irrigation, water treatment, data centers, commercial buildings, petrochemicals, and food processing.

Additionally, electric motors are structurally vital to the functionality of collaborative robots (cobots), which provide granular, responsive motion control necessary for machines to operate safely alongside human personnel.

- In April 2026, ABB launched high-speed, higher-payload PoWa cobots offering industrial-grade performance. The PoWa cobot offers six different payload categories ranging from 7kg - 30kg, offering a top speed of up to 5.8 m/s.

How are the supply chain disruptions of rare earth materials impacting the electric motor market?

Market expansion is hindered by the shortage of rare earth materials, which include Neodymium, Dysprosium, and Samarium. Electric motor permanent magnets made of rare earth elements by alloying Terbium, Praseodymium, and Iron-Boron (NdFeB) are used to produce powerful magnets for permanent magnet synchronous motors (PMSMs), which are lightweight and energy dense. The scarcity of rare earth materials restrains the market development avenues for electric motors used for specific end-use verticals. China’s control over more than 90% of global rare earth materials separation and refining capacity has led to export restrictions as a retaliatory move against U.S. tariff impositions. This has led to the deficit in high-performance permanent magnets required for EV drivetrains, highlighting structural vulnerabilities associated with geographic asset concentration for critical minerals, which restrains electric motor market growth.

To address the challenge, the market players are introducing rare earth material-free motor designs, which improve supply chain stability, lower production costs, eliminate environmental hazards from mining, and maintain high efficiency. These motors utilize varying magnetic resistance or induced electromagnetic fields in their designs.

- In February 2026, ABB expanded IE6 Hyper-Efficiency synchronous reluctance (SynRM) motor range, which includes no permanent magnets. The rare earth metal free design offers up to 76% energy savings and lower CO₂ emissions compared to IE5 alternatives over their operational lifetime.

- In October 2025, Niron Magnetics and Stellantis partnered to develop next-generation electric motors using rare-earth-free Iron Nitride magnet technology of Niron. The collaboration aims to reduce reliance on foreign rare-earth supply chains while improving motor performance and efficiency across vehicle types.

- In October 2024, Valeo and Mahle jointly launched the iBEE System, which is a next-generation brushless Electrically Excited Synchronous Motor (EESM) designed for high-performance 800V electric vehicles. The system eliminates the need for rare-earth magnets while delivering efficiency comparable to PMSMs.

How is the adoption of hairpin motor technology emerging as a notable trend in the electric motor market?

Hairpin motor technology incorporates the use of rectangular copper conductors, which are known as "hairpins," in place of conventional round wire windings. This enables higher power density, improved efficiency, and enhanced thermal management of the electric motor, enabling the design of compact motor configurations equipped with high torque. The technology finds extensive applicability in high-power industrial applications like generators and heavy machinery and in the automotive industry to enhance EV range along with overall drivetrain efficiency, steering systems, and auxiliary components.

- In May 2026, TECO launched high-payload UAV powertrain systems that include a hairpin motor powertrain, which offers a payload capacity in the 10-100 kg range. The UAV incorporates EV hairpin technology and a Halbach-array outer rotor to boost torque density and achieve peak efficiency of 91.8%, improving flight time by nearly 20%.

- In October 2025, BYD launched B12.b electric bus which features advanced wheel hub hairpin motor technology designed to enhance energy efficiency, performance, and passenger comfort. The vehicle is equipped with dual 150 kW hairpin motors that deliver high efficiency, reduced weight, lower noise levels, and improved torque for better acceleration and operation on demanding routes.

- In February 2025, BorgWarner Inc. secured four new electric motor projects with three major Chinese OEMs involving the supply of high-voltage hairpin (HVH) motors for a range of hybrid, plug-in hybrid, and battery electric vehicle platforms. The company introduced Ultra-Short High-Voltage Hairpin (S-HVH) eMotor technology, which enhances power density, improves efficiency, reduces copper usage, and supports both 400V and 800V vehicle architectures, addressing the evolving requirements of next-generation electric mobility.

Electric Motor Market Report Snapshot

|

Segmentation

|

Details

|

|

By Power Rating

|

Less than 1 kW, 1 - 2.2 kW, 2.2 - 375 kW, 375 -900 kW, Above 900 kW

|

|

By Type

|

AC Motor, DC Motor

|

|

By Standard

|

IE2, IE3, IE4, Others

|

|

By Rotor Type

|

Inner Rotor, Outer Rotor

|

|

By Application

|

Pump, Fans, Compressor, Machinery, Robotics, Others

|

|

By End Use

|

Industrial, Residential, HVAC, Municipal, Medical, Transportation, Others

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Power Rating (Less than 1 kW, 1 - 2.2 kW, 2.2 - 375 kW, 375 -900 kW, Above 900 kW). The less than 1 kW segment captures the highest market share of 51.89% in 2025 with a valuation of USD 52.47 billion. The high share is attributable to their applicability in residential and small-scale applications, which demand low-power, energy-efficient, and cost-effective solutions.

- By Type (AC Motor, DC Motor). The AC motor type segment was valued at USD 74.01 billion in 2025 and is anticipated to register a CAGR of 5.50% over the forecast period. The high efficiency, reliability, and use across industrial and commercial applications drives their demand and steady revenue growth.

- By Standard (IE2, IE3, IE4, Others). The IE3 standard captures the highest market share of 54.56% in 2025 with a valuation of USD 55.17 billion. The IE3 standard dominates the market due to its optimal balance of high energy efficiency and cost-effectiveness which makes it widely acceptable across industrial and commercial motor applications.

- By Rotor Type (Inner Rotor, Outer Rotor). The inner rotor segment was valued at USD 84.04 billion with the highest market share of 83.12% in 2025. The higher efficiency, compact design, and superior torque performance of inner rotors makes them a preferred choice across industrial and commercial applications.

- By Application (Pump, Fans, Compressor, Machinery, Robotics, Others). The fans segment captures the highest market share of 26.81% in 2025 with a valuation of USD 27.11 billion. The high share of fans is due to their extensive use in HVAC systems, industrial ventilation, and commercial cooling applications. The consistent demand for energy-efficient airflow solutions across residential, commercial, and industrial sectors drives their growth.

- By End Use (Industrial, Residential, HVAC, Municipal, Medical, Transportation, Others). The industrial end use segment captures the highest market share of 38.12% in 2025 with a valuation of USD 38.54 billion. The extensive reliance on electric motors for continuous, high-load operations across manufacturing, processing, and automation industries contributes to its high share.

What is the market scenario in the Asia Pacific and European regions?

Based on region, the global electric motor market has been segmented into North America, Europe, Asia Pacific, Middle East and Africa, and South America.

The Asia Pacific electric motor market share stood at 38.54% with a valuation of USD 38.97 billion in 2025. The region is designated as an emerging hub for the modernization of industrial infrastructure, which necessitates the adoption of electric motors across industrial and commercial applications. The rising automation trend further boosts their demand in automated industrial systems.

According to the International Monetary Fund (IMF), Asia Pacific is projected to remain the main driver of global growth. The region is anticipated to maintain moderate growth rate of up to 4.4% with China and India contributing approximately 70% of the growth.

Additionally, the high demand for electric vehicles in the region acts as a significant driver for electric motors. For instance, China registered sales of more than 13 million electric cars in 2025, maintaining its position as the largest electric car manufacturer and as a consumer of electric motors.

- In January 2026, VinFast reported preliminary full-year 2025 EV deliveries of 196,919 units across the globe, marking a 102% year-over-year increase. Southeast Asia and India emerged as the key growth markets, with the company ranked as the number one BEV brand in the Philippines, fourth in India and eighth in Indonesia.

The European electric motor market is set to grow at the growth rate of 7.62% over the forecast period. The expanding applicability of industrial electric mobility as a competitive standard in Europe across logistics, construction, and off-highway machinery drives the market growth of electric motors in the region. The move involves emphasis on replacing combustion systems with integrated electric motors, transmissions, and intelligent control systems across applications such as forklifts, AGVs, construction equipment, and other high-duty industrial vehicles.

Additionally, the European Commission introduced the Industrial Accelerator Act in March 2026, which is designed to boost the manufacturing capacity, protect strategic industries, and accelerate the transition to clean technologies of the region. The act further aims to reverse the decline of European manufacturing and increase its contribution to the EU GDP from 14.3% to 20% by 2035, leading to a boost in demand for industrial machinery and allied sectors.

- In October 2024, Valeo and MAHLE entered a partnership to develop the iBEE (Inner Brushless Electrical Excitation), a magnet-free electric motor system for upper-segment EVs. The new e-axle offers high performance levels between 220 kW and 350 kW and is designed to reduce carbon emissions by over 40% compared to permanent magnet motors and avoid rare earth materials.

- In May 2024, WEG launched W23 Sync+ ULTRA motor, which is an IE6 efficiency-class electric motor. The motor uses PMSynRM technology that involves combination of permanent magnet (ferrite or neodymium) and synchronous reluctance designs to reduce electrical losses. This causes electric motors to maintain high efficiency with varying speeds and load conditions across compressor, pump, fan, and conveyor applications.

Regulatory Frameworks

- In the U.S., the Energy Policy and Conservation Act (EPCA) prescribes energy conservation standards for commercial and industrial equipment including small electric motors (SEM). The act is designed to reduce national energy consumption and carbon emissions by ensuring that motors designed utilize energy as efficiently as technologically and economically possible.

- In Europe, the eco-design framework of European Commission Regulation (EU) 2019/1781 mandates electric motors between 75 kW and 200 kW to meet strict IE4 energy efficiency standards. The framework aims to significantly reduce annual energy consumption and CO2 emissions across Europe.

- In China, GB standards GB/T12350-2022 regulate the low-power electric motor market. It mandates key safety technical requirements in electric motor designs with focus on installation of basic insulation systems to address short-circuit protection requirements and strict temperature rise.

Competitive Landscape

Key players operating in the electric motor market, such as ABB, Danfoss A/S, Franklin Electric Co., Inc., Hitachi, Ltd., Johnson Electric Holdings Limited, Mitsubishi Electric Corporation, Nidec Motor Corporation, Schneider Electric, Siemens, Fuji Electric Co., Ltd., Toshiba International Corporation and others, are focusing on strengthening their market position through technological innovations, strategic partnerships, and capacity expansion to leverage the booming growth in the electric motors market. Market participants are further pursuing strategic mergers, acquisitions, and joint ventures to expand their global footprint, enhance production capabilities, and diversify their product portfolios across industrial, commercial, automotive, and allied end use sectors.

- In March 2026, EXEDY Corporation acquired Protean Electric which deals in in-wheel motor technology. The acquisition enables Protean to scale production of its in-wheel motor solutions, address rising demand for electric vehicle technologies and reduce manufacturing costs through EXEDY’s industrial capabilities.

- In December 2024, ABB acquired Aurora Motors, which is a U.S.-based provider of vertical pump motors with operations in China and California. The acquisition enables ABB to strengthen its NEMA motor product portfolio, enhancing its supply chain capabilities, and improve customer support worldwide.

- In August 2024, Nidec announced the acquisition of Houma Armature Works which is a U.S.-based company specializing in the manufacturing, repair, maintenance, and upgrading of motors, generators, and control systems. The acquisition is targeted at strengthening service and aftermarket capabilities and driving profitable growth.

Key Companies In The Electric Motor Market:

- ABB

- Danfoss A/S

- Franklin Electric Co., Inc.

- Hitachi, Ltd.

- Johnson Electric Holdings Limited

- Mitsubishi Electric Corporation

- Nidec Motor Corporation

- Regal Rexnord Corporation

- Robert Bosch GmbH

- Schneider Electric

- Siemens

- Fuji Electric Co., Ltd.

- Toshiba International Corporation

- WEG

- YASKAWA ELECTRIC CORPORATION

Recent Developments

- In June 2026, Mercedes-Benz commenced the production of a new lightweight axial‑flux electric motor to electrify its high‑performance AMG line. The "pancake" motor, acquired technology via Mercedes' 2021 purchase of YASA, is lighter and more efficient than conventional radial motors and will debut in the Mercedes‑AMG GT 4‑door coupe.

- In April 2026, Bosch launched permanent-magnet synchronous e-motor which offers reduction in losses by up to 30%. The motor delivers a continuous-to-peak power ratio of up to 93% and supports both battery-electric and hybrid powertrains. It further incorporates the use of rare-earth-reduced magnets to strengthen supply-chain resilience.

- In November 2025, Danfoss Power Solutions launched the Editron EM-PMI180 which is a 48-volt synchronous reluctance assisted permanent magnet (SRPM) low-voltage electric motor. The motor delivers 7 kW rated power at 3,000 rpm with maximum 90 Nm rated torque with 15% smaller envelope and 15% greater efficiency compared to AC induction motors.