Market Definition

The market encompasses the development, manufacturing, and sale of simulation-based racing products and software.

It includes hardware such as steering wheels, pedals, motion platforms, and VR headsets, along with software for racing simulations, training, and professional-grade applications. These solutions replicate real-world racing conditions, vehicles, and tracks, providing an immersive virtual experience.

Racing Simulator Market Overview

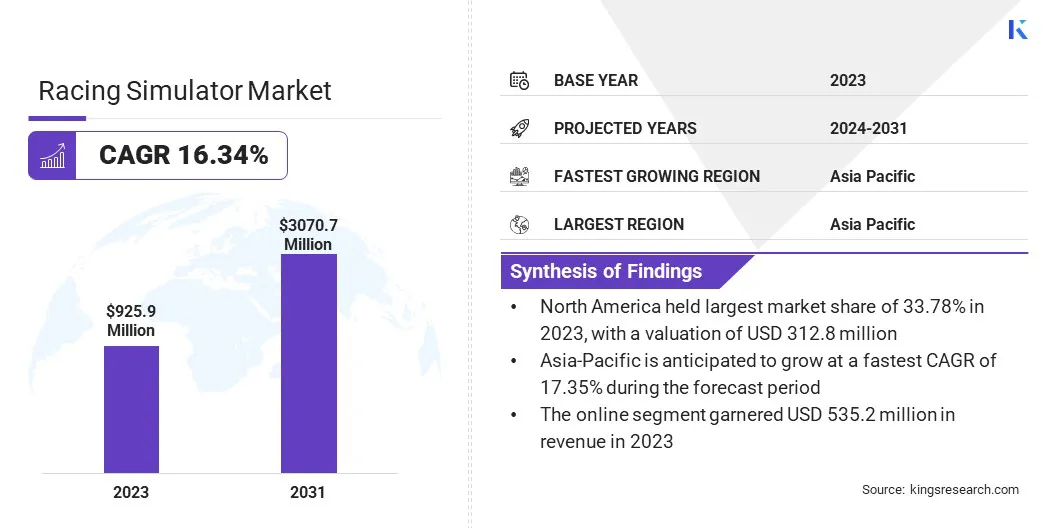

The global racing simulator market size was valued at USD 925.9 million in 2023 and is projected to grow from USD 1064.8 million in 2024 to USD 3070.7 million by 2031, exhibiting a CAGR of 16.34% during the forecast period.

The growing popularity of virtual racing competitions and esports has significantly boosted the demand for high-quality simulators, with professional drivers integrating them for training and strategy development. Advancements in hardware, such as enhanced force-feedback systems, motion platforms, and realistic vehicle physics, are further elevating user experience, attracting both enthusiasts and professionals.

Major companies operating in the racing simulator market are CXC SIMULATIONS, Trak Racer, SimXperience, Vesaro, VI-grade GmbH, Next Level Racing, AB Dynamics plc, D-BOX Technologies Inc., SIMWORX Pty Ltd., Cranfield Aerospace Solutions, Logitech, THRUSTMASTER, Fanatec, Cruden BV, and Ansible Motion Limited.

Innovations in cloud gaming and subscription-based models are expanding accessibility, enabling a wider audience to experience racing simulators without the need for expensive setups. With the rise of cross-platform integration and ongoing virtual reality advancements, the market is expected to see increasing consumer engagement across various demographics.

- In October 2024, Greaves 3D Engineering introduced “The Ultimate Drivers Rig,” a state-of-the-art racing car simulator designed for portability and professional performance. The simulator folds into a compact road case, allowing for easy transport to racetracks, trade shows, and corporate events.

Key Highlights:

- The racing simulator industry size was valued at USD 925.9 million in 2023.

- The market is projected to grow at a CAGR of 16.34% from 2024 to 2031.

- North America held a share of 33.78% in 2023, valued at USD 312.8 million.

- The hardware segment garnered USD 530.6 million in revenue in 2023.

- The beginner segment is expected to reach USD 1179.2 million by 2031.

- The personal segment is anticipated to witness the fastest CAGR of 16.51% during the forecast period

- The online segment garnered USD 535.2 million in revenue in 2023.

- Asia Pacific is anticipated to grow at a CAGR of 17.35% during the forecast period.

Market Driver

"Growth of Esports and Online Racing"

The growth of esports and online racing is boosting the growth of the racing simulator market. Competitive titles such as iRacing, F1 Esports Series, and Gran Turismo Sport attract global audiences through large-scale tournaments with substantial prize pools.

Online racing leagues, such as the Sim Racing League and VCO Simmy Awards, further support market growth by providing structured competitive platforms. Additionally, real-world motorsport teams, such as those in Formula 1 and NASCAR, integrate virtual racing into training and recruitment, strenghthening the connection between traditional motorsports and esports.

This growing recognition of virtual competitions and esports recognition has increased the demand for high-quality simulators, as gamers and aspiring drivers seek immersive, realistic experiences.

- In January 2025, BMW M Motorsport partnered with iRacing as the "Official Safety Car Partner," BMW M Motorsport for the 2025 virtual racing season. As part of this collaboration, BMW M Motorsport supplied the lead car for major races on the platform. Additionally, the BMW M2 CS Racing was introduced as a free entry-level model for all iRacing users in December.

Market Challenge

"High Cost of Advanced Simulators"

The high cost of advanced simulators is a major barrier to the racing simulator market. Premium systems, featuring force-feedback steering wheels, high-quality pedals, motion platforms, and VR headsets, can be costly.

While offering superior realism, their steep price tag limits adoption to professional drivers, and esports players. This challenges manufacturers to balance performance and affordability, restricting broader market accessibility.

Manufacturers can enhance accessibility by offering affordable entry-level options without compromising key features such as realistic feedback and basic immersion. Modular systems allowing gradual upgrades, financing plans, and subscription-based models can help manage costs.

Additionally, budget-friendly alternatives, such as compact setups or steering wheels and pedals with moderate force feedback, can maintain quality while reducing expenses.

Market Trend

"Integration of Virtual Reality (VR) and Augmented Reality (AR)"

The integration of virtual reality (VR) and augmented reality (AR) is transforming the racing simulator market by offering unparalleled immersion and realism. VR headsets, such as Oculus Rift and HTC Vive, immerse users in a 360-degree racing environment, and simulating real-world sensations such as G-forces and racing pressure.

AR enhances the experience by overlaying real-time data, such as lap times and racing lines, onto the environment to improve performance. In professional training, AR provides valuable insights with minimal distractions. As VR and AR technologies advance and become more accessible, they are driving growth in esports, professional racing, and the broader consumer market.

- In October 2024, Racing Unleashed and McLaren Racing announced a strategic partnership aimed at revolutionizing digital motorsport. By combining McLaren Racing's expertise in real-world racing with Racing Unleashed's leadership in digital simulation, the collaboration aims to enhance the global racing experience through the development of a McLaren Racing Motion Simulator..

Racing Simulator Market Report Snapshot

|

Segmentation

|

Details

|

|

By Component

|

Hardware, Software

|

|

By Type

|

Beginner, Medium, Full-scale

|

|

By End Use

|

Personal, Commercial, Training Institutes, Automotive

|

|

By Sales Channel

|

Online, Offline

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, UAE, Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Component (Hardware and Software): The hardware segment earned USD 530.6 million in 2023 due to the growing demand for high-performance steering wheels, pedals, motion systems, and VR equipment, which enhance the realism and immersion of racing simulations.

- By Type (Beginner, Medium, and Full-scale): The beginner segment held a share of 38.43% in 2023, due to the increasing affordability and accessibility of entry-level racing simulators, appealing to casual gamers and newcomers to racing simulations.

- By End Use (Personal, Commercial, Training Institutes, and Automotive): The commercial segment is projected to reach USD 980.5 million by 2031, owing to the rising adoption of racing simulators in esports arenas, entertainment centers, and professional racing teams for training, competitions, and consumer engagement.

- By Sales Channel (Online and Offline): The online segment is anticipated to witness the fastest CAGR of 16.36% over the forecast period, driven by the growing popularity of e-commerce platforms, digital distribution of racing simulator software, and the convenience of purchasing hardware and accessories online.

Racing Simulator Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and Latin America.

North America racing simulator market captured a share of around 33.78% in 2023, valued at USD 312.8 million. This dominance is reinforced by the increasing demand for immersive gaming experiences, technological advancements in simulation hardware, and the rise of eSports.

The regional market benefits from a well-established gaming infrastructure and a strong base of racing enthusiasts and gamers investing in high-quality simulators for entertainment and professional training. The growing popularity of virtual racing competitions and partnerships with automotive companies further fuel regional market expansion.

This trend is likely to continue, with key players focusing on enhancing realism and interactivity, providing North America with a competitive edge in the global market.

- In January 2025, SimCraft partnered with Riley Technologies, a leading North American race car constructor, to develop the official Riley Racing Simulator. This collaboration establishes SimCraft as Riley Technologies' official racing simulator provider, reinforcing both companies' commitment to innovation and excellence in motorsports.

Asia-Pacific racing simulator industry is set to grow at a robust CAGR of 17.35% over the forecast period. This growth is supported by a surge in interest in motorsports, particularly in countries such as Japan, China, and South Korea, where both traditional and virtual racing have strong followings.

The increasing adoption of gaming consoles, mobile gaming, and PC gaming, along with advancements in VR and AR technologies, is further fueling regional market growth. The region is home to numerous motorsports events and manufacturers, creating a strong demand for high-quality racing simulators for both recreational and professional training purposes.

With rising disposable incomes and an expanding gaming culture, the Asia-Pacific market is expected to witness a considerable uptick in consumer adoption and industry investment.

Regulatory Frameworks:

- In the European Union (EU), CE Marking regulation ensures that products meet essential health, safety, and environmental protection standards before sale in the European Economic Area (EEA).

- The Federal Communications Commission (FCC) Radio Frequency (RF) Safety Regulations, are designed to prevent electronic devices from emitting harmful electromagnetic radiation.

- The U.S. Department of Transportation (DOT) enforces vehicle safety and human factors regulations, particularly those simulating real-world driving conditions.

Competitive Landscape

Participants in the racing simulator industry are actively vying for market share through various strategies such as product innovation, mergers and acquisitions, partnerships, and geographical expansion.

Key players are increasingly focusing on enhancing the realism and customization of their simulators to attract both professional racers and gaming enthusiasts. Many are investing in advanced technologies such as motion-capture systems, virtual reality, and artificial intelligence to create a more immersive experience.

- In March 2024, Formula 1 announced a new multi-year partnership with Playseat, a leading racing simulator brand, to produce exclusive and bespoke F1 licensed racing products for gamers and sim racers. The collaboration highlights Formula 1's commitment to expanding audience engagement and enhancing fan experience.

List of Key Companies in Racing Simulator Market:

- CXC SIMULATIONS

- Trak Racer

- SimXperience

- Vesaro

- VI-grade GmbH

- Next Level Racing

- AB Dynamics plc

- D-BOX Technologies Inc.

- SIMWORX Pty Ltd.

- Cranfield Aerospace Solutions

- Logitech

- THRUSTMASTER

- Fanatec

- Cruden BV

- Ansible Motion Limited

Recent Developments (M&A/Partnerships/Agreements/New Product Launch)

- In February 2025, Masters of Motoring partnered with Perfect Acceleration Racing Simulators (PASR) and Veloce to integrate cutting-edge simulation technology and expert driver coaching into its premier automotive events. This collaboration enhances accessibility to professional motorsport training.

- In February 2025, Next Level Racing launched the Next Level Racing GTRacer 2.0 Simulator Cockpit, an evolution of its widely acclaimed GTRacer. Developed with global sim racer input, it offers enhanced ergonomics, increased adjustability, and enhanced durability.

- In February 2025, SimXperience launched an innovative motion table designed to elevate the racing simulation experience. Available in two configurations— the Traction Loss Package and the Enhanced Traction Loss + Longitudinal Motion Package.

- In June 2024, Next Level Racing and Pimax ormed a strategic partnership to enhance immersive realism in sim racing by combining Next Level Racing’s simulation hardware with Pimax’s advanced VR technology..

- In March 2024, Racing Unleashed and Pagani Automobili unveiled the Huayra R simulator, a groundbreaking advancement in virtual driving technology that merges digital and real-world motorsports.

- In November 2023, D-BOX Technologies Inc. and Playseat partnered to integrate D-BOX’s haptic technology into Playseat’s sim racing chassis and flying simulation cockpits, reinforcing its leadership in delivering realistic haptic experiences..