Medical Terminology Software Market Size

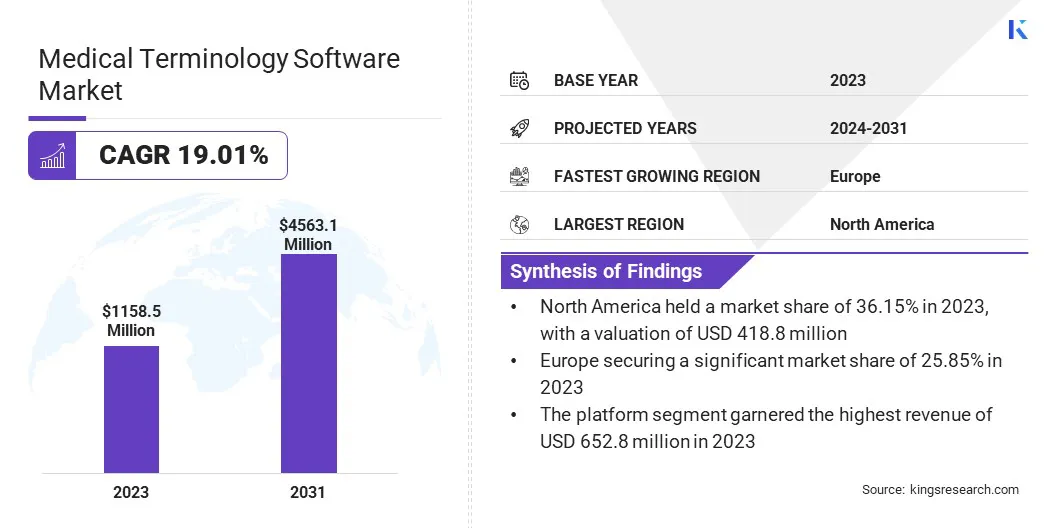

The global Medical Terminology Software Market size was valued at USD 1,158.5 million in 2023 and is projected to reach USD 4,563.1 million by 2031, growing at a CAGR of 19.01% from 2024 to 2031. In the scope of work, the report includes products offered by companies such as Intelligent Medical Objects (IMO), Clinical Architecture LLC, Apelon, Inc., CareCom A/S, Bitacube, Inc., Primaris Healthcare Solutions, 3M Health Information Systems, Wolters Kluwer Health, B2i Healthcare, HiveWorx and others.

The market for medical terminology software is experiencing strong growth, primarily driven by the increasing adoption of electronic health records (EHRs), advancements in healthcare technology, and the growing emphasis on regulatory compliance in the healthcare sector.

Key drivers propelling this growth include the integration of AI, natural language processing (NLP), and machine learning (ML) technologies into medical terminology software, improving data accuracy and decision-making processes for healthcare providers. The expansion of healthcare infrastructure in emerging economies further contributes to market growth opportunities, with a growing focus on digitalization initiatives and enhanced healthcare accessibility.

In the foreseeable future, innovations such as voice recognition, blockchain-based data management, and augmented reality are expected to transform the market, providing advanced features for clinical documentation, data security, and healthcare education. The medical terminology software market is marked by fierce competition among major players aiming to deliver holistic and interoperable solutions customized to address evolving healthcare demands worldwide.

Medical terminology software is a specialized tool designed to bridge the communication gap between clinical terminology and everyday language in the healthcare sector. It assists healthcare professionals in accurately documenting patient information, coding diagnoses and procedures, and ensuring regulatory compliance.

Key application areas include electronic health records (EHRs) integration for streamlined data management, clinical decision support systems (CDSS) for improved diagnosis and treatment planning, telehealth platforms for remote patient care, and medical education/training programs for healthcare professionals. These software solutions leverage technologies such as artificial intelligence (AI), natural language processing (NLP), and voice recognition to enhance efficiency and accuracy in healthcare documentation and processes.

Analyst’s Review

Key players in the medical terminology software market stand to achieve success by understanding and adapting to evolving consumer behavior trends, including demand for user-friendly interfaces, interoperability with existing healthcare systems, and customizable solutions. Leveraging advanced technologies such as artificial intelligence (AI) and natural language processing (NLP) has the potential to enhance software functionality, offering value-added features such as predictive analytics and automated coding suggestions.

Navigating the regulatory landscape, staying updated with healthcare regulations such as HIPAA, and fostering partnerships with healthcare institutions, industry stakeholders, and technology partners are playing a crucial role in sustained growth and competitive advantage in this dynamic and competitive market.

Medical Terminology Software Market Growth Factors

The rising focus on regulatory compliance, particularly with standards such as ICD-10 and SNOMED CT, is shaping the medical terminology software market landscape. Healthcare organizations globally must adhere to these stringent standards to ensure accurate coding, billing efficiency, and regulatory adherence.

Investing in advanced medical terminology software solutions becomes imperative for healthcare providers to effectively navigate these standards, translate clinical documentation into standardized codes, ensure coding accuracy, and automate coding processes.

As regulatory requirements continue to evolve, the demand for sophisticated medical terminology software equipped with compliance features and interoperability capabilities is expected to grow, thereby driving innovation and market expansion in the healthcare IT sector.

Utilizing medical terminology software for advanced clinical decision support systems enhances healthcare outcomes across medical settings. Integrated algorithms and data analytics provide valuable insights for diagnostic accuracy, treatment planning, and patient care.

These systems analyze patient data, including medical histories and imaging reports, to identify patterns and potential risk factors. Standardized medical terminologies such as SNOMED CT and ICD-10 enable accurate interpretation of clinical information, which aids informed decision-making at the point of care.

Addressing data privacy and security concerns within medical terminology software is crucial for trust and regulatory compliance in healthcare. Robust cybersecurity measures, including encryption protocols and access controls, are essential to safeguard patient data from unauthorized access and breaches. Healthcare organizations and software developers must implement stringent policies, conduct regular audits, and provide ongoing training to personnel.

Prioritizing data privacy and security mitigates risks, prevents breaches, and upholds the trustworthiness of medical terminology software. This proactive approach fosters a secure healthcare IT environment that is conducive to innovation and improved patient care.

Medical Terminology Software Market Trends

The emergence of augmented reality (AR) and virtual reality (VR) applications in healthcare education and training are set to drive the growth of the medical terminology software market. These technologies offer immersive learning experiences and simulation-based practice scenarios, revolutionizing healthcare professional training.

Intelligent medical terminology software seamlessly integrates with AR and VR platforms, providing accurate clinical data during training simulations. This integration enhances training realism, allowing users to interact with virtual patient cases, medical procedures, and diagnostic challenges in a risk-free environment.

As healthcare organizations prioritize continuous learning and skills development, the adoption of AR and VR-enabled training solutions supported by intelligent medical terminology software may increase, thereby improving educational outcomes and clinical proficiency. This convergence of technologies fosters innovation, efficiency, and excellence in healthcare education and practice, which is likely to drive market growth in the foreseeable future.

Segmentation Analysis

The global market is segmented based on type, end-user, application, and geography.

By Type

Based on type, the market is bifurcated into platform and services. The platform segment garnered the highest revenue of USD 652.8 million in 2023. Platforms offer comprehensive solutions that include advanced features such as AI-driven data analytics, interoperability with EHR systems, and customizable modules tailored to healthcare needs.

- The 2023 article published in the National Institutes of Health (NIH) journal BMC Medical Education underscores the potential of AI in healthcare, particularly in disease diagnosis and treatment selection.

This level of functionality and integration is essential for healthcare organizations seeking end-to-end solutions for clinical documentation, coding accuracy, and regulatory compliance. Additionally, platforms often provide scalability options, ongoing updates, and technical support, making them preferred choices for healthcare providers looking for robust and sustainable medical terminology software solutions.

By End-User

Based on end-user, the market is classified into healthcare providers, healthcare payers, and healthcare IT vendors. The healthcare providers segment accrued the largest medical terminology software market share of 45.09% in 2023. Healthcare providers, including hospitals, clinics, and physician practices, are the primary users of medical terminology software for clinical documentation, coding, and patient management.

The increasing adoption of electronic health records (EHRs) and the growing emphasis on data accuracy and regulatory compliance prompt healthcare providers to invest in advanced software solutions.

- A 2022 report by the Office of the National Coordinator for Health Information Technology (ONC) in the US shows that 96% of non-federal acute care hospitals and 78% of office-based physicians have adopted certified EHRs.

Additionally, the demand for integrated platforms offering seamless interoperability with existing healthcare systems boosts the adoption of medical terminology software among healthcare providers, thereby contributing to the segment's dominant market share.

By Application

Based on application, the market is classified into data aggregation, public health surveillance, data integration, clinical trials, and quality reporting, among others. The public health surveillance segment is anticipated to lead the medical terminology software market in the foreseeable future, reaching a valuation of USD 993.6 million by 2031. Increased global awareness of robust public health surveillance systems is expected to play a crucial role in the growth of the segment.

Medical terminology software plays a pivotal role in standardizing and analyzing vast amounts of health data, enabling early detection of disease outbreaks, monitoring population health trends, and facilitating data-driven public health interventions.

Medical Terminology Software Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

The North America Medical Terminology Software Market share stood around 36.15% in 2023 in the global market, with a valuation of USD 418.8 million.

- The region's leading position is supported by favorable initiatives such as the USD 5 billion budget allocated to the Advanced Research Projects Agency for Health (ARPA-H) by the US government, as highlighted in a recent report by the Office of Disease Prevention and Health Promotion (ODPHP).

This substantial funding underscores North America's commitment to advancing healthcare technologies, including the development of innovative solutions such as advanced medical terminology software. Such investments are expected to drive further growth and innovation in the region's healthcare IT sector.

Moreover, Europe experienced considerable growth in the medical terminology software market, securing a significant market share of 25.85% in 2023. The region's robust healthcare infrastructure and stringent regulatory frameworks promoting digital health initiatives, propel market growth in the region. European countries prioritize interoperability, data privacy, and quality healthcare delivery, which is driving the demand for innovative medical terminology software solutions.

With a rising focus on enhancing healthcare efficiency and patient outcomes, Europe is poised to maintain its leading position and drive further advancements in the market.

Competitive Landscape

The medical terminology software market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, are foreseen to create new opportunities for market growth.

List of Key Companies in the Medical Terminology Software Market

- Intelligent Medical Objects (IMO)

- Clinical Architecture LLC

- Apelon, Inc.

- CareCom A/S

- Bitacube, Inc.

- Primaris Healthcare Solutions

- 3M Health Information Systems

- Wolters Kluwer Health

- B2i Healthcare

- HiveWorx

Key Industry Development

- December 2023 (Product Launch): Google introduced MedLM, a medical language model designed specifically for the health industry. MedLM aimed to improve the understanding and summarization of medical information, assisting healthcare professionals in handling complex clinical data efficiently. This initiative reflected Google's commitment to developing specialized tools that catered to the unique needs of healthcare providers, enhancing the accuracy and effectiveness of medical terminology usage in healthcare settings.

The Global Medical Terminology Software Market is Segmented as:

By Type

By End-User

- Healthcare Providers

- Healthcare Payers

- Healthcare IT Vendors

By Application

- Data Aggregation

- Public Health Surveillance

- Data Integration

- Clinical Trials

- Quality Reporting

- Others

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America