Market Definition

Laboratory proficiency testing is an external quality assessment process that evaluates a laboratory’s ability to generate accurate and reliable test results. It compared performance against predefined standards and peer laboratories, ensuring compliance with global quality frameworks such as International Organization for Standardization (ISO), Clinical Laboratory Improvement Amendments (CLIA), and College of American Pathologists (CAP).

The market spans clinical diagnostics, food and beverage testing, pharmaceuticals, environmental monitoring, and cannabis testing, where accuracy and reliability are critical. Laboratories implement proficiency testing for accreditation, regulatory compliance, error detection, and performance benchmarking to maintain credibility and meet industry standards.

Laboratory Proficiency Testing Market Overview

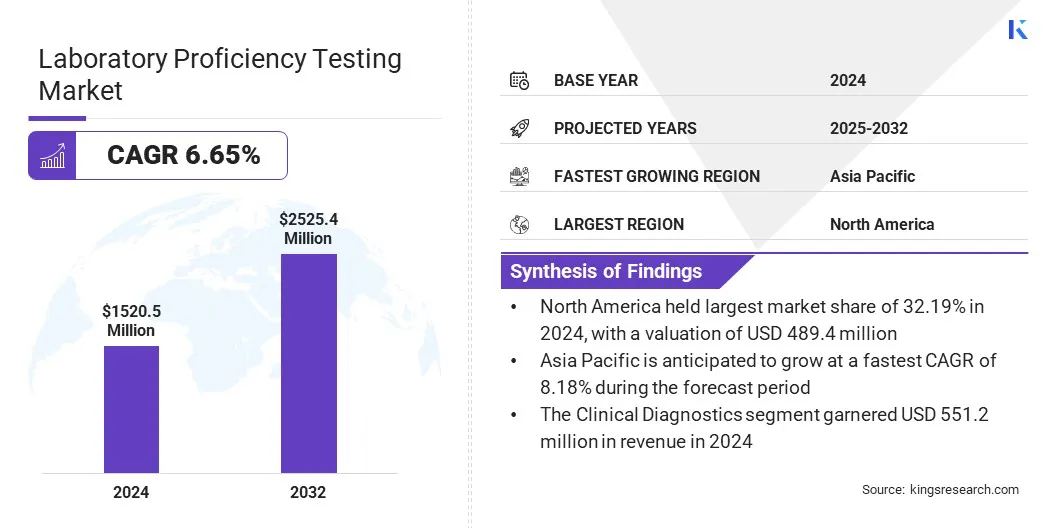

The global laboratory proficiency testing market size was valued at USD 1,520.50 million in 2024 and is projected to grow from USD 1,609.49 million in 2025 to USD 2,525.39 million by 2032, exhibiting a CAGR of 6.65% during the forecast period.

Market growth is driven by regulatory and accreditation requirements, prompting laboratories to participate in PT programs to comply with standards such as CLIA and ISO. Additionally, the integration of automation and big data in PT Programs streamlines workflows, reduces errors, and enables more accurate benchmarking across laboratories.

Key Highlights

- The laboratory proficiency testing industry size was valued at USD 1,520.50 million in 2024.

- The market is projected to grow at a CAGR of 6.65% from 2025 to 2032.

- North America held a share of 32.19% in 2024, valued at USD 489.45 million.

- The polymerase chain reaction (PCR) segment garnered USD 343.94 million in revenue in 2024.

- The clinical diagnostics segment is expected to reach USD 891.27 million by 2032.

- The academic & research laboratories segment secured the largest revenue share of 34.71% in 2024.

- Asia Pacific is anticipated to grow at a CAGR of 8.18% over the forecast period.

Major companies operating in the laboratory proficiency testing market are The College of American Pathologists, API, Randox Laboratories Ltd., UK NEQAS MICROBIOLOGY, EMQN, Weqas, SKML, GenQA, LGC Clinical Diagnostics (SeraCare), Association of American Feed Control Officials, AOAC INTERNATIONAL, CTS, Inc., INSTAND, Reference Institute for Bioanalytics, and IQMH.

The market is experiencing strong growth with the rising importance of accurate and reliable diagnostic testing. Increased adoption of molecular diagnostics, cell culture techniques, and specialized assays is highlighting the need for robust proficiency testing programs to ensure quality and compliance. The shift toward personalized medicine further increases demand, as laboratories must validate precision-driven results for disease-specific applications.

Recent initiatives, such as the College of American Pathologists (CAP) launching H5N1-specific proficiency testing schemes, highlight how tailored programs are evolving to meet emerging healthcare needs .

- In June 2025, the College of American Pathologists launched the H5N1 Influenza A Detection and Subtyping Program. This program provides two laboratory-created samples that simulate realistic patient specimens, allowing U.S.-based laboratories to verify their accuracy in detecting and differentiating H5N1 from seasonal flu strains.

Market Driver

Regulatory & Accreditation Requirements

The laboratory proficiency testing market is fueled by stringent regulatory and accreditation requirements that mandate laboratories to participate in proficiency testing. Standards such as the Clinical Laboratory Improvement Amendments (CLIA) in the United States and ISO/IEC 17025 globally enforce accuracy, reliability, and compliance across testing processes.

These regulations make proficiency testing a critical, not optional, supporting consistent performance validation. Sectors including healthcare, pharmaceuticals, and food safety are generating demand for proficiency testing services to maintain quality assurance and regulatory approval.

- In July 2024, the Centers for Medicare & Medicaid Services (CMS) finalized CLIA regulations, expanding proficiency testing requirements for additional analytes and tightening performance criteria. Newly included analytes such as hemoglobin A1c now require proficiency testing, while allowable error thresholds for tests such as hematocrit, red blood cell, and white blood cell counts have been reduced by up to 40%.

Market Challenge

High Capital and Operational Costs

A key challenge impeding the progress of the laboratory proficiency testing market is the high investment required for advanced analytical equipment and testing processes. Laboratories are relying on technologies such as liquid chromatography–tandem mass spectrometry (LC-MS/MS), which involve significant setup and operational expenditure.

Additionally, costs associated with sample preparation, logistics, data handling, and recruitment of skilled personnel are creating further financial pressure, particularly for smaller laboratories with limited budgets.

To address this challenge, market players are offering cloud-based data management systems, developing cost-sharing consortium models, and introducing scalable testing solutions that reduce upfront capital needs. These approaches facilitate wider participation in proficiency testing programs while easing the financial burden on resource-constrained laboratories.

Market Trend

Rising Adoption of Automation & Big Data in PT Programs

The laboratory proficiency testing market is witnessing a notable trend toward the surging adoption of automation and artificial intelligence to modernize testing processes. Automated platforms reduce manual intervention, minimizing errors in sample handling, distribution, and reporting.

AI-driven analytics enable faster and more accurate assessment of laboratory performance, uncovering patterns and deviations that may be overlooked through conventional evaluation. The use of big data further supports benchmarking across multiple laboratories, enhancing quality assurance, compliance, and overall efficiency in proficiency testing programs.

- In February 2025, Cormay Diagnostics partnered with the Randox International Quality Assessment Scheme (RIQAS) to provide world-class External Quality Assessment (EQA) programs. The partnership enables the evaluation of Cormay Diagnostics' in vitro diagnostic (IVD) solutions within RIQAS’s extensive global EQA services network. The collaboration involves the application of digital reporting tools and analytics in the assessment process.

Laboratory Proficiency Testing Market Report Snapshot

|

Segmentation

|

Details

|

|

By Technology

|

Cell Culture, Polymerase Chain Reaction (PCR), Immunoassays, Chromatography, Spectrometry, Others

|

|

By Industry

|

Clinical Diagnostics, Pharmaceuticals, Biologics, Microbiology

|

|

By End User

|

Hospitals & Clinics, Academic & Research Laboratories, Contract Research Organizations (CROs), Public Health Laboratories

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Technology (Cell Culture, Polymerase Chain Reaction (PCR), Immunoassays, Chromatography, Spectrometry, and Others): The polymerase chain reaction (PCR) segment earned USD 343.94 million in 2024, mainly due to its widespread use in molecular diagnostics and infectious disease testing.

- By Industry (Clinical Diagnostics, Pharmaceuticals, Biologics, and Microbiology): The clinical diagnostics segment held a share of 36.25% in 2024, largely attributed to the wide range of essential laboratory tests, which sustains demand for external quality assessment to ensure accuracy, compliance, and reliability across hospitals, diagnostic centers, and research laboratories.

- By End User (Hospitals & Clinics, Academic & Research Laboratories, Contract Research Organizations (CROs), and Public Health Laboratories): The academic & research laboratories segment is projected to reach USD 846.43 million by 2032, owing to high volumes of complex testing, strict adherence to research quality standards, and continuous need for external validation.

Laboratory Proficiency Testing Market Regional Analysis

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

The North America laboratory proficiency testing market share stood at 32.19% in 2024, valued at USD 489.45 million. This dominance is reinforced by the presence of leading pharmaceutical and biotechnology companies. Continuous investment in drug discovery, vaccine development, and biologics manufacturing requires reliable laboratory testing.

Additionally, regulatory oversight from the U.S. Food and Drug Administration (FDA) prompts laboratories to adopt PT programs to meet compliance and maintain credibility in clinical trials and quality assurance.

- In April 2024, the U.S. Food and Drug Administration (FDA) finalized a rule classifying laboratory-developed tests (LDTs) as medical devices under the Federal Food, Drug, and Cosmetic Act. The rule introduced a four-year phaseout of the agency’s enforcement discretion, establishing a staged compliance timeline for laboratories. Stage 1 begins in May 2025 and requires laboratories to comply with medical device reporting, correction and removal reporting, and maintenance of complaint files.

Moreover, the region is at the forefront of precision medicine and molecular diagnostics, fueled by a growing use of genetic testing, oncology panels, and infectious disease diagnostics. The expansion of personalized treatment models in North America is creating consistent demand for PT providers, as laboratories need external validation to ensure reliability in high-stakes testing.

The Asia-Pacific laboratory proficiency testing industry is estimated to grow at a CAGR of 8.18% over the forecast period. This growth is supported by the expansion of diagnostic laboratories in the region, characterized by rising healthcare spending and a growing patient base.

As laboratories conduct higher volumes of tests in areas such as infectious diseases and oncology, participation in PT schemes has become increasingly important to maintain credibility and meet accreditation standards. The demand for advanced diagnostic technologies further reinforces the need for consistent quality verification.

- In 2024, Agilus Diagnostics expanded its network of laboratories and earned additional international accreditations. The company extended its footprint across India, the Middle East, and South Asia, operating over 418 laboratories.

Additionally, concerns related to food quality and contamination have led regulatory authorities in Asia Pacific to strengthen safety standards, resulting in greater adoption of mandatory testing in food laboratories.

Regulatory Frameworks

- In the U.S., the Clinical Laboratory Improvement Amendments (CLIA), codified under 42 Code of Federal Regulations Part 493, mandate that laboratories performing human diagnostic testing must participate in approved proficiency testing programs. The regulations specify minimum sample numbers for each testing event, including five specimens for bacteriology, and are overseen by the Centers for Medicare & Medicaid Services (CMS). Failure to meet standards may result in sanctions, including loss of certification.

- In the UK, laboratory quality assurance is overseen by the United Kingdom Accreditation Service (UKAS), the sole national body appointed by the government. Medical laboratories must comply with ISO 15189:2022 – Medical laboratories: Requirements for quality and competence, which requires participation in external quality assurance schemes, including proficiency testing.

- In China, laboratory quality assurance is governed by the National Health Commission (NHC) and implemented through the National Center for Clinical Laboratories (NCCL). Clinical laboratories are required to participate in national and regional external quality assessment programs, which serve as the country’s form of proficiency testing.

- In India, the National Accreditation Board for Testing and Calibration Laboratories (NABL), under the Quality Council of India (QCI), governs laboratory and proficiency testing accreditation. Laboratories performing medical diagnostics must comply with ISO 15189, while PT providers are accredited under ISO/IEC 17043: Conformity assessment – General requirements for proficiency testing.

- South Korea manages laboratory accreditation through the Korea Laboratory Accreditation Scheme (KOLAS), operated by the Korean Agency for Technology and Standards (KATS). Laboratories are accredited under international standards, including ISO/IEC 17025, ISO 15189, and ISO/IEC 17043, with mandatory participation in proficiency testing at least once every three years for each accreditation field.

Competitive Landscape

Market players in the laboratory proficiency testing industry are adopting strategies such as expanding the scope of their proficiency testing programs, collaborating with specialized diagnostic companies, and incorporating advanced technologies to improve test accuracy and coverage, to maintain competitiveness.

They are also investing in research and development to introduce new testing modules, enhancing the reliability of their services across different laboratory disciplines. Strategic partnerships and technological upgrades help providers address emerging diagnostic needs and maintain regulatory compliance.

- In 2024, the Royal College of Pathologists of Australasia Quality Assurance Programs (RCPAQAP) expanded its Pediatric Diagnostic program from 10 to 12 samples. This adjustment aimed to enhance the program's comprehensiveness and better support laboratories in assessing pediatric diagnostic proficiency. Additionally, RCPAQAP launched a pilot External Quality Assurance (EQA) study for Mutation Detection in Lung Cancer, in collaboration with Roche.

Key Companies in Laboratory Proficiency Testing Market:

- The College of American Pathologists

- API

- Randox Laboratories Ltd.

- UK NEQAS MICROBIOLOGY

- EMQN

- Weqas

- SKML

- GenQA

- LGC Clinical Diagnostics (SeraCare)

- Association of American Feed Control Officials

- AOAC INTERNATIONAL

- CTS, Inc.

- INSTAND

- Reference Institute for Bioanalytics

- IQMH

Recent Developments (Product Launch)

- In March 2023, CAP launched a new proficiency testing program focused on the monkeypox (mpox) virus. This initiative aimed to enhance the quality assurance of molecular testing processes and contribute to the assurance of precise and dependable test outcomes, aiding in the detection of the mpox virus.

Laboratory Proficiency Testing Market

Laboratory Proficiency Testing Market