Idiopathic Pulmonary Fibrosis Market Size

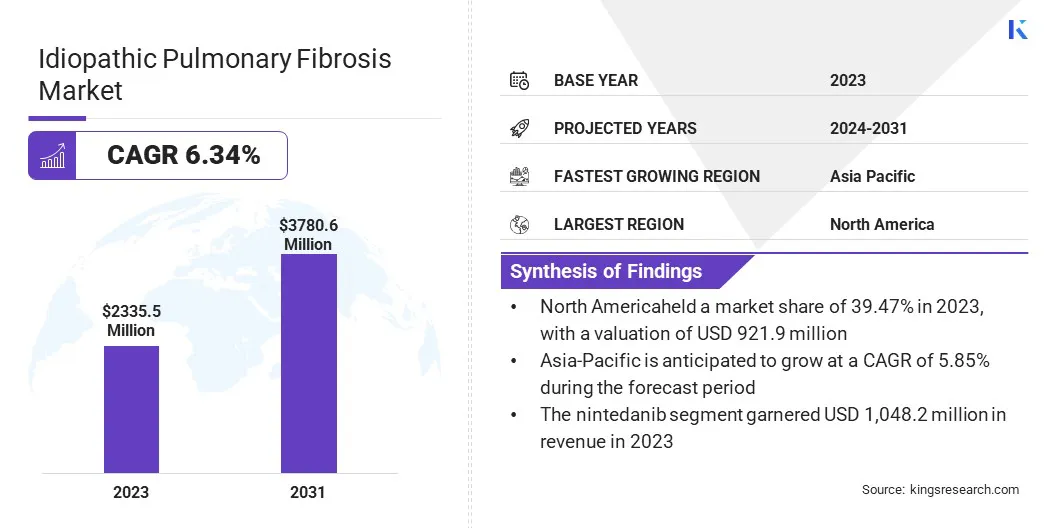

Global Idiopathic Pulmonary Fibrosis Market size was valued at USD 2,335.5 million in 2023 and is projected to grow from USD 2,457.9 million in 2024 to USD 3,780.6 million by 2031, exhibiting a CAGR of 6.34% during the forecast period. The market is expanding significantly due to the rising prevalence of the disease, ongoing research, and continual advancements in treatments such as antifibrotic drugs and personalized medicine.

Regulatory approvals and the introduction of novel therapies are improving treatment effectiveness and reducing adverse effects. In the scope of work, the report includes solutions offered by companies such as Boehringer Ingelheim International GmbH, Bristol-Myers Squibb Company, Cipla Inc., Hoffmann-La Roche Ltd, FibroGen Inc., MediciNova Inc., Merck & Co. Inc., Avalyn Pharma Inc., CS Pharmaceuticals, Novartis AG, and others.

The market is experiencing significant growth, driven by ongoing research, the development of advanced treatment options, and the increasing prevalence of the disease.

- According to an article published in the NIH, IPF is more prevalent in men than women, with adjusted prevalence estimates ranging from 0.33 to 2.51 per 10,000 individuals in Europe and from 2.40 to 2.98 per 10,000 individuals in North America.

Antifibrotic drugs and personalized medicine approaches are at the forefront, with the primary goal of slowing disease progression and improving patient outcomes. Increased regulatory approvals and emerging novel therapies are enhancing therapeutic efficacy and reducing adverse effects. Key players are investing in strategic initiatives such as mergers, acquisitions, and partnerships to strengthen their portfolios and expand their reach. As innovations continue to emerge, the IPF market is poised to experience considerable growth in the coming years.

Idiopathic Pulmonary Fibrosis (IPF) is a chronic lung disease marked by the progressive scarring (fibrosis) of lung tissue, which impairs normal respiratory function. Its exact cause of IPF remains unidentified ("idiopathic"), thereby complicating the diagnostic process. Symptoms of IPF include a persistent dry cough, shortness of breath, fatigue, and, ultimately, respiratory failure.

IPF primarily affects older adults and worsens over time, resulting in a poor prognosis and limited treatment options. The management of IPF is directed toward slowing disease progression and alleviating symptoms to improve the patient's quality of life. Research into IPF focuses on understanding its mechanisms, developing new therapies such as antifibrotic drugs, and exploring personalized treatment approaches based on genetic factors.

Analyst’s Review

The rising research and development activities, along with the growing adoption of strategic initiatives such as mergers, acquisitions, partnerships, and investments by key market players associated with the drug pirfenidone, are significantly contributing to idiopathic pulmonary fibrosis market growth. These efforts allow companies to strengthen their product portfolios and enhance distribution networks, thereby ensuring broader access to treatments.

- For instance, an article published in the Journal of Thoracic Disease in March 2023 reports that a clinical trial has been registered at the UMIN Clinical Trials Registry. This trial aims to evaluate the efficacy of perioperative pirfenidone therapy in patients with non-small cell lung cancer who also have idiopathic pulmonary fibrosis.This trial aims to confirm pirfenidone's preventative effect against postoperative acute exacerbation, highlighting the drug's potential and fostering further market expansion.

Key players are investing heavily in R&D, forming strategic partnerships, and conducting clinical trials to expand their product portfolios and enhance distribution networks, thereby driving market growth.

Idiopathic Pulmonary Fibrosis Market Growth Factors

The rising incidence of idiopathic pulmonary fibrosis (IPF) globally is contributing substantially to the expansion of the market, significantly increasing the demand for effective treatments and therapies. IPF is a chronic and progressive lung disease characterized by lung tissue thickening and scarring, which leads to severe respiratory issues. The exact cause remains unidentified, which complicates both diagnosis and treatment.

As the global population ages, with a notable increase among older adults who are more susceptible to IPF, the prevalence of this condition is expected to rise. This growing patient population underscores the pressing need for advanced therapeutic options, which is leading to significant investment and advancements in the IPF market.

The limited accessibility and high costs of treatment for idiopathic pulmonary fibrosis (IPF) are expected to hinder market growth by restricting patient access to advanced therapies. High costs are deterring patients from seeking treatment, thereby impeding market development. Additionally, limited accessibility due to regulatory barriers and complex diagnostic procedures is delaying treatment initiation, which is impacting overall market expansion.

However, key players are mitigating this challenge by engaging in pricing strategies, such as patient assistance programs and partnerships with healthcare providers, to improve affordability. They are further investing in research and development to innovate new treatments and streamline regulatory processes to expedite approval and market availability, thereby expanding access and enhancing patient outcomes in IPF management.

Idiopathic Pulmonary Fibrosis Market Trends

Improved diagnostic methods, including high-resolution imaging and genetic testing, are significantly boosting the growth of the idiopathic pulmonary fibrosis market by facilitating earlier and more accurate diagnoses. High-resolution imaging techniques, such as high-resolution computed tomography (HRCT), provide detailed images of lung tissue, enabling physicians to identify the characteristic patterns of IPF more precisely.

Genetic testing offers insights into the potential hereditary aspects and molecular mechanisms associated with the disease, enabling the development of more targeted and personalized treatment approaches. These advancements reduce the time required for diagnosis, thereby ensuring that patients receive timely and appropriate care. The rising demand for IPF treatments is aiding market growth.

The ongoing research and development of new and advanced treatment options, such as antifibrotic drugs and personalized medicine approaches, are significant trends reshaping the landscape of the idiopathic pulmonary fibrosis market. Antifibrotic drugs are designed to slow lung scarring progression and preserve lung function, thereby offering better disease management and improving patient outcomes. Personalized medicine tailors treatments based on individual genetic profiles, thereby ensuring more effective and targeted interventions.

- In January 2023, Bristol Myers Squibb reported results from a Phase 2 study investigating BMS-986278, an oral lysophosphatidic acid receptor 1 (LPA1) antagonist, in patients with idiopathic pulmonary fibrosis (IPF). The study showed that administering 60 mg of BMS-986278 twice daily for 26 weeks reduced the decline rate in percent predicted forced vital capacity (ppFVC) by 62% compared to placebo. These findings indicate that BMS-986278 effectively slowed the progression of the disease and enhanced lung function among IPF patients.

These innovations enhance therapeutic efficacy and reduce adverse effects, thereby fostering market growth. With the rise in regulatory approvals increase and the advent of novel therapies emerge, the IPF market is poised to witness substantial expansion, providing patients with more treatment options and improving their quality of life.

Segmentation Analysis

The global market is segmented based on drug type, distribution channel, and geography.

By Drug Type

Based on drug type, the idiopathic pulmonary fibrosis market is categorized into nintedanib, pirfenidone, and other. The nintedanib segment garnered the highest revenue of USD 1,048.2 million in 2023, mainly due to its role as a leading antifibrotic therapy. Approved for its ability to slow disease progression by targeting key pathways involved in lung fibrosis, nintedanib enhances lung function and quality of life for IPF patients.

Its mechanism, which inhibits multiple growth factors crucial in fibrotic processes, underscores its effectiveness. Widely adopted in treatment regimens, nintedanib's ongoing validation in clinical trials solidifies its status as a pivotal therapy, significantly contributing to market expansion by meeting critical therapeutic needs in managing this chronic and debilitating lung disease.

By Distribution Channel

Based on distribution channel, the market is divided into hospitals, retail, and online. The hospital segment captured the largest idiopathic pulmonary fibrosis market share of 54.18% in 2023. Hospitals serve as key providers of medical services, including specialized treatments and procedures that require advanced equipment and expertise.

This growth is further propelled by increasing healthcare demand due to aging populations, rising chronic disease prevalence, and technological advancements in medical treatments. Hospitals are playing a crucial role due to their capacity to handle complex cases, provide intensive care, and facilitate research and clinical trials. Their role as hubs for specialized care and as centers for medical innovation supports the expansion of the segment.

Idiopathic Pulmonary Fibrosis Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia-Pacific, MEA, and Latin America.

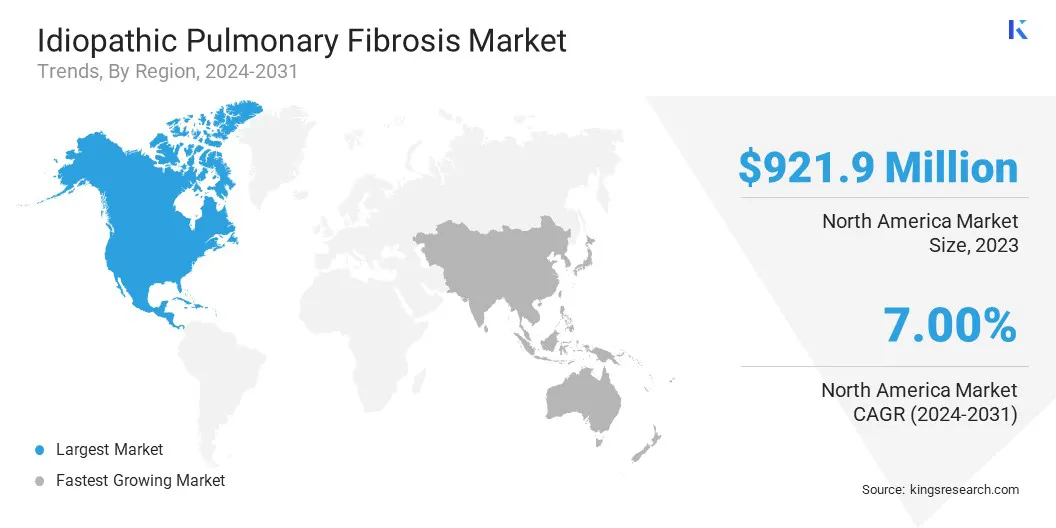

North America idiopathic pulmonary fibrosis market share stood around 39.47% in 2023 in the global market, with a valuation of USD 921.9 million. The region boasts a high prevalence of the disease, leading to a substantial demand for effective treatments such as antifibrotic drugs and personalized medicine. Regulatory frameworks in both countries enforce stringent standards for drug approvals and patient care, thereby fostering a favorable environment for regional market growth.

Furthermore, product launches, partnerships, and mergers and acquisitions are pivotal strategies that enable companies to broaden their product portfolios and geographic reach, thereby stimulating domestic market growth.

Asia-Pacific is anticipated to witness significant growth at a CAGR of 5.85% over the forecast period, mainly due to increasing awareness, healthcare infrastructure development, and the rising prevalence of chronic respiratory diseases. Countries such as China, Japan, and India are witnessing a growing incidence of IPF due to aging populations and environmental factors. Collaboration between local and international pharmaceutical companies and research institutions is further accelerating innovation in IPF management.

- For instance, in January 2023, Daewoong Pharmaceutical Ltd. out-licensed greater China rights for its idiopathic pulmonary fibrosis (IPF) candidate, bersiporocin (DWN-2088), to CS Pharmaceuticals Ltd. in a deal valued up to $336 million. Bersiporocin, a prolyl-tRNA synthetase inhibitor, was being developed by Daewoong for the treatment of IPF and potentially other fibrotic conditions. This strategic partnership allowed Daewoong to expand its market reach in the greater China region while leveraging CS Pharmaceuticals' expertise and distribution network.

Such collaborations are playing an important role in advancing the development and commercialization of innovative therapies, thereby contributing significantly to the growth of the Asia-Pacific IPF market.

Competitive Landscape

The global idiopathic pulmonary fibrosis market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Companies are implementing impactful strategic initiatives, such as expanding services, investing in research and development (R&D), establishing new service delivery centers, and optimizing their service delivery processes, which are likely to create new opportunities for market growth.

List of Key Companies in Idiopathic Pulmonary Fibrosis Market

- Boehringer Ingelheim International GmbH

- Bristol-Myers Squibb Company

- Cipla Inc.

- Hoffmann-La Roche Ltd

- FibroGen Inc.

- MediciNova Inc.

- Merck & Co. Inc.

- Avalyn Pharma Inc.

- CS Pharmaceuticals

- Novartis AG

Key Industry Development

- January 2023 (Approval): Lotus Pharmaceutical, a multinational pharmaceutical company based in Taiwan, announced that the US Food and Drug Administration (US FDA) had granted tentative approval for the Company's Abbreviated New Drug Application (ANDA) for Nintedanib Capsules, the generic version of Boehringer Ingelheim’s OFEV. Lotus Pharmaceutical's generic version intended to enhance treatment accessibility and affordability for patients with IPF, thereby potentially broadening access to essential therapy options.

The global idiopathic pulmonary fibrosis market is segmented as:

By Drug Type

- Nintedanib

- Pirfenidone

- Other

By Distribution Channel

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America