Market Definition

The market involves technologies and solutions that measure the distance between a sensor and objects within its field of view to generate three-dimensional data. The market encompasses a range of sensor types including stereo vision, time-of-flight (ToF), structured light sensors, and associated software components.

Depth sensing is used in applications spanning consumer electronics, automotive, industrial automation, healthcare, and robotics, supporting functions like gesture recognition, object detection, and spatial mapping. The report identifies the principal factors contributing to market expansion, along with an analysis of the competitive landscape influencing its growth trajectory.

Depth Sensing Market Overview

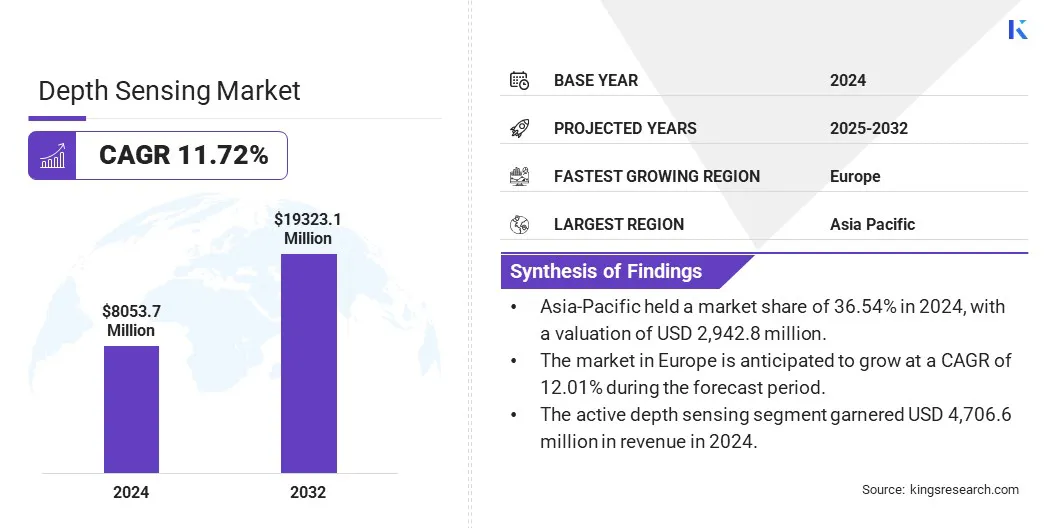

The global depth sensing market size was valued at USD 8,053.7 million in 2024 and is projected to grow from USD 8,897.0 million in 2025 to USD 19,323.1 million by 2032, exhibiting a CAGR of 11.72% during the forecast period. This growth is attributed to the rising integration of depth sensing technologies across diverse end-use sectors such as consumer electronics, automotive, healthcare, and industrial automation.

Major companies operating in the depth sensing industry are Qualcomm Technologies, Inc, Infineon Technologies AG, STMicroelectronics, Sony Depthsensing Solutions, Intel Corporation, pmdtechnologies ag, Analog Devices, Inc., Stereolabs Inc, Samsung, BECOM, Melexis, FRAMOS, Leopard Imaging Inc., KYOCERA Corporation, and Terabee.

Increasing demand for enhanced user experiences such as facial recognition, gesture control, and 3D imaging in smartphones and gaming devices is driving the adoption of depth sensing solutions.

The growing emphasis on autonomous systems, including self-driving vehicles and intelligent robotics, along with advancements in AR/VR applications, is further driving the growth of the market.

In addition, ongoing innovations in sensor accuracy, miniaturization, and cost-efficiency, combined with expanding applications in smart cities and surveillance, are accelerating the development of the market.

- In March 2025, onsemi unveiled the Hyperlux ID family, an advanced real-time indirect Time-of-Flight (iToF) depth sensor tailored for industrial applications. Capable of sensing depths up to 30 meters, it provides high-precision measurements of fast-moving objects, making it ideal for use in automation, robotics, logistics, and agriculture, while integrating both depth and monochrome imaging to streamline system design.

Key Highlights

- The depth sensing industry size was valued at USD 8,053.7 million in 2024.

- The market is projected to grow at a CAGR of 11.72% from 2025 to 2032.

- Asia-Pacific held a market share of 36.54% in 2024, with a valuation of USD 2,942.8 million.

- The active depth sensing segment garnered USD 4,706.6 million in revenue in 2024.

- The sensors segment is expected to reach USD 9,664.8 million by 2032.

- The automotive segment is anticipated to witness the fastest CAGR of 12.96% during the forecast period

- The market in Europe is anticipated to grow at a CAGR of 12.01% during the forecast period.

Market Driver

Rising Demand for 3D Imaging and Sensing in Consumer Electronics

The market is propelled by the rising demand for 3D imaging and sensing capabilities in consumer electronics. With increasing expectations for enhanced user experiences, consumers are seeking advanced features such as facial recognition, depth-enabled photography, and immersive augmented reality (AR) applications in smartphones, tablets, and wearable devices.

This is prompting leading electronics manufacturers to integrate depth sensing technologies such as time-of-flight (ToF), structured light, and stereo vision into their products.

This is further supported by the rapid evolution of smart devices and the expanding Internet of Things (IoT) ecosystem, where depth sensors enable applications like gesture control, secure authentication, and spatial mapping in smart home devices and personal electronics.

The growing consumer appetite for intelligent and interactive technologies is compelling brands to invest in compact, high-performance, and cost-effective depth sensing solutions, thereby accelerating the growth of the global depth sensing market.

- In December 2024, MagikEye Inc.unveiled the latest advancements in its Invertible Light Technology (ILT) at CES 2025, featuring advanced 3D depth sensing solution capable of measuring distances from as close as 5 centimeters to as far as 5 meters. This expanded range enables more immersive and precise interactions across various applications, including robotics, consumer electronics, AR/VR, industrial automation, and transportation.

Market Challenge

Complexity in Integration and Calibration

The complexity of integrating and calibrating depth sensing technologies presents a significant challenge to the growth and widespread adoption of these solutions, particularly in consumer electronics, automotive, and industrial automation sectors.

The calibration process for depth sensors is intricate, requiring precise alignment with other system components such as cameras, accelerometers, and AI algorithms.

Additionally, factors like device movement, varying light conditions, and environmental variables can compromise the accuracy of depth data, leading to unreliable performance. These integration challenges can delay product development, increase costs, and prevent seamless user experiences.

To address these issues, manufacturers are focusing on developing pre-calibrated, modular depth sensing solutions that simplify the process of embedding depth sensors into various systems.

AI-based calibration tools are also being employed to automate and enhance the accuracy of the setup, adapting to dynamic environments. Moreover, advanced sensor fusion techniques are integrated to improve the reliability and accuracy of depth sensing systems.

Market Trend

Advancements in Sensor Technologies

Advancements in sensor technologies are significantly reshaping the depth sensing landscape by improving performance, integration, and application versatility. Modern depth sensors now utilize cutting-edge architectures such as backside-illuminated (BSI) sensors, stacked designs, and SPAD arrays, which enhance light sensitivity, spatial resolution, and responsiveness in real-time 3D imaging environments.

These innovations allow for greater accuracy in depth perception, even under low-light or high-speed conditions, making them ideal for applications ranging from consumer electronics to robotics and autonomous systems.

Enhanced integration with edge computing capabilities also supports on-device processing, reducing latency and power consumption while enabling real-time decision-making.

Furthermore, the miniaturization of sensor components is facilitating compact and lightweight module designs, expanding their use in wearables, mobile devices, and UAVs. As sensor technologies continue to evolve, they are driving a new era of smart, adaptive, and energy-efficient depth sensing solutions across a broad range of industries.

- In April 2025, Sony Electronics announced the AS-DT1 LiDAR Depth Sensor, the smallest and lightest sensor in the world. Utilizing Direct Time of Flight (dToF) technology, it delivers precise 3D depth measurements up to 40 meters indoors and 20 meters outdoors, ideal for drones, robotics, and autonomous systems.

Depth Sensing Market Report Snapshot

|

Segmentation

|

Details

|

|

By Type

|

Active Depth Sensing, Passive Depth Sensing

|

|

By Component

|

Camera/Lens Module, Sensors, Illuminator

|

|

By End-user Industry

|

Automotive, Consumer Electronics, Medical, Industrial, and Others (Building Automation, Entertainment, Agriculture)

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Type (Active Depth Sensing, Passive Depth Sensing): The active depth sensing segment held 58.44% of the market in 2024, due to its ability to deliver more accurate and reliable depth measurements.

- By Component (Camera/Lens Module, Sensors, Illuminator): The sensor segment earned USD 3,828.7 million in 2024 due to its critical role in enabling precise depth measurement and enhancing system performance.

- By End-user Industry (Automotive, Consumer Electronics, Medical, Industrial, and Others (Building Automation, Entertainment, Agriculture)): The consumer electronics segment is projected to reach USD 7,126.8 million by 2032, owing to the increasing demand for depth sensing in devices like smartphones, wearables, and AR/VR applications.

Depth Sensing Market Regional Analysis

Based on region, the depth sensing industry has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Asia Pacific depth sensing market share stood at around 36.54% in 2024, with a valuation of USD 2,942.8 million. This dominance is attributed to the growing adoption of consumer electronics, rising disposable incomes, and strong demand for innovative smart devices such as smartphones, AR/VR headsets, smart home assistants, and wearable fitness trackers across the region.

across the region. Additionally, the increasing integration of depth sensing technologies in automotive applications, healthcare devices, and robotics continues to support the market growth in this region.

Favorable government initiatives that promote technological advancements in fields such as artificial intelligence, semiconductor manufacturing, 3D imaging, and autonomous systems,, along with expanding infrastructure for electronics manufacturing and research, further drive the market growth in Asia Pacific.

Furthermore, the region's focus on advancing AI and machine learning technologies is enhancing the capabilities and applications of depth sensing, thereby driving market growth.

- In January 2025, Kyocera Corporation (Japan) introduced an AI-based depth sensor capable of achieving 100μm resolution at a 10 cm range, including for reflective and semi-transparent objects. This technology is designed to support applications in manufacturing, medical imaging, and logistics by enabling more accurate measurement of small-scale objects that are typically difficult to evaluate.

The depth sensing industry in Europe is poised for significant growth at a robust CAGR of 12.01% over the forecast period. This growth is attributed to the increasing adoption of advanced technologies such as AI, IoT, robotics, and autonomous systems across various sectors, which is driving the demand for depth sensing solutions.

The region’s well-established technology infrastructure, coupled with the presence of leading manufacturers and innovators in the electronics and automotive sectors, supports the widespread integration and development of depth sensing technologies.

Rising investments in smart city development and autonomous mobility are also accelerating demand for advanced depth sensing technologies in applications such as traffic management, infrastructure monitoring, and autonomous navigation systems.

Additionally, ongoing advancements in AI, machine learning, and sensor miniaturization are enhancing the capabilities and applications of depth sensing, in turn, propelling market growth in this region.

Regulatory Frameworks

- In the European Union, CE marking requirements under the Radio Equipment Directive (RED) 2014/53/EU govern depth sensing components. It mandates compliance with safety, electromagnetic compatibility (EMC), and efficient use of the radio spectrum.

- In Japan, depth sensing systems are regulated under the Radio Law and Telecommunications Business Act, enforced by the Ministry of Internal Affairs and Communications (MIC). These frameworks ensure that depth sensing modules using RF or laser technology adhere to strict safety and spectrum-use standards.

- The International Electrotechnical Commission (IEC) regulates laser safety through the IEC 60825-1:2014 It classifies laser products by hazard level and sets requirements for labeling, safety measures, and user information to reduce risks in devices such as those used in depth sensing.

Competitive Landscape

The depth sensing industry is characterized by a diverse mix of well-established global players and innovative regional companies, each focusing on expanding their product portfolios and global presence through technological advancements, expansion and strategic collaborations.

- In February 2024, STMicroelectronics unveiled an expanded 3D depth sensing portfolio, featuring advanced Time-of-Flight (ToF) sensors. The new offerings include a 2.3k resolution direct ToF 3D LiDAR module designed for applications in AR, VR, robotics, and smart buildings. The company also introduced the VD55H1, the world’s smallest 500k-pixel indirect ToF sensor, aimed at enhancing mobile robotics with intelligent obstacle avoidance and precise docking.

Leading companies are heavily investing in research and development to improve the performance, accuracy, and energy efficiency of depth sensing technologies, with a focus on miniaturization and integration into a wider range of applications.

They are also developing cost-effective solutions to cater to the growing demand in consumer electronics, automotive, and industrial sectors. Additionally, firms are forming partnerships with key players in the automotive, healthcare, and robotics industries to enhance the deployment of depth sensing technologies across a broader range of use cases.

List of Key Companies in Depth Sensing Market:

- Qualcomm Technologies, Inc

- Infineon Technologies AG

- STMicroelectronics

- Sony Depthsensing Solutions

- Intel Corporation

- pmdtechnologies ag

- Analog Devices, Inc.

- Stereolabs Inc

- Samsung

- BECOM

- Melexis

- FRAMOS

- Leopard Imaging Inc.

- KYOCERA Corporation

- Terabee

Recent Developments (M&A/Partnerships/New Product Launch)

- In August 2024, Symbotic Inc. completed the acquisition of Veo Robotics’ assets, including its FreeMove 3D depth-sensing system, for USD 8.7 million. This strategic move strengthens Symbotic’s AI-powered robotic warehouse solutions by improving safety and enabling more flexible human-robot interaction, while also meeting stringent EU safety regulations.

- In January 2024, Infineon Technologies AG, in partnership with OMS and pmdtechnologies, launched a hybrid Time-of-Flight (hToF) camera to advance depth sensing and 3D mapping for smart consumer robots. The camera combines indirect and direct ToF technologies in one module, allowing for precise mapping and navigation in varied lighting environments.

- In March 2023, Sony Semiconductor Solutions launched the IMX611, a SPAD-based direct Time-of-Flight (dToF) depth sensor designed for smartphones. The sensor offers a high photon detection efficiency of 28% and enables precise distance measurements with minimal power consumption. It is expected to enhance smartphone features such as low-light autofocus, bokeh effects, and 3D spatial recognition for augmented reality.