Market Definition

The global market encompasses materials utilized in the manufacturing of aircraft, spacecraft, and defense equipment. The market is fueled by the growing demand for commercial aircraft, advancements in aerospace technology, and the expansion of space exploration.

The market focuses on high-performance materials that deliver durability, lightweight characteristics, and resistance to extreme conditions, driving growth and innovation across the industry. The report outlines the primary drivers of market growth, along with an in-depth analysis of emerging trends and evolving regulatory frameworks shaping the market trajectory.

Aerospace and Defense Materials Market Overview

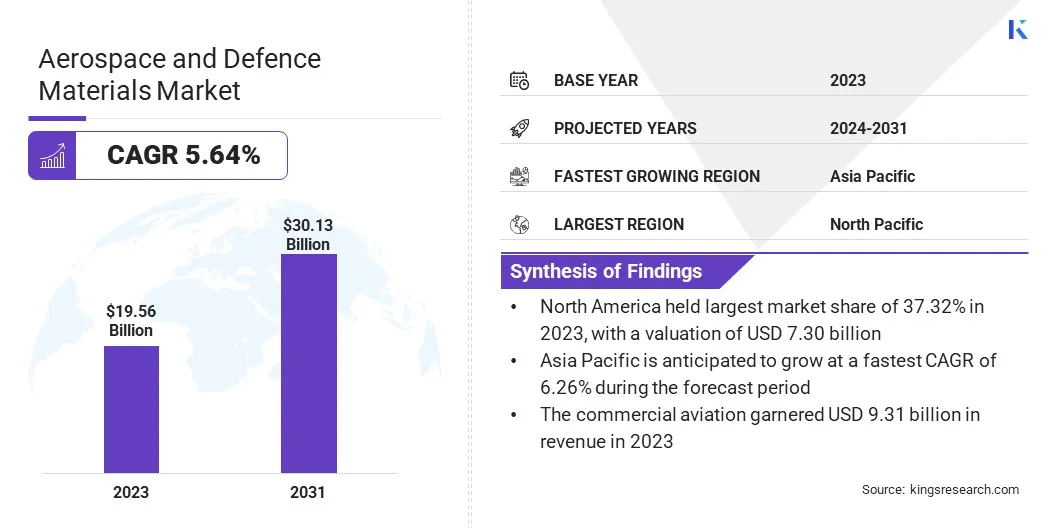

The global aerospace and defense materials market size was valued at USD 19.56 billion in 2023 and is projected to grow from USD 20.52 billion in 2024 to USD 30.13 billion by 2031, exhibiting a CAGR of 5.64% during the forecast period.

Strong commercial aviation growth and accelerated space programs are fueling the demand for innovative aerospace materials, positioning the market for sustained expansion and technological advancement.

Major companies operating in the aerospace and defense materials industry are TORAY INDUSTRIES, INC., Solvay, DuPont., Alcoa Corporation, TEIJIN LIMITED., ATI., Constellium, KOBE STEEL, LTD., AMG, Novelis, Hexcel Corporation, Arconic, CRS Holdings, LLC., Materion Corporation, and 3M.

The growing global demand for fuel-efficient and lightweight aircraft is driving the market. Airlines prioritize reducing fuel consumption and operational costs, prompting the increased use of advanced composites and alloys. This trend is fueling innovation in material technology to meet performance, sustainability, and cost-efficiency demands.

- In January 2024, the International Air Transport Association (IATA) announced that global air travel demand showed continued recovery in 2023. Total traffic surged by 36.9% compared to 2022, reaching 94.1% of pre-pandemic levels, while international traffic rose by 41.6%, highlighting a strong market rebound, especially in the fourth quarter.

Key Highlights:

- The aerospace and defense materials market size was valued at USD 19.56 billion in 2023.

- The market is projected to grow at a CAGR of 5.64% from 2024 to 2031.

- North America held a market share of 37.32% in 2023, with a valuation of USD 7.30 billion.

- The aluminum alloys segment garnered USD 7.16 billion in revenue in 2023.

- The commercial aviation segment is expected to reach USD 14.01 billion by 2031.

- The market in Asia Pacific is anticipated to grow at a CAGR of 6.26% during the forecast period.

Market Driver

Space Exploration & Satellite Expansion

The expansion of space exploration and satellite technologies is driving the global market. The demand for specialized materials, such as high-performance composites and alloys, surged as governments and private entities invested in advanced space missions.

These materials are essential for withstanding extreme conditions, ensuring the durability and functionality of spacecraft and satellites in space.

- In April 2024, a World Economic Forum report highlighted that the global space economy could surge to USD 1.8 trillion by 2035, rivaling the semiconductor industry. This growth will drive demand in the market, as space-based technologies like communications, navigation, and Earth observation services require advanced materials for their development and functionality.

Market Challenge

High Manufacturing Costs

The aerospace and defense materials market faces high manufacturing costs, due to advanced technologies and specialized facilities. These expenses are further amplified by the need for precision and compliance with stringent industry standards.

Companies should adopt cost-efficient methods like additive manufacturing (AM), automation, and strategic partnerships. Streamlining production, enhancing supply chain collaboration, and leveraging economies of scale can reduce expenses, improve profitability, and maintain a competitive edge in a demanding global market.

Market Trend

Lightweighting with Advanced Alloys

The global market is focused on the trend of lightweighting with advanced alloys. Manufacturers are turning to these alloys to reduce weight without compromising strength or durability as the demand for fuel-efficient and high-performance aircraft grows.

This trend is essential for improving operational efficiency, enhancing fuel economy, and meeting stringent environmental regulations.

- In June 2024, the Japan Aerospace Exploration Agency (JAXA), Mitsubishi Electric, Kumamoto University, and TOHO KINZOKU introduced the first high-precision 3D printing technology for magnesium alloys in wire-laser metal 3D printing. This advancement is set to transform the market by enabling the production of lighter, stronger components, enhancing fuel efficiency, reducing costs, and promoting sustainability in aerospace manufacturing.

Aerospace and Defense Materials Market Report Snapshot

|

Segmentation

|

Details

|

|

By Material Type

|

Aluminum Alloys, Steel Alloys, Titanium Alloys, Others

|

|

By Application

|

Commercial Aviation, Military Aircraft, Spacecraft

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation:

- By Material Type (Aluminum Alloys, Steel Alloys, Titanium Alloys, Others): The aluminum alloys segment earned USD 7.16 billion in 2023, due to its optimal balance of strength, lightweight properties, cost-efficiency, and corrosion resistance, making it ideal for high-performance structural applications in both commercial and military aerospace sectors.

- By Application (Commercial Aviation, Military Aircraft, Spacecraft): The commercial aviation segment held 47.61% share of the market in 2023, due to the rising demand for global air travel, fleet expansion by major airlines, and increased production of fuel-efficient aircraft, driving substantial material consumption for lightweight and durable components.

Aerospace and Defense Materials Market Regional Analysis

Based on region, the global market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America .

North America accounted for 37.32% share of the aerospace and defense materials market in 2023, with a valuation of USD 7.30 billion. This dominance is attributed to the high global defense spending in the region. The U.S. leads in military investments, driving the demand for advanced materials crucial for defense and aerospace applications.

This substantial budget supports innovation, technological advancements, and supply chain growth, reinforcing North America's strategic position in the market.

- In September 2024, the Aerospace Industries Association (AIA), in collaboration with S&P Global Market Intelligence, published key findings highlighting the significant contributions of the U.S. aerospace and defense industry. Generating over USD 955 billion in sales and contributing USD 425 billion to GDP in 2023, the U.S. remains a dominant player in the market, driving innovation and economic growth.

The aerospace and defense materials industry in Asia Pacific is poised for significant growth at a robust CAGR of 6.26% over the forecast period. This is attributed to significant investments from countries like China, Japan, and South Korea in developing domestic commercial aircraft programs.

This surge in aerospace manufacturing activity is boosting the demand for advanced materials across Asia Pacific, reinforcing its leadership role and boosting the global market.

- In December 2024, a report from Airbus highlighted China's continuous growth in aviation, with air travel reaching USD 700 million in passenger volume.

Regulatory Frameworks

- In the U.S., the Federal Aviation Administration (FAA) enforces strict regulatory frameworks governing civil aviation safety, including the certification of aerospace materials. Materials used in commercial aircraft must meet high-performance and safety standards, such as those specified under FAR Part 25, ensuring compliance and reliability across the nation’s aviation industry.

- In the U.S., the Environmental Protection Agency (EPA) enforces regulatory frameworks aimed at minimizing the environmental impact of aerospace and defence material manufacturing. These regulations mandate strict controls on hazardous substances, emissions, and waste management, ensuring that industry practices align with federal sustainability and environmental compliance standards.

- In Asia Pacific, the Civil Aviation Administration of China (CAAC) plays a pivotal role in regulating civil aviation safety and certifying aerospace materials. These regulations ensure that materials used in commercial aircraft meet stringent safety and performance standards, supporting the continued growth and global competitiveness of China’s expanding aerospace sector.

Competitive Landscape

The aerospace and defense materials market is undergoing significant consolidation through strategic acquisitions, allowing companies to expand their technological capabilities.

These mergers focus on advancing specialized materials, engineering solutions, and deployable systems, strengthening competitive positioning, driving innovation, and enhancing market differentiation in an increasingly dynamic and competitive industry environment.

- In March 2025, Applied Aerospace acquired NeXolve, a specialist in thermo-mechanical engineering and advanced polymer applications for space systems. This acquisition enhances Applied Aerospace’s position in the market, combining NeXolve’s expertise in deployable sunshields and solar sails with its capabilities in composite and metallic manufacturing to innovate in deployable sub-systems and advanced materials.

List of Key Companies in Aerospace and Defense Materials Market:

- TORAY INDUSTRIES, INC.

- Solvay

- DuPont.

- Alcoa Corporation

- TEIJIN LIMITED.

- ATI.

- Constellium

- KOBE STEEL, LTD.

- AMG

- Novelis

- Hexcel Corporation

- Arconic

- CRS Holdings, LLC.

- Materion Corporation

- 3M

Recent Developments (M&A/Product Launches)

- In January 2025, Redwire Corporation announced the acquisition of Edge Autonomy, a leader in uncrewed airborne system technology. This merger strengthens Redwire’s position in the market by enhancing its capabilities in space infrastructure and uncrewed systems. The acquisition also benefits Edge Autonomy, by ensuring its access to Redwire's resources, boosting innovation, and expanding its market reach in the aerospace and defense sector.

- In December 2024, Woodward announced the acquisition of Safran Electronics & Defense’s electromechanical actuation business, including advanced technologies for aircraft stabilization systems like Horizontal Stabilizer Trim Actuation (HSTA). This merger enhances Woodward’s aerospace capabilities, expanding its product portfolio for next-generation aircraft. The deal allows Safran to focus on other growth areas, while ensuring continued value creation under Woodward’s leadership.

- In January 2024, Arlington Capital Partners launched Verus Aerospace, a platform focused on next-generation aerospace, defense, and space programs. Comprising Arlington-backed companies, Verus specializes in manufacturing large, complex components for mission-critical applications, positioning itself as a key player in the market with operations across California, Kansas, and Washington.