Market Definition

Torque vectoring is an advanced drivetrain technology that manages the distribution of engine or motor torque across individual wheels. It encompasses traction control, stability enhancement, and cornering optimization, and is used in modern vehicles to improve driving dynamics, safety, and performance in high-performance and premium automotive applications.

Torque Vectoring Market Overview

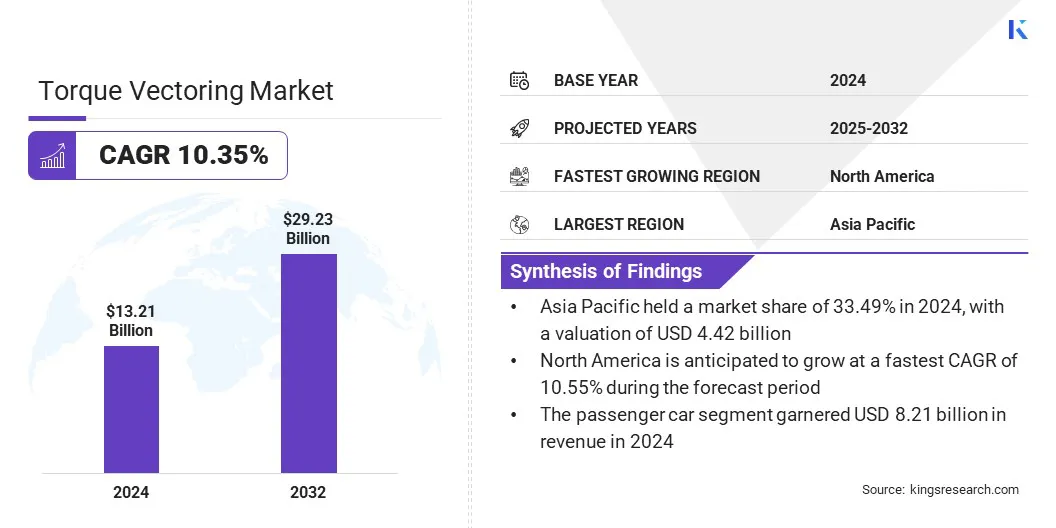

The global torque vectoring market size was valued at USD 13.21 billion in 2024 and is projected to grow from USD 14.52 billion in 2025 to USD 29.23 billion by 2032, exhibiting a CAGR of 10.35% during the forecast period.

Rising demand for high-performance and sports vehicles is driving torque vectoring adoption by enhancing handling, stability, and overall driving dynamics. Additionally, increasing consumer awareness of vehicle safety and advanced driver assistance systems (ADAS) is prompting manufacturers to integrate torque vectoring technologies to maintain stability, prevent skidding, and ensure stability during emergency maneuvers.

Key Highlights:

- The torque vectoring industry size was recorded at USD 13.21 billion in 2024.

- The market is projected to grow at a CAGR of 10.35% from 2024 to 2032.

- Asia Pacific held a share of 33.49% in 2024, valued at USD 4.42 billion.

- The active segment garnered USD 7.60 billion in revenue in 2024.

- The electronic segment is expected to reach USD 17.24 billion by 2032.

- The commercial vehicles segment is anticipated to witness the fastest CAGR of 10.57% over the forecast period.

- The front wheel drive (FWD) segment held a share of 42.17% in 2024.

- North America is anticipated to grow at a CAGR of 10.55% over the forecast period.

Major companies operating in the torque vectoring market are GKN Automotive Limited, BorgWarner Inc, ZF Friedrichshafen AG, Dana Limited, Magna International Inc, Nexteer Automotive Corporation, JTEKT Corporation, Honda Motor Co., Ltd, Voith GmbH & Co. KGaA, TOYOTA MOTOR CORPORATION, JAECOO, Automobili Lamborghini S.p.A, Continental AG, AISIN CORPORATION, and Nissan Motor Co., LTD.

Government funding is influencing market by enabling research, development, and innovation in advanced drivetrain technologies. It allows automakers and suppliers to accelerate the development and commercialization of torque vectoring systems and enhance vehicle performance and safety. It also enables them to adopt advanced solutions more efficiently, boosting technology adoption across the automotive sector.

- In January 2025, the U.S. Department of Energy (DOE) allocated USD 88 million through the Vehicle Technologies Office to promote research, development, and adoption of advanced drivetrain technologies, including torque vectoring systems.

Market Driver

Growth in Electric Vehicle Sales

A major factor propelling the growth of the torque vectoring market is the increasing adoption of electric and hybrid vehicles. Rising EV volumes are creating a strong demand for advanced torque management systems that enhance vehicle stability, handling, and performance.

This is prompting automakers and suppliers to invest in innovative torque vectoring solutions, develop software for precise torque distribution, and optimize wheel-level torque management, thus fueling market expansion.

- The International Energy Agency (IEA) reported that global electric vehicle sales reached 17 million units in 2024, a growth of over 25% from 2023. This highlights the rising demand for advanced drivetrain technologies, including torque vectoring systems, to enhance performance, handling, and safety in EVs.

Market Challenge

High Cost of Torque Vectoring Systems

A key challenge hindering the progress of the torque vectoring market is the significant investment required to design, manufacture, and implement advanced torque vectoring systems. The reliance on specialized components, sensors, and electronic control units spurs production costs, increasing vehicle prices. Additionally, the need for research, development, and calibration slows market growth and restricts widespread adoption of torque vectoring solutions.

To address this challenge, market players are developing lighter and more efficient components to reduce production expenses. They are optimizing electronic control units to improve system performance and lower manufacturing costs.

Furthermore, companies are adopting modular designs that simplify integration and minimize the development complexity of torque vectoring systems in modern drivetrains. Automakers are offering torque vectoring as part of optional packages in premium models to boost the adoption of advanced handling and stability technologies.

Market Trend

Integration of Torque Vectoring Systems with Electric Vehicle Powertrains

A key trend influencing the torque vectoring market is the increasing integration of torque vectoring systems with electric vehicle powertrains. Automakers are combining multiple motors, reducers, and control modules into single, compact units to optimize torque distribution, improve handling, and enhance vehicle stability.

This integration enables precise wheel-level control, supports energy-efficient operation, and improves low-speed maneuverability. It also prompts innovation in drivetrain design and software development to deliver superior performance, safety, and overall driving experience.

- In May 2025, InfiMotion Technology launched the TL 300 integrated drive system, an ultra-lightweight dual-motor powertrain with advanced torque vectoring. The compact unit combines dual motors, reducers, and a power control module. It offers improved energy efficiency, thermal management, and low-speed maneuverability while enabling enhanced handling in electric vehicles.

Torque Vectoring Market Report Snapshot

|

Segmentation

|

Details

|

|

By Technology

|

Active, Passive

|

|

By Clutch Actuation

|

Hydraulic, Electronic

|

|

By Vehicle

|

Passenger Car, Commercial Vehicles

|

|

By Propulsion

|

Front Wheel Drive (FWD), Rear Wheel Drive (RWD), All Wheel Drive/Four Wheel Drive (AWD/4WD)

|

|

By Region

|

North America: U.S., Canada, Mexico

|

|

Europe: France, UK, Spain, Germany, Italy, Russia, Rest of Europe

|

|

Asia-Pacific: China, Japan, India, Australia, ASEAN, South Korea, Rest of Asia-Pacific

|

|

Middle East & Africa: Turkey, U.A.E., Saudi Arabia, South Africa, Rest of Middle East & Africa

|

|

South America: Brazil, Argentina, Rest of South America

|

Market Segmentation

- By Technology (Active and Passive): The active segment earned USD 7.60 billion in 2024, largely due to higher adoption of advanced torque vectoring systems that enhance vehicle stability and handling.

- By Clutch Actuation (Hydraulic, and Electronic): The electronic segment held a share of 59.94% in 2024, fueled by its precise control, faster response, and compatibility with electric and hybrid drivetrains.

- By Vehicle (Passenger Car and Commercial Vehicles): The passenger car segment is projected to reach USD 17.99 billion by 2032, propelled by rising demand for high-performance and safety-enhanced vehicles.

- By Propulsion (Front Wheel Drive (FWD), Rear Wheel Drive (RWD), and All Wheel Drive/Four Wheel Drive (AWD/4WD)): The rear wheel drive (RWD) segment is anticipated to witness the fastest CAGR of 10.47% over the forecast period, attributed to improved handling and better performance with torque vectoring systems.

Torque Vectoring Market Regional Analysis

Based on region, the market has been classified into North America, Europe, Asia Pacific, Middle East & Africa, and South America.

Asia Pacific torque vectoring market share stood at 33.49% in 2024, valued at USD 4.42 billion. This dominance is reinforced by the rapid expansion of electric and hybrid vehicles, which is creating a strong demand for advanced torque management systems to enhance traction and driving stability.

Increasing focus on vehicle safety and performance standards is prompting automakers to adopt sophisticated torque vectoring technologies to meet regulatory requirements. Rising investments by automakers in local EV and hybrid production facilities are accelerating the adoption of advanced drivetrain technologies. Additionally, growing preference for SUVs and off-road vehicles is boosting the adoption of torque vectoring systems in the region.

- In May 2024, JAECOO launched its new J8 SUV featuring the ARDIS torque vectoring all-wheel drive system. The system dynamically distributes torque between front, rear, and individual rear wheels to enhance off-road performance, handling, comfort, and safety, with the capability to deliver up to 1,800 Nm of torque per wheel.

The North America torque vectoring industry is set to grow at a robust CAGR of 10.55% over the forecast period. This growth is bolstered by the rising adoption of electric and hybrid vehicles, leading to surging demand for advanced torque management systems to enhance the stability, handling, and traction of modern drivetrains.

Rising consumer preference for high-performance and luxury vehicles is prompting automakers to integrate sophisticated torque vectoring technologies. Additionally, the integration of torque vectoring in high-performance hybrid and sports SUVs is boosting the adoption of torque vectoring systems, propelling regional market growth.

- In May 2024, Lamborghini introduced the 2025 Urus SE, a performance-oriented hybrid SUV featuring a centrally-located electric torque vectoring system, a twin-turbo V8, and a rear electric motor. The system employs an electro-hydraulic multi-plate clutch to optimize torque distribution, enhancing vehicle stability, cornering, and drivetrain efficiency.

Regulatory Frameworks

- In the U.S., the National Highway Traffic Safety Administration (NHTSA) regulates vehicle safety standards, overseeing the design, performance, and integration of advanced drivetrain technologies, including torque vectoring systems. It ensures compliance with stability, traction, and electronic control requirements and evaluates software-driven torque management in electric and hybrid vehicles to maintain safety and performance.

- In the U.K., the Vehicle Certification Agency (VCA) regulates vehicle approval, safety, and environmental compliance. It oversees the adoption of advanced drivetrain technologies such as torque vectoring, monitoring stability, handling, and traction. VCA evaluates software-controlled torque distribution in EVs and hybrid vehicles, and ensures performance and safety standards align with European regulations.

- In China, the Ministry of Industry and Information Technology (MIIT) regulates automotive manufacturing and technology integration, overseeing advanced drivetrain adoption, including torque vectoring. It ensures compliance with safety, emissions, and energy efficiency standards, evaluates software-controlled torque distribution, and monitors integration in electric, hybrid, and high-performance vehicles.

Competitive Landscape

Major players in the torque vectoring industry are expanding their electric drivetrain offerings to meet growing demand in the EV and SUV sectors. They are deploying advanced torque vectoring systems that integrate torque management with axle disengagement to improve vehicle stability, traction, and handling.

Market participants are focusing on reducing brake and tire wear through optimized torque distribution. Additionally, they are developing software-driven control solutions to enable precise torque management and enhance the performance of intelligent electric drivetrains.

- In May 2024, BorgWarner expanded its electric drivetrain business by supplying HVH220 hairpin electric motors to Xpeng for upcoming SUV models and deploying its eTVD torque vectoring system with Polestar 3. The eTVD integrates torque vectoring with demand-controlled axle disengagement to improve stability, traction, and dynamic performance, reduce brake and tire wear, and support software-defined vehicle control in electric vehicles.

Key Companies in Torque Vectoring Market:

- GKN Automotive Limited

- BorgWarner Inc

- ZF Friedrichshafen AG

- Dana Limited

- Magna International Inc

- Nexteer Automotive Corporation

- JTEKT Corporation

- Honda Motor Co., Ltd

- Voith GmbH & Co. KGaA

- TOYOTA MOTOR CORPORATION

- JAECOO

- Automobili Lamborghini S.p.A

- Continental AG

- AISIN CORPORATION

- Nissan Motor Co., LTD.

Recent Developments (Product Launch)

- In May 2024, BorgWarner launched its electric Torque Vectoring and Disconnect (eTVD) system for battery electric vehicles. The system integrates torque vectoring with an on-demand disconnect function to enhance stability, traction, and dynamic performance, while reducing brake wear and improving driving safety and agility.