Semiconductor Market Size

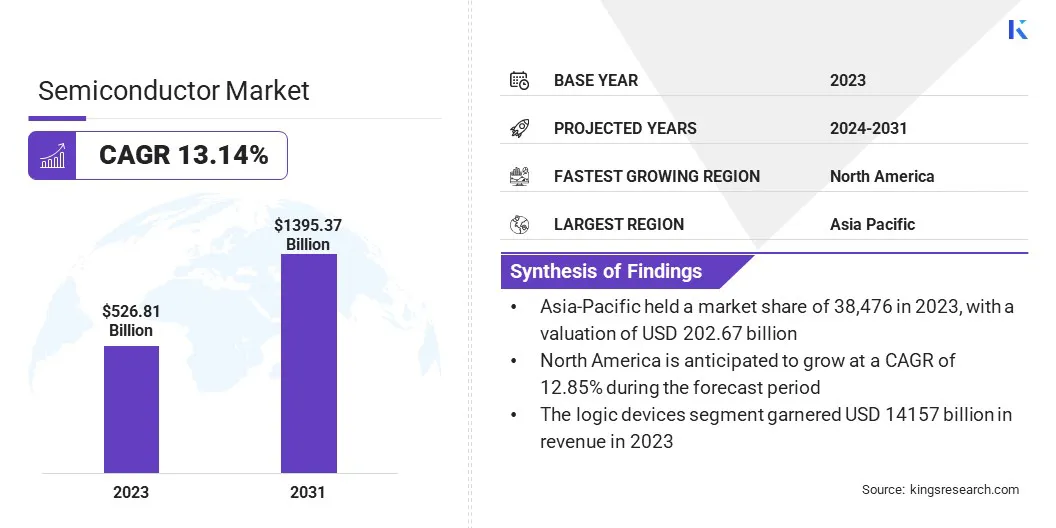

Global Semiconductor Market size was recorded at USD 526.81 billion in 2023, which is estimated to be at USD 588.12 billion in 2024 and projected to reach USD 1,395.37 billion by 2031, growing at a CAGR of 13.14% from 2024 to 2031. In the scope of work, the report includes solutions offered by companies such as Hua Hong Semiconductor Limited, Intel Corporation, MediaTek Inc., Micron Technology, Inc., Powertech Technology Inc., Qualcomm Technologies, Inc., Samsung, Taiwan Semiconductor Manufacturing Company Limited, United Microelectronics Corporation., SMIC, and others. This growth is driven by the increasing demand for electric vehicles, advancements in AI and IoT technologies, and adoption of 5G technology.

The semiconductor market is propelled by several key factors, including the rising demand for consumer electronics, such as smartphones and laptops. Moreover, the automotive industry's shift toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is boosting the requirement for semiconductors.

Furthermore, the proliferation of Internet of Things (IoT) devices necessitates more integrated circuits since, advancements in artificial intelligence (AI) and machine learning (ML) applications demand high-performance semiconductors. Thus, the ongoing digital transformation across industries enhances the need for data centers, thereby increasing the demand for semiconductors.

- The semiconductor market is a vital part of the technology sector, that is experiencing rapid growth. The market benefits from the constant innovation and broad application spectrum across industries.

Asia-Pacific leads in production and consumption, while North America and Europe also hold significant shares. The market is marked by rapid technological progress and heavy investment in research and development. Despite supply chain disruptions and geopolitical issues, the market maintains strong growth prospects, driven by increasing digitalization and technological advancements.

Semiconductors are materials with conductivity between conductors and insulators, essential for electronic devices. They form the foundation of modern electronics, enabling the functionality of a wide range of applications, from simple diodes to complex integrated circuits. Their key components include transistors, diodes, and microprocessors. Semiconductors are crucial in various industries, including consumer electronics, automotive, telecommunications, and healthcare, among others.

The semiconductor industry encompasses the design, manufacturing, and distribution of these components. The industry's success relies on continuous innovation, precision manufacturing processes, and robust supply chains to meet the growing global demand for electronic devices.

Analyst’s Review

In the market, manufacturers are intensifying efforts to innovate and meet evolving demands due to rapid advancements in technology. The key focus areas for manufacturers are the advancement of AI-specific chips and expansion of 5G-related semiconductor solutions. New product launches are driving competition, with a notable surge in specialized components for electric vehicles and IoT devices.

To maintain their significance and footprint in the industry, companies need to prioritize R&D investments, foster strategic partnerships, and maintain supply chain resilience. Staying agile in product development and market adaptation is crucial for sustained growth in this highly competitive industry.

Semiconductor Market Growth Factors

The growing demand for electric vehicles (EVs) is driving the semiconductor market expansion. EVs require advanced semiconductor components for their battery management systems, power electronics, and infotainment systems. Worldwide implementation of stricter emissions regulations and government incentives for EV adoption has caused the automotive industry to rapidly shift toward electrification. This transition is marked by continuous increase in the need for high-performance and efficient semiconductors.

Moreover, advancements in autonomous driving technology are further amplifying the demand for sophisticated semiconductor solutions, thereby fostering the market outlook.

- The U.S. Department of Energy's Advanced Technology Vehicles Manufacturing Loan Program provided eligible manufacturers with direct loans. These loans covered up to 30% of the expenses for expanding, re-equipping, or establishing manufacturing facilities in the U.S. These facilities were designed to be used for producing qualified ultra-efficient advanced technological vehicles (ATVs), alternative fuel infrastructure, or ATV components.

The ongoing supply chain disruptions are a significant challenge in the industry. These disruptions are a result of various factors, including geopolitical tensions and natural disasters, leading to production delays and component shortages. To overcome this challenge, companies are diversifying their supply chains by sourcing materials from multiple regions and investing in local manufacturing facilities.

Additionally, enhancing supply chain transparency through digital technologies such as blockchain is improving monitoring and management. Collaborative partnerships with suppliers and strategic stockpiling of critical components is further mitigating the impact of supply chain disruptions, ensuring a more resilient semiconductor market.

- The U.S. Department of Commerce initiated an updated Semiconductor Alert Mechanism, overseen by the International Trade Administration. This initiative aimed to identify and evaluate bottlenecks in semiconductor supply chains, facilitating better resource coordination to mitigate risks. Companies and stakeholders were encouraged to report disruptions to global semiconductor manufacturing facilities and supply chains. This information aided in assessing potential disruptions, engaging with trade partners, and safeguarding the global semiconductor supply chain.

Semiconductor Market Trends

The adoption of artificial intelligence (AI) is significantly impacting the semiconductor market. AI technologies require advanced and specialized semiconductors to handle complex computations and large datasets efficiently. Companies are developing AI-specific chips, such as neural processing units (NPUs) and application-specific integrated circuits (ASICs), to meet this demand. These chips are being integrated into various applications, including autonomous vehicles, smart home devices, and industrial automation.

Moreover, continuous advancements in AI and machine learning algorithms are driving the need for more powerful and efficient semiconductor solutions, thereby shaping the market's trajectory.

- In June 2023, AMD unveiled its future computing roadmap, alongside a range of products and partnerships aimed at advancing data center innovation. Collaborating with industry giants like AWS, Citadel, Hugging Face, Meta, Microsoft Azure, and PyTorch, AMD showcased its AI Platform strategy. This included the introduction of the AMD Instinct MI300 Series accelerator family, featuring the AMD Instinct MI300X accelerator, designed to cater to generative AI workloads. Additionally, AMD highlighted its ROCm software ecosystem, enhancing AI software compatibility and performance on AMD accelerators.

Notably, the expansion of 5G technology is transforming the semiconductor market. 5G networks require a new generation of semiconductors to support higher speeds, lower latency, and increased connectivity. This demand is driving the development of advanced radio frequency (RF) components, system-on-chip (SoC) designs, and power management integrated circuits (PMICs).

As telecommunications companies rapidly deploy 5G infrastructure globally, semiconductor manufacturers are innovating to meet these specific needs. The growth of 5G is enabling new applications in areas such as IoT, augmented reality (AR), and smart cities, further boosting the demand for cutting-edge semiconductor technology.

Segmentation Analysis

The global market is segmented based on component, application, and geography.

By Component

Based on component, the semiconductor industry is categorized into memory devices, logic devices, analog IC, MCU, MPU, sensors, discrete power devices, and others. The logic devices segment led the semiconductor market in 2023, reaching a valuation of USD 141.57 billion. Logic devices, including microprocessors and microcontrollers, are essential for various applications, from computing to telecommunications. The surge in demand for advanced computing devices, smartphones, and data centers is fueling this growth.

Additionally, the rise of artificial intelligence and machine learning applications requires sophisticated logic devices for processing power. Continuous innovation in semiconductor manufacturing and the push toward miniaturization are further contributing to the segment's robust expansion.

By Application

Based on application, the semiconductor industry is classified into telecommunication, defense & military, industrial, consumer electronics, automotive, and others. The consumer electronics segment is poised to witness significant growth at a CAGR of 13.93% through the forecast period (2024-2031). This expansion is attributed to the increasing consumer demand for smart devices, such as smartphones, tablets, and wearable technology.

Innovations in smart home appliances and entertainment systems are further boosting segment progress. The growing adoption of IoT devices, which integrate seamlessly with consumer electronics, is also a key factor fueling product adoption in the sector. Additionally, technological advancements in display technology, battery life, and device connectivity are driving the continuous growth and diversification of the consumer electronics segment.

Semiconductor Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia Pacific, MEA, and Latin America.

The Asia-Pacific Semiconductor Industry share stood around 38.47% in 2023 in the global market, with a valuation of USD 202.67 billion. This dominance in the global market is primarily backed by the presence of major semiconductor manufacturers such as TSMC, Samsung, and SMIC in the region that are leading in production capacity and technological advancements.

Additionally, the high demand for consumer electronics, automotive electronics, and industrial applications in countries such as China, South Korea, and Japan is fueling regional market growth. Government initiatives and investments in semiconductor infrastructure and research are also contributing to Asia-Pacific's leadership in the market.

North America is poised to register notable progress at a CAGR of 12.85% between 2024 and 2031. This growth is driven by the region's strong emphasis on innovation and technological development, particularly in fields such as AI, IoT, and 5G. The presence of major technology companies and extensive research and development activities are fostering advancements in semiconductor technologies.

Additionally, increasing investments in semiconductor manufacturing and efforts to strengthen the domestic supply chain are fostering the regional market outlook. The growing demand for advanced electronics in industries such as automotive, healthcare, and defense is further supporting North America's rapid semiconductor market expansion.

Competitive Landscape

The semiconductor industry report will provide valuable insights with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions. Manufacturers are adopting a range of strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, to strengthen their market standing.

List of Key Companies in Semiconductor Market

- Hua Hong Semiconductor Limited

- Intel Corporation

- MediaTek Inc.

- Micron Technology, Inc.

- Powertech Technology Inc.

- Qualcomm Technologies, Inc.

- Samsung

- Taiwan Semiconductor Manufacturing Company Limited

- United Microelectronics Corporation.

- SMIC

Key Industry Developments

- May 2023 (Launch): iDEAL Semiconductor unveiled its patented SuperQ technology, that displays enhanced power efficiency. This innovation is applicable across various sectors such as data centers and electric vehicles and is aimed to reduce power loss. The technology aligns with the majority of semiconductor manufacturing capacity, ensuring future compatibility by utilizing silicon. It is aimed to mark a significant departure from traditional power device architectures in order to enhance performance and sustainability in the semiconductor industry.

- August 2023 (Launch): Nidec Instruments Corporation, a subsidiary of Nidec Corporation, launched the SR7163 series in order to meet the rising demand for high-capacity semiconductor factories worldwide. This series features an arm-link mechanism, facilitates substrate transfer with precision, and has a small turning radius.

The Global Semiconductor Market is Segmented as:

By Component

- Memory Devices

- Logic Devices

- Analog IC

- MCU

- MPU

- Sensors

- Discrete Power Devices

- Others

By Application

- Telecommunication

- Defense & Military

- Industrial

- Consumer Electronics

- Automotive

- Others

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America