Reciprocating Engine Market Size

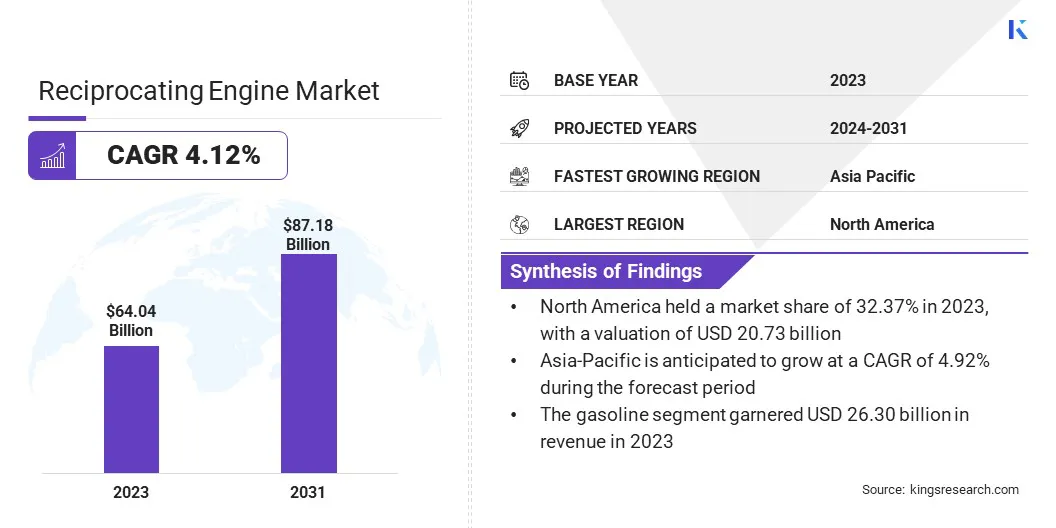

The global Reciprocating Engine Market size was valued at USD 64.04 billion in 2023 and is projected to grow from USD 65.72 billion in 2024 to USD 87.18 billion by 2031, exhibiting a CAGR of 4.12% during the forecast period. The growth of the market is driven by the increasing demand for reliable decentralized power generation, advancements in engine efficiency and emissions control, and expanding applications across industrial, automotive, and power generation sectors.

In the scope of work, the report includes products offered by companies such as Briggs & Stratton, Caterpillar, Cummins Inc., Fairbanks Morse Defense, IHI Power Systems Co.,Ltd., Kawasaki Heavy Industries, Ltd., MAN Energy Solutions, Siemens AG, Wärtsilä, MITSUBISHI HEAVY INDUSTRIES, LTD., and others.

The expansion of the reciprocating engine market is primarily spurred by increasing demand for reliable and efficient power generation solutions. Key sectors such as industrial manufacturing, power utilities, and marine transportation are significant contributors to this demand. Additionally, the shift toward reducing carbon emissions is fostering innovation in fuel-efficient and environmentally-friendly engine technologies.

The rise in decentralized power generation and combined heat and power (CHP) systems further bolsters market growth. Furthermore, the expanding infrastructure in emerging economies and the need for backup power systems in developed regions stimulate market expansion. The versatility and adaptability of reciprocating engines to various fuels, including natural gas and renewable options, further enhance their market appeal.

- According to the U.S. Energy Information Administration (EIA), the industrial sector accounted for nearly 26% (1.02 trillion kWh) of total electricity consumption in the U.S. in 2023, highlighting the crucial role of reciprocating engines in powering industrial operations.

The reciprocating engine market encompasses a wide range of applications across multiple sectors, including power generation, transportation, and industrial machinery. These engines are renowned for their efficiency, reliability, and ability to run on diverse fuel types. The market is characterized by continuous technological advancements aimed at improving performance and reducing environmental impact.

Major market players are investing heavily in research and development to enhance engine efficiency and comply with stringent emission regulations. The market exhibits robust growth potential, driven by the increasing demand for decentralized power solutions and the integration of renewable energy sources.

A reciprocating engine, also known as a piston engine, is a type of internal combustion engine where pistons move up and down within cylinders to convert pressure into a rotating motion. This engine type is widely used in various applications, including power generation, automotive, marine, and industrial sectors. The reciprocating motion is achieved through the combustion of fuel, which creates pressure and drives the pistons.

These engines are valued for their high efficiency, operational reliability, and fuel flexibility, as they possess the ability to operate on natural gas, diesel, and alternative fuels. Their adaptability to a range of operational requirements makes them a crucial component in both stationary and mobile power solutions.

Analyst’s Review

Manufacturers are focusing on enhancing engine efficiency and reducing emissions to meet stringent regulatory standards globally. These efforts include the development of advanced combustion technologies and the integration of digital solutions for enhanced performance monitoring and maintenance prediction. Manufacturers are further expanding their product portfolios to include hybrid and dual-fuel engines, catering to the growing demand for flexible and sustainable power solutions.

- In May 2024, Toyota Motor Corp., Mazda Motor Corp., and Subaru Corp. announced they had developed new engines to improve their hybrid and plug-in hybrid vehicles. These engines enabled the cars to carry more batteries, reduced CO2 emissions, and allowed vehicles to function similar to EVs while maintaining engine power for long distances. This effort addressed slowing global EV sales and aimed to offer diverse green vehicle options for carbon neutrality.

As the market evolves, continuous innovation remains crucial to stay competitive. Manufacturers are prioritizing research in renewable fuel integration and investing heavily in IoT capabilities for real-time data analytics. Moreover, enhancing customer support networks and fostering strategic partnerships are likely to be essential to navigating the dynamic landscape of the reciprocating engine market effectively.

Reciprocating Engine Market Growth Factors

Businesses and communities are continuously seeking reliable, on-site power solutions to ensure uninterrupted energy supply and reduce dependence on centralized grids. This demand is particularly strong in remote and rural areas where grid access is limited.

- According to a 2023 report by the International Energy Agency (IEA), over 600 million people in Africa still lack access to electricity, with the majority residing in rural areas where infrastructure development remains a critical challenge.

Decentralized power generation through reciprocating engines offers flexibility, scalability, and efficiency. These engines are continuously being improved to operate on various fuels, including renewable options, which makes them environmentally sustainable. As energy needs grow, the versatility and reliability of reciprocating engines are continuously positioning them as a preferred choice for localized power generation solutions.

A major challenge in the reciprocating engine market is the stringent emission regulations. These regulations are continuously being implemented globally to reduce environmental pollution. To overcome this challenge, manufacturers are focusing on developing advanced engine technologies that enhance fuel efficiency and lower emissions. Incorporating cleaner fuel alternatives such as natural gas and biofuels is emerging as an effective solution to mitigate this challenge.

Additionally, investing in research and development to improve combustion processes and integrate after-treatment systems contribute significantly to meeting emission standards. Continuous innovation and collaboration with regulatory bodies are essential strategies. By addressing emissions through technological advancements, the market is continuously evolving to meet environmental requirements while maintaining performance and reliability.

Reciprocating Engine Market Trends

The increasing adoption of hybrid power systems is resulting in the integration of reciprocating engines with renewable energy sources such as solar and wind power. This integration enhances energy reliability and efficiency by utilizing multiple energy inputs.

Hybrid systems are gaining significant traction in both stationary and mobile applications, offering flexibility and reducing dependency on traditional fossil fuels. The trend toward hybridization is further fostered by the rising need for sustainable energy solutions that reduce carbon footprint and operational costs over the long term.

Manufacturers are investing heavily in hybrid technology to optimize system performance and meet diverse customer demands for resilient and eco-friendly power solutions. Another significant trend impacting the reciprocating engine market is the focus on digitalization and connectivity. Engine manufacturers are increasingly incorporating IoT (Internet of Things) technologies and advanced analytics to enhance engine performance monitoring and predictive maintenance capabilities.

Real-time data analytics enable operators to optimize engine operation, improve fuel efficiency, and minimize downtime. Digitalization further supports remote monitoring and control, thereby enhancing operational flexibility and responsiveness.

This notable trend toward smart, connected engines is spurred by the industry's imperative for enhanced operational efficiency, reduced maintenance costs, and improved reliability. As digital technologies continue to evolve, their integration into reciprocating engines is expected to foster innovation and enhance competitiveness in the market.

Segmentation Analysis

The global market is segmented based on type, power, and geography.

By Type

Based on type, the market is categorized into gasoline, diesel, natural gas, and others. The gasoline segment led the reciprocating engine market in 2023, reaching a valuation of USD 26.30 billion. The gasoline segment has experienced significant expansion primarily due to its widespread application in automotive and small-scale power generation.

Gasoline engines are highly favored for their affordability, ease of maintenance, and suitability for smaller power applications such as portable generators and lawn equipment. In the automotive sector, gasoline engines dominate owing to their performance characteristics and existing infrastructure support. The growth of the segment is further bolstered by ongoing technological advancements that improve fuel efficiency and reduce emissions, thereby aligning with regulatory standards.

Moreover, rising consumer preference for gasoline-powered vehicles and equipment in both developed and emerging markets contributes to sustained demand. As urbanization and mobility needs increase globally, the gasoline segment is expected to maintain its leading position in the market.

By Application

Based on application, the reciprocating engine market is classified into power generation, automotive, marine, industrial, and others. The power generation vehicle segment is poised to witness significant growth at a CAGR of 4.81% through the forecast period (2024-2031). This robust growth is further reinforced by increasing global energy demands and the need for reliable decentralized power solutions.

Reciprocating engines in power generation offer flexibility, quick start-up times, and cost-effectiveness, making them suitable for various applications ranging from standby power to prime power generation. Particularly in remote and off-grid areas, these engines provide essential electricity supply without relying on centralized grids.

Furthermore, advancements in engine technology, including improved efficiency and emissions control, enhance their attractiveness for power generation applications. The expansion of the segment is further propelled by increased investments in infrastructure development, robust industrial expansion, and the growing integration of renewable energy sources.

Reciprocating Engine Market Regional Analysis

Based on region, the global market is classified into North America, Europe, Asia Pacific, MEA, and Latin America.

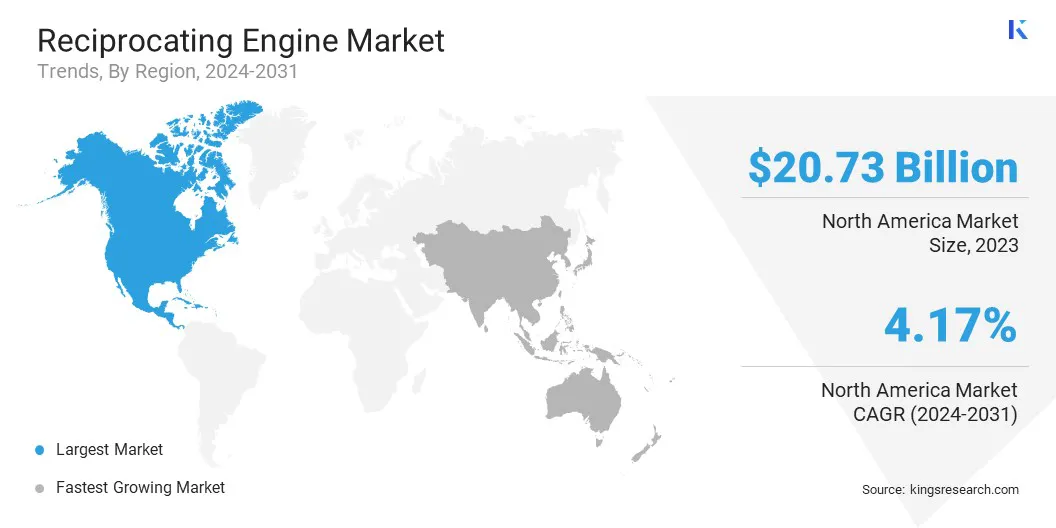

The North America reciprocating engine market accounted for a significant share of around 32.37% in 2023, with a valuation of USD 20.73 billion. North America dominates the market due to its established industrial infrastructure, significant investments in energy projects, and robust demand across various sectors. The region's leading position is bolstered by a strong presence of key market players investing in advanced engine technologies and sustainable energy solutions.

Moreover, stringent environmental regulations boost the adoption of cleaner and more efficient reciprocating engines, further solidifying North America's leading position. The region benefits from a mature automotive sector and extensive applications in power generation, marine, and industrial equipment.

Asia-Pacific is poised to at a robust CAGR of 4.92% through the estimated timeframe. This considerable growth is supported by rapid industrialization, urbanization, and infrastructure development initiatives. Increasing energy demands across emerging economies, coupled with favorable government initiatives promoting sustainable energy solutions, fuel the adoption of reciprocating engines.

The region's growing automotive production, expanding manufacturing sector, and rising investments in power generation infrastructure are key factors fueling market expansion. Additionally, technological advancements that enhance engine efficiency and reliability cater to the region's diverse industrial and commercial needs, contributing significantly to Asia-Pacific reciprocating engine market.

Competitive Landscape

The reciprocating engine market report will provide valuable insight with an emphasis on the fragmented nature of the industry. Prominent players are focusing on several key business strategies such as partnerships, mergers and acquisitions, product innovations, and joint ventures to expand their product portfolio and increase their market shares across different regions.

Manufacturers are adopting a range of strategic initiatives, including investments in R&D activities, the establishment of new manufacturing facilities, and supply chain optimization, to strengthen their market standing.

List of Key Companies in Reciprocating Engine Market

Key Industry Developments

- February 2024 (Partnership): Wärtsilä supplied its reciprocating internal combustion engines (RICE) for an 18 MW expansion at the Bluffview Power Plant in Farmington, New Mexico. The city of Farmington, acting as the buyer, signed an equipment supply contract valued at around USD 13.9 million. Wärtsilä planned to deliver generator sets and auxiliary equipment by January 2025. The selected Wärtsilä 34SG engines, are powered by natural gas and are adaptable to synthetic methanol, biogas, and a hydrogen blend.

- July 2023 (Partnership): Burns & McDonnell initiated the construction of Basin Electric Power Cooperative’s Pioneer Generation Station Phase IV, aimed at expanding its natural gas-fueled facility in the Bakken region by 600 MW. This marks Basin Electric’s largest single-site project since the 1980s, featuring Siemens STG6-5000F turbines and Wärtsilä W18V50SG reciprocating engines. The project addresses the increased electricity demand forecasted for 2025, thereby supporting Bakken’s economic growth. Basin Electric partnered with Burns & McDonnell in 2022 for EPC services, ensuring efficient planning, design, and execution to meet the ambitious timeline.

The global reciprocating engine market is segmented as:

By Type

- Gasoline

- Diesel

- Natural Gas

- Others

By Application

- Power Generation

- Automotive

- Marine

- Industrial

- Others

By Region

- North America

- Europe

- France

- U.K.

- Spain

- Germany

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- North Africa

- South Africa

- Rest of Middle East & Africa

- Latin America

- Brazil

- Argentina

- Rest of Latin America